With a geographic size that dwarfs its neighbors in the Gulf in particular, and the Middle East in general, Saudi Arabia is in the sights of private equity firms who are looking to the kingdom as a potentially excellent market.

With new plans sprouting up to develop the country’s infrastructure, particularly in the transport and communication sectors, as well as down-market industries in the supply chain of goods and services, Saudi Arabia is a slow giant ripe for the introduction of management efficiency.

A slow relaxation of regulations on private equity firms is just one of a series of measures — along with building the social infrastructure of education and healthcare — where the kingdom is thoughtfully giving a thumbs-up to private equity groups looking to enter the market. This is done through obvious contacts with regulatory and other government authorities, but also with the country’s major family firms.

Having spent over a decade in the kingdom, Richard Dallas, managing director of private equity at Gulf Capital, has noticed the difference between the Saudi market and those of its neighboring economies.

Dallas believes that both the UAE and Bahrain “have been leaders in creating regulatory and economic environments that have been inviting and welcoming to foreign investment, particularly the development of the banking and financial services sector.”

Because Saudi Arabia is the biggest market in the Gulf Cooperation Council (GCC) and its economic powerhouse, the economy is “slower, more deliberate and has a regulatory scheme that is changing on a more deliberate basis.”

But the kingdom has already made significant changes. Fadi Arbid, executive vice president for Amwal Al-Khaleej, pointed out that the Saudi government shifted from its traditional policy to spend 60-70% of GDP on defense and infrastructure to the new plan whereby more than 50% of the GDP is being spent on education and healthcare. To prepare the country for an era of declining demand for oil and the possible price drops associated with it.

Wadah Al-Taha, head of strategies at Emaar Financial Services, explained that Saudi regulators “have to set criteria, they have to be careful, then they have to make a move,” attributing the caution to the relative size of the country and the potential for grave errors from a regulatory or economic misstep.

Establishing a castle in the kingdom

Culturally, however, entry into the Saudi market is a new frontier for private equity firms. They must understand how to navigate policies by deciphering them. Firms seeking entry into the Saudi market are also best served by a synergetic partnership with families in the kingdom.

The largest families are mainly sought out for their networking potential and relationships with them are cultivated through a mixture of attracting them to a specific private equity firm as an individual investor or as the owner of a company in which a private equity firm owns a minority stake.

Deliberate, careful motions are not only the way Saudi authorities move but also how new firms proceed as they seek to gain entry into the country. By doing one successful deal with a Saudi firm, a new private equity firm might establish a relationship that generates more deal flow than previously imagined.

Shailesh Dash, senior vice president of alternative investments at Global Investment House, explained that “family-owned businesses in the MENA region are often diversified across vertical and horizontal lines of their supply chain and, accordingly, many family-owned businesses also engage in activities that are unrelated to their primary business. As ownership and control of these family-owned businesses move into future generations, the need to capitalize assets often becomes important, as some of the successors may want to pursue independent interests or liquidate their interest in the business.”

There is a need for liquidity and a “formal capital structure in an increasingly competitive free-market economic environment, which will result in significant merger, acquisition and divestiture activity. We have capitalized on these opportunities and many times have been invited by various families to corporatize them and grow their businesses beyond their countries boundaries and helping these businesses in acquiring economies of scale.”

The help Global Investment House provides to firms comes in several varieties, including “providing liquidity to the family group as a buyer of the group’s non-core businesses or as an investor in the group’s core business, providing suitable exit opportunities by identifying regional or international partners, valuing the business and assisting in various divestment activities to create value for the shareholders of such business, and providing a framework for target identification, target screening and transaction execution to assist in making strategic acquisitions for a family group’s core business.”

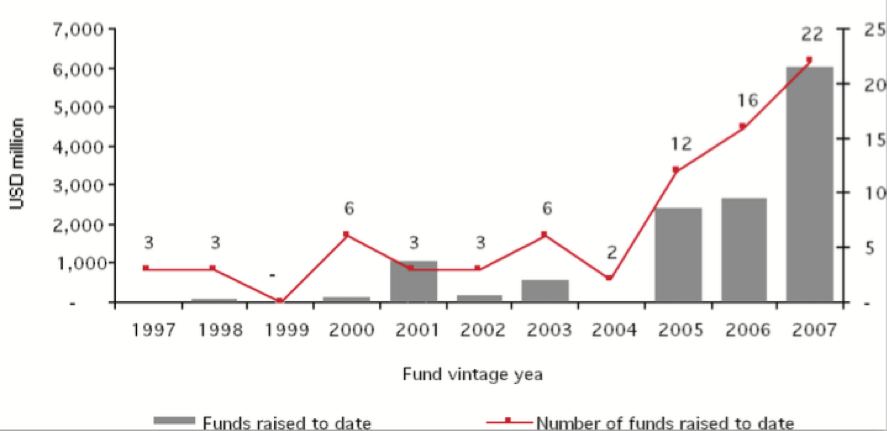

KSA public equity issuance ($ million)

According to Richard Dallas, managing director of private equity at Gulf Capital, “they are very guarded and careful about making sure they do everything in an organized fashion, so that they understand the consequences of what they do as much as they can.”

The reasons for this lie not only in the special role played by Saudi authorities as the guardians of the two holiest Muslim sites and the hosts of the hajj. Although these are important factors in a majority-Muslim region such as MENA, and for the significant Muslim populations of South and Southeast Asia, the internal population dynamics are putting pressure on the Saudi state to consider the future of a people whose riches and nobility are to a large part maintained through their natural resources, or down market-related industries. Dallas said, for the authorities “job creation is very, very important. For a long time they have been very focused on providing opportunities to their younger people, so I wouldn’t say they are slower or more resistant to change. I would just say they are more deliberate in what they do. Because if they don’t, quite candidly, they would make a major misstep and I think that this deliberateness will ultimately serve them very well.”

Every major private equity firm gives due consideration to Saudi Arabia. If they do not already have businesses in the country or at least relationships through investors in their firms, regional and global private equity managers are assembling their teams to penetrate this new market. Rasmala Investment Holdings is just one private equity group that received a green light from the Saudi Capital Markets Authority to expand its service in the kingdom.

In addition to its private equity business, Rasmala will be able to operate its mergers and acquisitions and IPO advisory arms. When the group appointed Hamad Mubarak al-Huthaili as the general manager of Rasmala Saudi Arabia, the company’s CEO said that “Saudi Arabia is the largest and most important capital market.”

This appointment hints at the importance of the country’s relationship-driven business culture as al-Huthaili had previously worked for four years at the Saudi Monetary Agency, in addition to other firms in the Saudi financial sector. His experience is likely to provide Rasmala with the sort of inside deal generation necessary to sustain business with key contacts in the kingdom.

A. Shabu Qureshi, director of EMP Global, related his firm’s investment in SIPCHEM, a Saudi diversified petrochemical company. Explaining the market dynamics of the Saudi regulators, he pointed out that “what the Saudi government has done is to allow ARAMCO to controlling the upstream industry, but then to get the private sector involved in downstream investment.”

At the time of the investment, three years ago, EMP took a 23% stake in the company, which then “executed its business plan well, and was able to go for an IPO quickly. It was a very good growth story and a sort of poster child in Saudi Arabia for what the government has been able to achieve by encouraging some degree of privatization, and how some of the dynamic family groups there, in this case the al-Zamil family, have been able to take advantage of this.”

However, Qureshi admitted that “it is a bit of a challenge to penetrate the Saudi market.” He attributes success in Saudi Arabia to the fact that EMP has a “good network of people in Saudi Arabia and we know the government as well as the industrial groups. Also, the Saudi pension funds, including the PIF and the PPA have invested with us, and they have been a very big help to us.”

In addition to EMP’s investment and exit of SIPCHEM, the firm also invested in APPC, a Saudi single purpose petrochemical company manufacturing polypropylene. “It was a greenfield investment where we went in very early and just worked with the company by sitting on the board of directors. The company recently achieved an IPO and is about to begin production. Under the radar, Saudi Arabia has achieved a fair amount of macroeconomic liberalization. And then firms like EMP Global are able to help that along and take advantage of what the government has done.”

Knighthood

Having an institutional backer during its start of operations aimed at the Saudi market was important for EMP, which had the backing of the Jeddah-based Islamic Development Bank, where, according to Qureshi, the firm “had some friends we could rely on for support in the region. The IDB is important for the region as a leading multilateral institution, and we also had the support of two of the Saudi government pension funds.”

In addition to the Saudi pension funds and IDB, EMP “had some prior relationships and our local executives were very familiar with the market and the industrial groups. We don’t go in and punch over our weight. That has over time allowed us to have good relationships. We tend to look at each investment by itself and to add our best professional advice, and not to favor one family group over another. We also look to bring our international relationships to the table if they can be of use to our portfolio companies.”

The bridging of Western models and what some observers affectionately call ‘Bedouin math’ is taking root in the kingdom. Qureshi thinks that “as Western banks and investment banks establish themselves in Saudi Arabia, both parties will benefit. The Western banks will get more familiar with the Saudi market, and that will benefit the Saudi partners and families who will get better access to Western financial technology. Having people on the ground with Western technical skills and knowing how the region does business is helpful for both sides.”

Abe Saad, head of private equity at Rasmala, believes that, “the kingdom is one of the largest markets in the GCC. It hasn’t been treated as it should be on the private equity side, though.

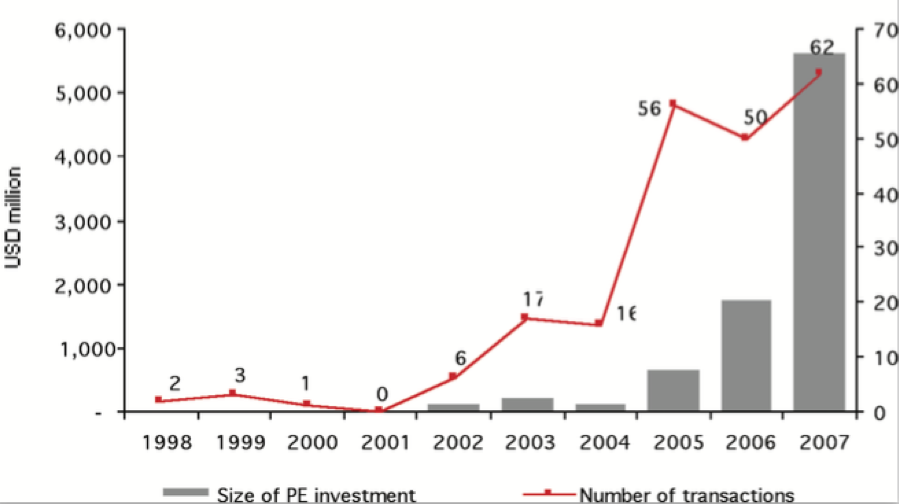

Composition of total estimated value of projects in KSA. Total value $665.42 billion