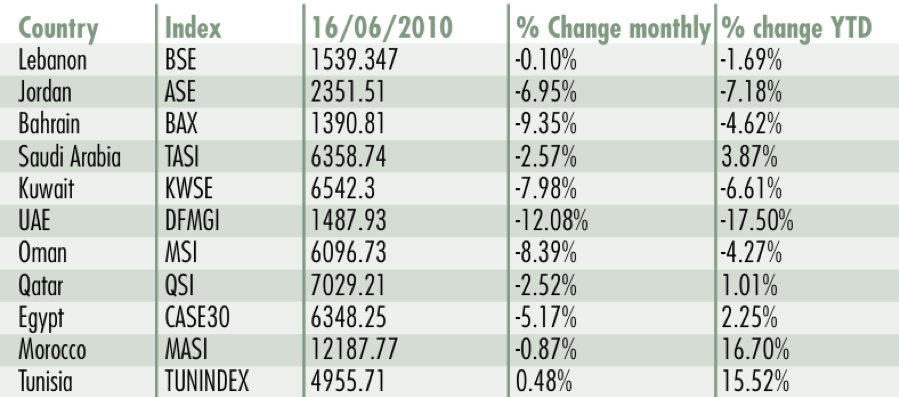

Regional stock market indices

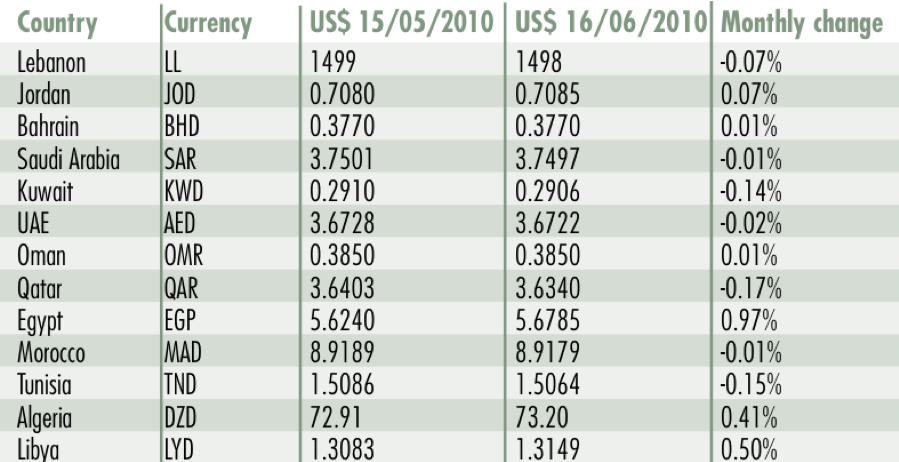

Regional currency rates

ICT aids textiles in Tunisia

Information and Communication Technologies (ICT) is currently the most promising sector in Tunisia’s economy. It has witnessed a growth of 14 percent this year, confirming the World Bank’s recent ICT access index that ranked Tunisia as top in the North Africa region. The sector’s importance was highlighted at the 8th Mediterranean ICT Summit, hosted on June 10 and 11 by El Ghazala’s Technological Pole, which was themed “ICT for the benefit of the competitiveness of textile companies in Tunisia.” Speaking at the occasion, the minister of communication and technologies stressed the importance of using ICT to boost productivity and enhance the added value and competitiveness of the textile sector. The country’s training of highly skilled human resources goes hand in hand with the sector’s evolution, as demonstrated by the recent convention signed between Tunisia and SunGard, under which the company plans to employ 450 engineers and university graduates in 2010, 650 in 2011 and 1000 in 2012.

Atomic alliance for Jordan and Japan

Jordan and Japan will sign a Nuclear Cooperation Agreement (NCA) before the end of the year. The Jordan Atomic Energy Commission (JAEC) announced that it has conducted long negotiations with Japanese officials to finalize the project, which will be located some 12 kilometers east of the southern coastal resort town of Aqaba. It will comprise a 1,000 and 1,150 megawatt model reactor, which incorporates technology from AREVA’s Evolutionary Power Reactor and Mitsubishi’s advanced Pressurized Water Reactor, and is expected to be completed by 2020. The JAEC and project managers Worley Parsons will begin a year-long process to select the final bidder, focusing on technological aspects. Jordan has already signed NCAs with France, Spain, China, South Korea, Canada, Russia, the UK and Argentina.

Investcorp rolls in the profit after US tire firm sale

Investcorp, a manager of alternative investment products with $12.4 billion in total assets under management, completed the sale of American Tire Distributors (ATD). The investment company had acquired ATD for $700 million in 2005 in collaboration with Berkshire Partners LLC and Greenbriar Equity Group LLC. Investcorp realized capital gains of $600 million in its five-year acquisition period, selling ATD for $1.3 billion. Investcorp has offices in Bahrain, New York, and London and is listed on both the Bahrain Stock Exchange and the London Stock Exchange.

ATD’s initial plans to go for an IPO were likely scrapped after TPG Capital bought the company from Investcorp. TPG will finance its acquisition through a combination of equity and debt financing from affiliates of Bank of America, Barclays Capital, General Electric Capital Corporation, and RBC Capital Markets. ATD is the largest independent tire distributor in the US, with 83 distribution centers, serving 37 states and 60,000 retailers.