It’s been anything but plain sailing. Joe

Faddoul, the 56-year-old chairman of

BML Istisharat, has been pursuing a

personal quest since he got into the computer

business almost 30 years ago. His

goal is to simplify the handling of complex

computing systems, the huge software programs

that companies and banks use to

manage everything from finances to customer

service. “We’re selling a service, so

our job is to be reliable and extremely cost-

efficient,” says Faddoul.

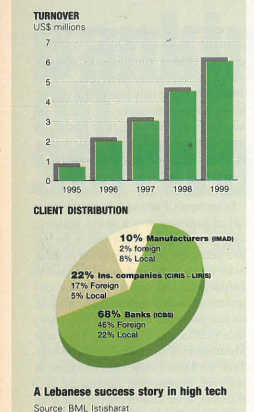

This could be rhetoric, but the fact is that

he has successfully marketed the company’s

products and lifted revenues from almost

zero in 1976 to $6 million last year (see

graph). The firm’s banking software,

Integrated Computerized Banking System

(ICBS), is mentioned in the annals of IBM

in New York as one of the top ten success

stories in software, and according to 1998

figures from the London-based International

Banking System, it ranks fourth out of 34 in

terms of sites where it has been installed:

some 40 banks in over 350 sites. With about

20 cents of operating profit extracted from

every $1 of revenue, Istisharat appears to

have something of a golden touch.

These respectable payoffs, rising to $1.2

million in 1999, have attracted such local

heavyweights as Societe Generale, Societe

Nationale d’ Assurance (SNA) and the

Lebanese Swiss Bank who are among the

company’s main shareholders. “Within its

class, BML Istisharat has the largest revenue base and the most advanced products,”

says Maroun Badr, assistant manager of

development at Societe Generale.

How do they do it? Analysts say

Istisharat’s $100,000 to $600,000 software

packages help organizations become more

customer-friendly on two fronts. This 28-

year-old company offers what both foreign

and local rivals cannot offer: a combination of

built-in customer profiling based on a successful

track record and personal attention

to the quirks of the local market. Using

Istisharat’s software, companies can make

their organizations more self-service oriented.

Credit Libanais replaced the French

software, Delta, with the Istisharat system

because, in the words of deputy general

manager Antoine Raad, “Istisharat has a

solid foundation for building the relationship

between businesses and the customer.”

Sammy Hashem of Libano-Suisse

agrees. The insurance company bought

Istisharat’s URIS package (Life Insurance

and Reinsurance), for about $100,000.

Today, Faddoul’s software firm derives

60% of its revenues from export sales to the

US and Western Europe, with a sprinkling to

the Middle East. Clients include Citibank,

Assurances Generales de France and

Banques Populaires (BPRNP). In the Middle

East and Lebanon, Banque Nationale de

Paris International (BNPI), Societe Generale

and Credit Bancaire all use Istisharat’s software

packages. But most of their bank clients

are foreign, not Lebanese. “This is a paradox,”

admits Faddoul. “Lebanese prefer to buy

blue-eyed software.”

Competition is particularly stiff from foreign

software manufacturers like Kindle

and Midas-Kapiti International (MKI) who

compete for banking accounts. They hold

the top three notches in sales figures of the International Banking Systems (MKI is

second and third with two banking packages,

Midas and Equation).

The Arab Bank has completely transformed

its operations over the past eight

years to install an English/Arabic version of

MKI’s Equation system. MKI’s software

was chosen because “the innovative use of

MKI IT has revolutionized our banking

business in the areas of cost savings and

improved customer service,” says Tarek

Abdulrezak, deputy manager of Arab

Bank’s IT department.

Kindle and MKI are subsidiaries of

Misys, a UK publicly-owned company

quoted on the London Stock Exchange.

The Misys Banking and Securities

Division (BSD) is the world’s largest independent

provider of software products to the

sector, supplying applications and services

to around 1,600 customers in 100 countries, 360 odd customers with Kindle’s

Bankmaster system, and the remaining

1240 on either of the MKI packages. In

1999, Misys generated revenues of $920

million and an operating profit of $213

million. BSD accounts for 60% of revenue

and the Insurance Division for 9%.

Given Istisharat’s turnover of $6 million,

Faddoul is hardly a big-company guy in

global terms. With his core of just over

100 key accounts around the world,

Faddoul is refining the art of nurturing customers.

Citibank has been a loyal Istisharat

client since 1988, which has accounted for

$2 million in sales in 11 years.

As a result of his own experience in market

research, Faddoul is quick to advise

potential clients to conduct thorough surveys

of corporate IT before any costly purchase.

He has also made local prices on

Istisharat software low compared to

Europe, at averages of $100,000 and

$350,000 for insurance and banking

licenses respectively, compared to

$250,000 and $500,000.

It may seem somewhat unexpected to

learn that Istisharat entered the electronic

arena almost by accident and that, like most

success stories, the company has humble,

back-office roots. Istisharat opened its doors

in 1972, on a radically different footing.

Istisharat, Arabic for consulting, was set up by

four partners, including Faddoul, with a

business plan aimed primarily at market

research and management consultancy. The

subsequent replotting of corporate strategy

came with the start of the war, when demand

for management consultancy and research

dwindled to almost nothing overnight. “War

forced us to transform into a computer services

company,” says Faddoul. By 1988,

Istisharat had graduated into a principal software

developer with a breakthrough on the

lucrative Citibank account.

But as IT matured, businesses were forced

to broaden their plans. Istisharat acquired

the agency for IBM in 1990 and an extra three

letters to its company logo. “Lebanon

Business Machines was our and IBM’s first

choice,” says Faddoul. “But that was already

registered by a company that sells typewriters.

So we became Business Machines of

Lebanon, BML Istisharat, a name we kept

even when we sold our IBM agency.”

It was with the same corporate eye on an

evolving electronic landscape that they

dropped IBM in 1995 in order to focus

solely on software development. “In the

1980s there were only four or five players

in the hardware business, now there are

hundreds and competition is that much

more cutthroat,” says Faddoul. “It became

clear that we were losing time selling computer

boxes when the real action had shifted

to software.”

In retrospect, Faddoul believes the move

out of hardware was a sound decision.

Turnover has grown eight-fold in the last

four years, and profit margins are as much

as ten points higher in the service industry.

Istisharat has 100 employees who are split

into three software departments and working

on four packages: banking (ICBS), insurance

(LIRIS and CIRIS) and Integrated

Manufacturing and Distribution (IMAD).

Their packages handle such functions as

management information systems and, in the case of IMAD, follow-up

on the manufacturing process.

Here’s how it works: Software is created,

developed under Oracle or AS/400 platforms

and installed on UNIX or NT, which

is then assembled into application-style

packages. These tailor-made programs are

then used either within companies or

between them, allowing companies to create

customized relationships with each of

their distributors or dealers and clients, giving

them up-to-date catalogs, order forms,

pricing, marketing materials, billing and

inventory. “We’ve developed our system in

a very parametric way,” says Faddoul

about their IMAD package. “You can use it

for textile or beer or cement.”

And while some 50 companies use the

IMAD system, bringing in a turnover in 1999

of about $600,000, IMAD represents only

10% of Istisharat’s business. The true

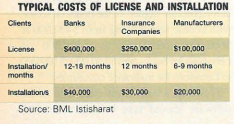

money-makers are in banking and insurance,

which, respectively, account for 68% and

22% of sales. Both licensing fees and installation

costs are higher for the financial sector,

with license fees ranging from $400,000 to

$600,000 ($350,000 to $400,000 in

Lebanon) for banks, and $250,000 ($100,000

in Lebanon) for insurance companies.

Typically, a bank implementation of the

software should take between 12 to 18 months, 12 months for an insurance company

and six to nine months for an average-sized

manufacturing or distribution business.

However, time frames can and do vary widely.

Six months represents roughly two

months in man-days, and these are billed at

$350 a day per project leader and $150 to $200

a day for a standard programmer, increasing

the net revenue for a typical project to

$30,000. Faddoul’s methods are sometimes

considered harsh but effective. He is also fair.

As the brainchild of a profit-sharing

scheme, 25% of company profits are redistributed

to members of the software teams.

An unexpected ally in Istisharat’s business

has come in the form of a general merging of

company descriptions and of nations.

Deregulation in the US and Europe has

brought a convergence of banking and insurance,

a move that is being copied in

Lebanon. “URIS is our latest child. In essence, it’s a bank insurance package which

we have already implemented at Fransabank

and Societe Generale.” Faddoul hopes that

URIS will become the next big earner as

more banks go down the insurance route.

Internationally, the European Union’s

(EU’s) move towards a single policy on tax

and other fiscal matters is also making life

easier. “The EU is actually helping our

industry to streamline and standardize our

products,” he says. At $600,000 per license

fee, the insurance package for the US is 2.4

times European fees. This is partly due to the

upgraded version that is being sold in the US

market, and partly to the differences in

legal reporting in each state.

If Istisharat’s contest with the foreign giant

Misys is something of a struggle between

David and Goliath, on the home front, at

least, the odds are stacked in Istisharat’s

favor. The company stands alone as a

Lebanese provider of banking and insurance

solutions in a market that has become saturated

with software developers all focusing on

similar back-office packages. “There are too

many players in a small field,” says Khalil

Taller, head of Logos, which provides general

bookkeeping and payroll packages.

“Recession is hitting hard with cutbacks in the

IT industry.” As much as 65% of Logos’

turnover now comes from export sales to

the Middle East, compared to 25% in 1998.

This is a strategy that’s been adopted by

Software Design, whose flagship Dolphin

business application package is sold in 15

countries in the face of a dwindling local

market. “In Lebanon’s software ecosystem,

there are essentially only seven or eight true

outfits in terms of western-style professionalism

and pursuit of high tech,” says Michel

Nseir, general manager of Software Design.

And in an emerging industry already marked

by fast consolidation, the company with staying

power may be Istisharat. “[Faddoul] has

done a great job in operations,” says Nseir. “I’d

say BML ranks about top on that list.”

Many executives complain that immature

technology and industry fragmentation

are keeping them from installing the latest

technology. That’s why Istisharat may have

an edge. Says Sammy Hashem of Libano-

Suisse, “In emerging software markets, the

people who win are the people who are

broad.” And Istisharat has proved that it is considerably broader than most of the 250 or

so local software developers. As the service

shakeout intensifies, smaller software companies

with tiny revenue streams are

already falling by the wayside. Skygazer

Technologies, which has been operating for

the past six years as IT consultants in both

the private and public sectors, recently disclosed

its decision to move its business

to Canada. “The bottom line is that

there’s no trust in this country,” says Abbas

Dagher, owner of Skygazer. “Poor business

ethics compound a market that is already stifled

by recession and government control.”

But companies like Istisharat should be

able to survive, not least because with a

healthy roll of major international clients,

they have chosen to specialize in a field that

pays as much attention to street credibility

as it does to software expertise.

Istisharat’s work should easily translate

into a dot-com environment. Faddoul doesn’t

believe that the rise in e-commerce can

adversely affect his traditional bricks-and-

mortar clientele. “Even if banking is transformed

into e-banking, the banking function

itself will remain,” he says. “There will

always be a need for banks, and therefore we

will always have a role to play.” Nor does

Faddoul feel the frustrations of being in a

backwater of the global economy, frustrations

that have driven countless other

Lebanese to take their talents and innovations

to Silicon Valley. “In today’s Internet

environment, it really doesn’t matter where

your head office is located. We can troubleshoot

a bug in Indianapolis, say, from the

comfort of our offices in Riad al Solh.”

Faddoul’s challenge now? To keep abreast

of e-banking and e-insurance with particular

regard to moves that would see software

developers operate their own portals on the

net. Oracle’s chairman Larry Ellison recently

funded a new Internet startup, NetLedger,

which aims to convince small companies that

it can do their bookkeeping over the Web. For

$4.95 a month, companies can hire

NetLedger to store and handle all of their

invoices, bills and general ledger records.

And while Istisharat’s eye is on a different

breed of customer, Faddoul still needs to woo

the industry with ideas that will fend off

rivals. If he can do that, then the rising e-tide

will assure smooth sailing for Istisharat.