Lebanon, exhausted by war in spring 2026, arrives at the negotiation table with Israel in a desperate socioeconomic position and an urgent question. The question animating Beirut’s government led by President Aoun and Prime Minister Nawaf Salam is whether a deal with Israel can secure a cessation of hostilities and unlock economic recovery.

In Lebanese society, the very idea of negotiating directly with Israel has important change-making potential, even though some of this potential is socially divisive. Moreover, although peace may be necessary for achieving a positive turning point in the economy, it is almost certainly insufficient. Lebanon’s economic collapse precedes the war, and its causes are structural, political, and self-inflicted.

To understand what a settlement can and cannot deliver, Executive has developed three scenarios. They are a peace-without-reforms scenario, a reform-without-peace scenario, and a reform-with-peace scenario, with an approach of mapping out the divergent growth trajectories each scenario implies.

The war between Israel and Hezbollah erupted in 2023 after nearly seventeen years of relative calm along Lebanon’s southern border before intensifying dramatically in September 2024. The conflict came at a time when Lebanon was already suffering from corruption, economic collapse, banking failure, high debt, lack of institutional sovereignty. Although the war lasted only two months, the ceasefire that followed never produced lasting stability, and violations and Israeli strikes persisted throughout the period.

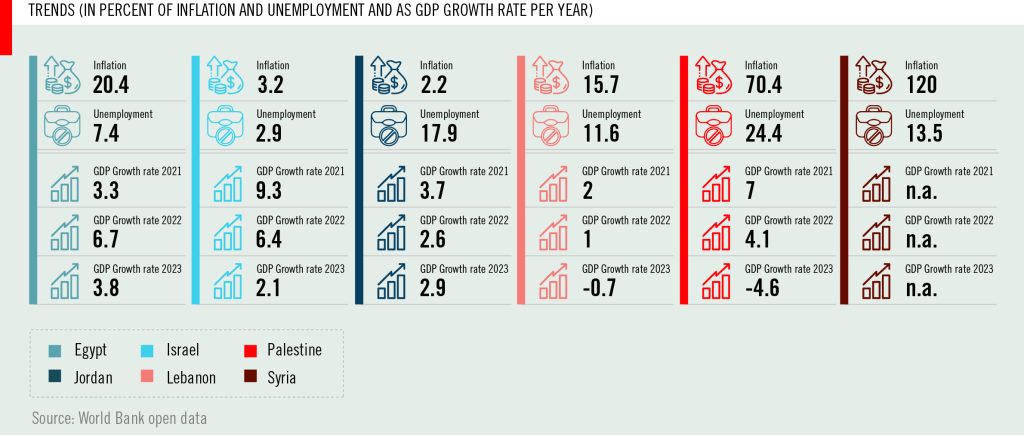

Following the November 2024 ceasefire agreement, Lebanon witnessed important political developments, including the election of a president, the formation of a new government, and a series of appointments across key state institutions. These changes helped revive hopes of reform and contributed to a modest economic recovery, with real GDP expansion to 3.5 percent in 2025 according to the World Bank Lebanon Economic Monitor after it witnessed a sharp contraction in the previous year.

In March 2026, hostilities erupted once again, extending beyond ninety days and renewing fears that Lebanon may remain trapped in a cycle of conflict and instability. By the end of May, Lebanon’s Ministry of Public Health had reported over 3,300 killed, with more than 10,000 injured. On May 21st, international news agency Reuters reported an estimate from the Lebanese Minister of Finance Yassine Jaber at 20 billion USD in damages and an economic contraction of seven percent.

Peace without reform

The first trajectory worth tracking is a peace scenario based on observable data from countries in the region that have embarked on similar endeavours. The 1994 Israel–Jordan Peace Treaty was an agreement that not only ended the state of war between the two countries but also built a foundation of trade cooperation, tourism, transportation, energy, water, telecommunications, and investment. The agreement was built on the belief that stability and regional integration would create new opportunities for economic growth.

In the year following the treaty, the World Bank recorded a six percent GDP growth, continuing a recorded two-year period of economic growth. Overall, the Hashemite Kingdom benefited from increased foreign aid, tourism, stronger diplomatic ties with Western countries, and higher investor confidence.

However, according to the International Monetary Fund (IMF) data, growth slowed in subsequent years and averaged roughly 3 percent annually since 2010. The slowdown reflected the persistence of structural challenges and weak institutional capacity. While stability helped improve the business environment, attract international support, and encourage investment, it did not fundamentally alter the country’s economic trend.

Jordan’s experience demonstrates the limits of peace as an economic strategy. More than thirty years after the peace agreement, the country continues to struggle with high unemployment, dependence on foreign aid, high public debt, and modest growth rates that generally fluctuate between 2 and 3 percent annually since 2010.

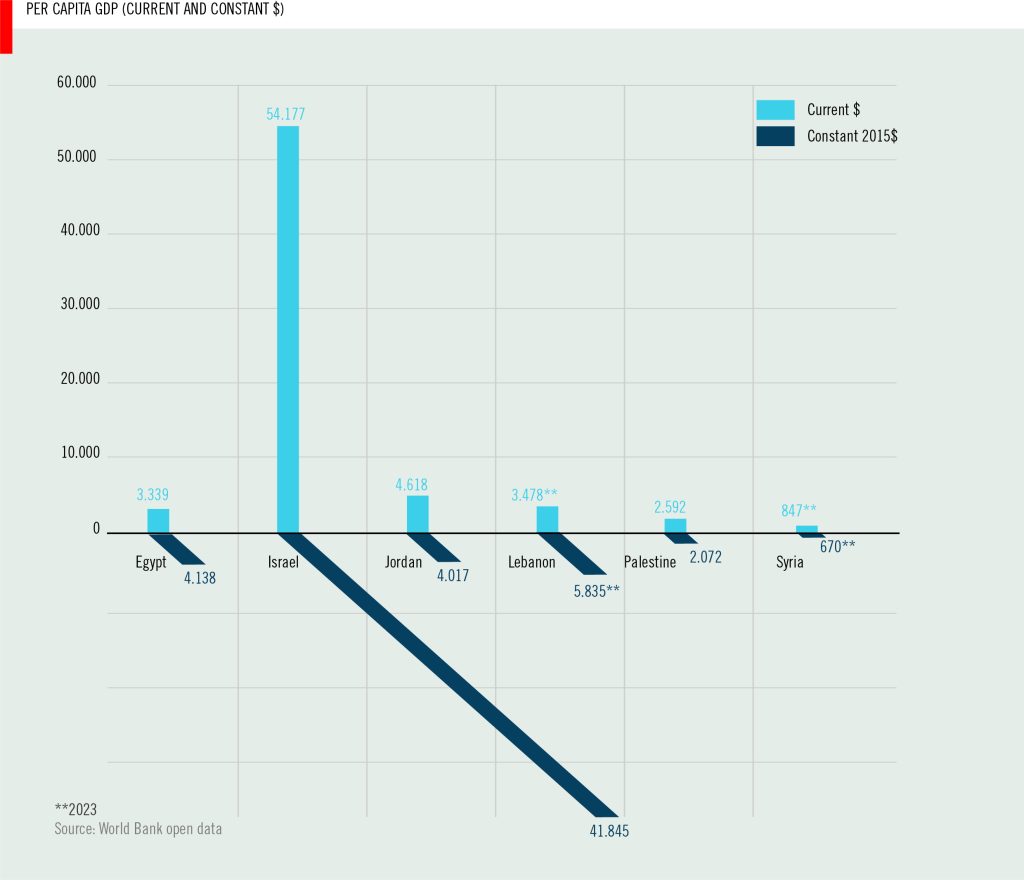

Jordan is not the only regional example. Egypt, the first Arab nation to officially enter a peace agreement with Israel, experienced a similar pattern. The Egypt-Israel Peace treaty of 1979, signed by President Anwar El-Sadat, Prime Minister Menachem Begin and witnessed by US President Jimmy Carter, contributed to greater stability, strengthened Egypt’s relations with Western countries, and was followed by substantial U.S. economic and military assistance combined with rising tourism revenues, remittance inflows, and increased activity through the Suez Canal.

IMF data reflects this as it recorded real Egyptian GDP growth at 3.4 percent in 1980, slightly decreasing to 2.2 percent following year, but accelerating to its highest recorded peak at nearly 9 percent in 1983. However, despite what may be described as an initial “peace premium,” Egypt has continued to face corruption, bureaucratic inefficiencies, inability to foster pluralistic growth, and persistent economic challenges since those initial dividends, and economic growth continued to drop dramatically for a decade. Although it expanded again in 1997 due to state-level structural reforms, Egypt’s economy is marked by repeated cycles of expansion and slowdown, with recoveries failing to reach previous peaks.

This pattern suggests that while peace may contribute to stability and growth, it does not guarantee a lasting economic transformation. The experience of both Jordan and Egypt suggests that peace can improve economic conditions and create new opportunities, but it does not by itself guarantee sustained growth or structural transformation.

Reform without peace

If peace is not, on its own, a guarantor of economic flourishing, it is worth asking whether reform without an enabling environment of negotiated peace is a suitable driver of growth. Lebanon’s own experience suggests that reform efforts alone do not guarantee sustained growth. Beginning in 2011, successive governments launched anti-corruption and governance initiatives, including the development of a National Anti-Corruption Strategy and the adoption of legislation on access to information, whistleblower protection, and anti-corruption oversight.

Yet these efforts unfolded within a context of political uncertainty and recurrence of war and sanctions, spillover effects from the Syrian conflict, and the arrival of large numbers of refugees. Despite these challenges, IMF data shows that the economy expanded from 0.9 percent in 2011 to 2.8 percent, 3.8 percent, and 2.4 percent in the three years that followed. This period illustrates how reforms and institutional improvements can support economic activity even in difficult circumstances, while also highlighting the limits of reform in the absence of lasting stability.

During the early years of Rafik Hariri’s premiership, between 1992 and 1996, Lebanon experienced a period in which ambitious reconstruction plans coincided with relatively high hopes for regional peace following the Madrid and Oslo processes. Hariri’s government launched Horizon 2000, a large-scale reconstruction and reform program aimed at rebuilding infrastructure, restoring the banking sector, and reviving Beirut’s role as a regional financial and commercial hub. This combination of domestic reform momentum and an external environment in which a broader Arab-Israeli settlement seemed plausible contributed to a strong economic rebound. The IMF recorded Lebanon’s average annual growth rates in the range of 7 to 8 percent during these years, reaching over 10 percent in 1996, the highest in its postwar history. Confidence in the currency was restored, capital inflows increased, and reconstruction activity drove growth across construction, services, and finance.

However, this period also illustrates the fragility of growth built on expectations rather than realized peace. As the regional peace process stalled in the mid-to-late 1990s and domestic political tensions resurfaced, growth rates declined sharply, and the debt burden accumulated during the reconstruction phase became increasingly difficult to manage. The 1992-1996 episode therefore offers a useful counterpart to the post-2011 period discussed above: whereas the later period shows reform proceeding without peace, the early Hariri years show strong growth driven partly by reform but heavily reliant on an anticipated peace dividend that ultimately did not materialize, leaving the economy exposed once those expectations faded.

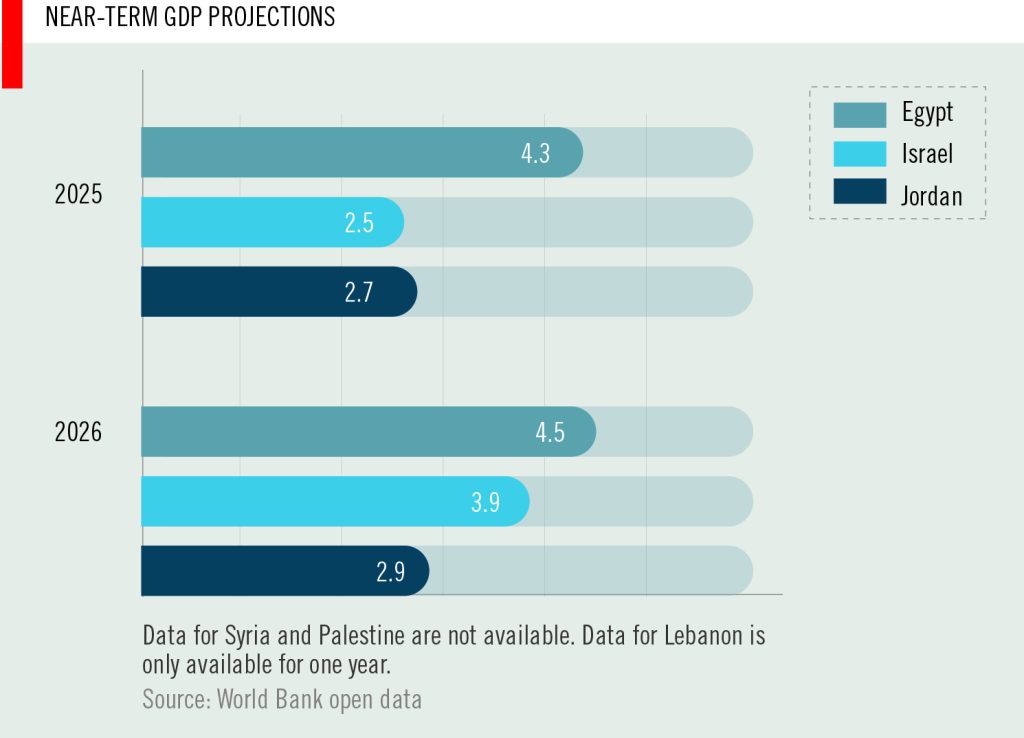

Building on this experience, Executive’s reform-without-stability scenario begins with the 4 percent growth recorded in 2025 by World Bank data, reflecting the gains associated with a period of relative stability and institutional reform. It then assumes a contraction similar to Lebanon’s 2024 after war recession, before returning to growth rates comparable to those observed during the post-2011 period.

Drawing on Lebanon previous experience and cycles, including the strong vacillation of GDP growth in the 2000s, the scenario assumes that a reform-without-stability trajectory is unlikely to follow a smooth upward path. Periods of growth may be interrupted by renewed security shocks, political crises, or regional tensions, producing a pattern of uneven recovery in which economic gains are followed by setbacks before growth resumes again.

This scenario suggests that reforms may help mitigate the economic costs of instability and support recovery, but their full benefits—which, according to Executive’s estimates, could translate to an economy with a GDP of 200 billion USD—are unlikely to be realized without a more secure and predictable political environment.

Peace and reform: an unrealized projection

Unsurprisingly, a more promising trajectory emerges when reform is coupled with stability. This speculative scenario assumes that Lebanon successfully addresses the mentioned issues and implements reforms while achieving the stability necessary for long-term recovery.

De-facto external peace, as it existed in a precarious way in the 2006-2023 period despite the absence of a state monopoly over violence and a concurrent dual presence of a political and a militarized Hezbollah organisation, has for the purpose of this scenario been replaced with the assumption of a formal peace treaty between Lebanon and Israel that is guaranteed by international and regional agreements.

This scenario anticipates a confluence of peace and reform momentum, the positive indications of which are borne out by data and expert opinions. In January 2026 Lebanon Economic Monitor, the World Bank projections estimate that Lebanon could sustain growth of around 4 percent if reform efforts continue and political stability is maintained, this aligns with IMF forecast. Several Lebanese economists, including Marwan Baraket, Layal Mansour, and Fouad Zmokhol, echoed similar views in interviews with Executive magazine, emphasizing the importance of structural reforms in restoring long-term growth and rebuilding confidence in the economy.

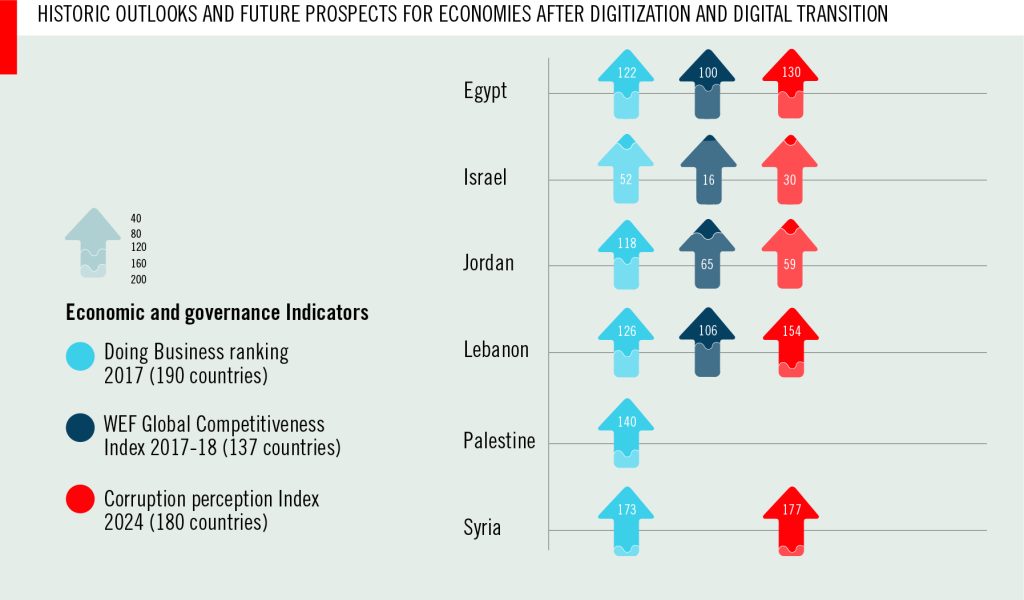

Decisively, this scenario also assumes that a solution for the longest-standing problem complex of inefficiency and corruption – which has invariably been identified as residing in the Lebanese power utility, Electricite du Liban – will be solved. A 2007 World Bank Policy Research Working paper estimated that reform of the electricity sector alone could raise Lebanon’s growth potential by approximately 0.2 to 0.3 percentage points annually.

Despite countless reports, conferences, popular protests, and governmental promises to the opposite, the proposition of EDL reform as potential growth booster is as undeniable in 2026 as it was in 2007. A June 2026 IMF “Diagnostic of Governance and Corruption (DGC)” cites the electricity sector as an examination of how corruption and patronage systems impact public service delivery and describes EDLL reform as outstanding.

The electricity sector in Lebanon provides a clear example of governance failure among other examples of mismanagement of state owned enterprises and state assets, many of which lack clear valuation. Decades of political interference, delayed reforms, and mismanagement turned what should have been a driver of economic growth into a major burden on public finances. The sector had become a symbol of the state’s inability to deliver basic services efficiently. According to BlomInvest Bank’s 2026 report, Turning the Lights On: Solutions for Lebanon’s Electricity Crisis, electricity-sector cumulative debt and related interest payments exceeded $43 billion by 2020, making it one of the largest contributors to Lebanon’s public debt.

Notably, many of the further structural challenges identified in the 2007 World Bank Policy Research Working Paper remain relevant today and progress in addressing the country’s key economic constraints has been limited. Additionally, a fiscal reform could generate annual growth of approximately 0.3–0.4 percent per year. Our scenario conservatively assumes only the lower bound of the electricity-sector reform estimate and gradually increases growth from 4 percent to 5 percent over the six consecutive years. This intentionally conservative assumption does not fully account for the potential gains that could arise from broader reforms in governance, public administration, anti-corruption efforts, and the banking sector.

The comparison of three scenarios highlights a central lesson for Lebanon: neither peace nor reform alone is likely to be sufficient. The peace scenario suggests that stability can generate important economic benefits by reducing uncertainty, encouraging investment, improving access to international support, and creating a more favourable environment for private-sector activity. However, from previous experience we can conclude that stability may create opportunities, but it does not by itself address the structural weaknesses that limit economic performance. The peace trajectory laid out here is an illustrative benchmark only and not a forecast. Lebanon’s economic structure, institutions, demographic profile, and political environment differ significantly from those of Jordan and Egypt, meaning the actual outcomes could be either stronger or weaker depending on a host of factors particular to the Lebanese case.

The reform-with-stability scenario produces the strongest outcome. In this case, governmental and sectoral increase long-standing inefficiencies and increase the economy’s productive capacity, while stability provides the predictability needed for business to expand. The combination allows the benefits of reform to be fully translated into economic growth and creates the conditions for a more durable recovery.

While reforms can improve economic fundamentals and support recovery, continued conflict and political instability would likely discourage investment, disrupt tourism, delay reconstruction, and leave growth vulnerable to recurring setbacks. Economic gains may still occur, but they are likely to be smaller, less predictable, and more easily reversed by future shocks.

The analysis therefore suggests that the greatest challenge facing Lebanon is not choosing between peace and reform but achieving both simultaneously.

The question facing Lebanon

The debate surrounding a potential agreement between Lebanon and Israel is often framed as a choice between war and peace, conflict and stability. Yet the economic question is more complex. History suggests that peace can create opportunities by encouraging investment, reviving tourism, reducing uncertainty, and opening new channels of regional cooperation. However, peace alone does not automatically translate into prosperity.

Lebanon’s economic collapse did not begin with the current war. Long before the latest conflict, the country was struggling with a banking crisis, chronic electricity shortages, rising public debt, corruption, and weak state institutions and infrastructure. These structural problems would continue to constrain growth regardless the situation on the border. Without stronger institutions, greater transparency, accountability, and meaningful economic reforms, many of the potential benefits of stability risk being lost to the same governance failures that contributed to the crisis in the first place.

The question facing Lebanon today is therefore not simply whether peace can generate economic benefits. History suggests that it can. The more important question is whether Lebanon can build the institutions capable of turning those opportunities into lasting prosperity.