When visiting Concord last month, EXECUTIVE got that “it could only happen in Lebanon” feeling. Representing this $50 million-a-year conglomerate is not some hard-headed CEO with years of experience, but two relative youths, Ihsan Hafez, 32, and his cousin Khaled Hafez, 25, both sons of the company owners. A typical family business.

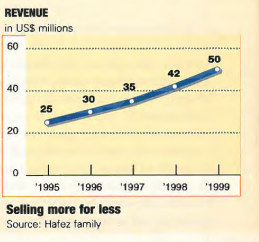

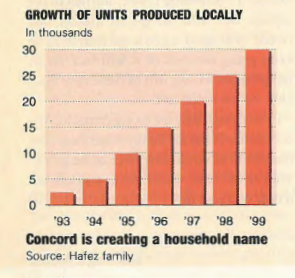

But you can’t argue with results. The combined revenues of the family’s business, which comprises a variety of companies in the region focusing on refrigeration, have exploded in the last five years, from $25 million in 1995 to $50 million in 1999. One example of this growth is in Lebanon, where production jumped from 2,500 refrigerators in 1992 to 30,000 in 1999. And these figures took place in the face of heavy competition from imports and a shrinking local economy. So what gives?

The first answer is that the Hafez family runs a diversified operation that is not tied to the sick Lebanese economy. The family group manufactures household appliances in Lebanon, Syria and Saudi Arabia. Unusually, the company sells its products under different brand names: Concord in Lebanon, Al Hafez in Syria and Lematic in Saudi Arabia.

Furthermore, unlike many Lebanese companies that believe that the rich will always be around in large enough numbers to support them, they’re not, the family has no delusions of grandeur; its products are downright inexpensive.

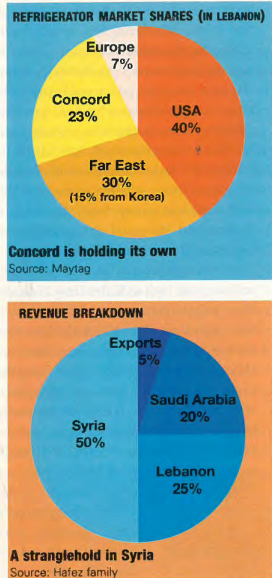

Lebanon is a good test case. In a market where established brand names like General Electric, Maytag, Samsung, LG, Hotpoint and others all have local distributors competing for market share, Concord has around a quarter of the refrigerator market. This adds up to $10 million in sales, the single largest chunk for any company.

The simple reason for this is that Concord refrigerators are the lowest priced coolers on the market. According to Raji El Mayla, the regional manager for Maytag, a US manufacturer of household appliances, Concord is on average 35% less expensive than Korean-made refrigerators and 45-50% less than the American competition.

For example, a 27-ft³ Concord fridge/freezer retails at anywhere from $750 to $840, while its Korean and US counterparts sell at slightly more than $2,000 and $2,500 to $2,700 respectively. In an economic recession, with people seeing their purchasing power decline, this pricing strategy is working like a charm.

“It’s a good time to sell low-end,” says Antoine Cherfane, president of AC Holdings, importers of the Korean Samsung brand. Historically, US brands have dominated the Lebanese market, one that once had an insatiable appetite for good quality and large-sized refrigerators. However, the recession has been particularly hard on US imports. “US imports overall have dropped 30% in the last three years,” says Majed Al Zein, deputy general manager at Abdulrahim Diab, a pioneer wholesaler of home appliances and sanitary ware in Lebanon and a supplier of Maytag refrigerators. US imports went down from 36,000 units three years ago to some 23,000 units in 1998 and “won’t exceed 15,000 units in 1999,” predicts Mayla.

Statistics from the Ministry of Economy and Trade show that imports of complete refrigerator units went from $21 million in 1998 down to $15.7 million in 1999. The beneficiaries of these conditions were the lower-priced Korean companies, which managed to increase their imports from $3.23 million in 1997 to $6.41 million in 1999, and Concord, which has boosted its production by 10,000 units since 1997.

But the key for the group in Lebanon is that no one can match or undercut its prices. Although there are some 500 suppliers of commercial refrigerators for mini-markets and supermarkets, such as Adam and Takal refrigerators, Concord is the only manufacturer of domestic refrigerators. It doesn’t have to fight any price battles with local competitors, something very few Lebanese businesses enjoy. Similarly, with shipping, customs and clearance adding 35-50% to the cost of US and Korean imports, Concord does not have to fear price competition from imports.

Concord backs up its low pricing with a strategy of taking good care of customers. Although it sells directly to retailers and distributors, its strategy is to provide service directly from the producer to the end-user, thereby relieving their buyers of the responsibility and gaining the trust of the consumers. The company has 10 roving trucks that go daily to all corners of Lebanon, carrying out maintenance and replacing parts.

But Concord does something unparalleled by any of the importers. It goes beyond its three-year warranty and replaces any damaged refrigerator parts for free. “Concord is very generous with their spare parts,” says Walid Tahan, sales manager at Abed Tahan and Sons, arguably the top retailer of household appliances. Tahan sells some 6,000 refrigerators a year, including some $400,000 worth of Concord refrigerators. “Our large volume of sales in refrigerator units allows us to replace a $10 plastic tray for free because it only costs us 10 cents to assemble it,” says Khaled Hafez, who handles factory operations. “So instead of burdening our distributors with that cost, the company prefers to absorb that cost to offer a better service.”

Since 1994, Concord has also maintained advertising of $600,000 a year, 80% of which is spent on ever-powerful TV commercials with the rest distributed among other media outlets. That budget exceeds the $470,000 budget put in by the Maytag Group for its number one brand Maytag, the group’s total budget averages $600,000 for its collective brands, namely Maytag, Hoover, Admiral, Magic Chef and Norge, and the budget for Samsung is just over $500,000. Thanks to this branding strategy, Concord has made itself a household name with many consumers.

Still, Concord is far behind the quality of its foreign counterparts, some point out. “Concord has more problems than US or Korean imports with leaks, noise and doors that don’t open or close well,” says Tahan.

But comparing the capital available to importers and their volume of sales to that of local manufacturing, it is easy to see why imports are better quality. Samsung has the newest factory in the world, costing hundreds of millions of dollars to build and which produces more than two million units a year but employs fewer than 30 workers. On one production line, robots assemble five different models and five different colors, achieving a ‘zero’ stock level, i.e. orders are manufactured simultaneously with other orders to remove the need for storage.

Samsung has used this efficiency and consistency in manufacturing to boost its sales volume by 25% a year in Lebanon. On the other hand, Maytag has invested some $220 million in a new technology called Advanced Product Design. Maytag has been the number one brand in the US for three years in a row, according to the US-published Consumer magazine. This new technology essentially eliminates noise, leaks and makes refrigerators totally rust-proof; Maytag has used this new technology to increase its local market share against other US importers from 32% in 1997, to 41% in 1998 and 61% in 1999.

Nonetheless, Concord is trying to improve quality within the means it has available. As production increases, quality will also improve as more money is invested into offering a better quality product. Concord invests about $1.5 million a year on upgrading machinery to improve the finish and on computerized equipment that performs internal temperature monitoring on the production line. “The manual test used to take us eight hours to perform, now the computer does it in two and a half,” says Ihsan Hafez, who handles the sales, exports and finance. Last year, the company increased its production by 5,000 units, but has maintained the same number of service calls, an indication that maintenance efficiency has improved.

The biggest chunk of the family’s business is generated in Syria. According to Ihsan, half of all revenues, some $20 million, originate from Syria, twice as much business as in Lebanon. The original company founders were Syrian, beginning with a small factory in 1952 which was later nationalized in the days of pan-Arab nationalism. Another larger factory was built in the early 1970s by the government, which ironically is now the factory that Al Hafez uses today. So now the company competes against a government-run factory it used to own and one other local manufacturer, a partnership between Joud and Syrian Batric Company, two large local manufacturers of a range of home-appliance brands such as Hi Life, Penguin, Zerowatt and Riviera. The family reckons Al Hafez has half of the market share in Syria, which consumes 120,000 refrigerators a year. That leaves 30% for the government, 15% for the Joud/Batric outfit and 5% for a slew of small workshops spread throughout the country.

But regardless of which company has what share, Al Hafez enjoys some marked advantages while operating in Syria. The company has seen sales increase by 20% a year. It produces about 30 refrigerator models at any one time; the competition, Khaled claims, manages to produce only three or four models.

Having a factory in Syria guarantees another advantage. For one, the country is a closed market to all but a few imports and thus competition is limited to local manufacturers. “In Syria you can import according to a quota, in a very limited fashion,” says Raymond Daou, sales manager at Samsung’s main showroom. Al Hafez is already an established brand name with more than 50 years in the market, and newcomers will have a very hard time taking away market share from it. “Al Hafez has their tradition and history in the market,” says a Joud representative in Syria. And, even though a free-trade deal exists with Syria, don’t look to Lebanon for increased competition.

Despite a 25% cut in import tariffs between the two countries since January 1999, Lebanese exports have declined from $47 million in 1998 down to $27 million in 1999. The deal has run into serious snags, mainly generated by the complex bureaucratic procedures that are still in place in Syria, leaving many Lebanese exporters wondering about the usefulness of the agreement. Although the accord stipulates the immediate removal of all paper formalities for the exchange of goods, customs officials on both sides of the border have ended up as the real enforcers of the agreement. Traders cite red tape and corruption as the major obstacles to trade. A further 25% cut in tariffs, bringing it to a 50% total cut, took effect last month, but it is too early to predict the effect.

Another advantage to having a factory in Syria, says Khaled, is that the current market will not provide sufficient returns on the investment necessary to break in. “If you’re already in Syria, you can invest little by little and grow gradually. But if you have to put in $30 million to start a new factory, it’s nearly impossible to make it.”

The Al Hafez factory only supplies the Syrian market and spends around $700,000 in yearly advertising to market its products. But what if peace with Israel takes effect and borders open up, will the company be affected? “It’s better for us,” says Ihsan. “Labor cost will still be down, the cost of parts will be reduced and since we’re the only ones selling in large volumes in Syria, we will have the best chance of surviving in the market.”

The final manufacturing operation of the family business is the 10,000 m² factory in Saudi Arabia, which produces 50 commercial freezers per day used for ice cream displays; Lematic complements the local market with imports of refrigerators from the Lebanon factory. The company does not manufacture refrigerator units in Saudi Arabia since local competitors produce 50,000 units a year, not to mention around 30,000 US imports. Saudi operations represent 20% of the group’s total annual turnover, $8 million, and spend $500,000 in advertising.

But since profit margins on refrigerator sales do not exceed 3% to 5%, the company has looked to diversify its operations. To that end, the family has started an industrial engineering company to take on turnkey projects in the region. This involves building home-appliance factories from scratch, starting with the design, moving into the manufacturing line, supplying the machines, operating them and transferring the entire operation to its clients. In almost all cases, these are government-run factories or government-funded projects, designed as an incentive to produce locally.

The family has built half of all the refrigerator factories in the Gulf. In order to support these activities during the civil war, the Lematic group built factories in Turkey and Italy and design offices in Germany, Britain and Canada.

An average project starts at $5 million and can go as high as $20 million. Now that these projects have been reduced to one or two a year at most, these factories have been reduced to representative offices. However, although factory building is slow-going due to the saturation of factories, agreements with the factories they built stipulate that the family supplies them components, and this currently represents a nice and steady income stream, 20% of sales in 1998 and 1999, for the company. In the early 1990s, when building projects were peaking, the company was supplying components that used to represent 55% of its turnover.

The company also branched into the commercial end of the market, supplying freezers and drink cooler cabinets for such clients as Pepsi, Cortina, Iceberg, Dolsi, and Maccaw. These companies use the refrigerators to push sales of their products and distribute these machines free of charge to supermarkets and grocers. Having the capability of high-volume manufacturing, the company has essentially pushed all competition out in Lebanon.

Hryar Atamian, the general manager of Adam Industries, was one of those supplying the market with soft drink coolers. “This market became dead for us because we couldn’t compete with Concord’s lower prices and volume of production,” he says. “Concord has almost a 100% market share supplying freezers, soft drink coolers, but we do have 15% of the supply of juice coolers for companies like X-tra, Libby’s, Snapple and Gatorade,” says Houssam Moghraby, sales and marketing manager at Joud Lebanon. Joud took that share by applying some special marketing techniques that included allowing clients to lease instead of buy, offering free parts and service, even if the user broke it, and free delivery. Joud Lebanon is also trying to get in on the cooler refrigerators and water cooler market under its brand Riviera.

Diversifying even more, the family also manufactures twin-tub semi-automatic washers and supplies the Gulf, Algeria and Libya, where most of its sales occur due to water and electricity shortages. They are competing against Chinese manufacturers, which got involved in the business about 10 years ago and have flooded the market due to overproduction. Lematic produces about 10,000 units annually, supplying anything from 2,000 to 20,000 components depending on the year, but its local sales are declining because as electricity is restored, people are shifting to fully automatic units.

Besides that, the family decided it wanted to tackle global competition. In 1998, the group embarked on an expansion program trying to export more finished products than components. It has entered North and West Africa, the Gulf and parts of Europe. As soon as customs barriers between Egypt and Lebanon were lifted, the company jumped into that market, where there are close to 60 million consumers.

The family is leaving it up to the wholesalers in these markets to advertise and market the products and also to provide service and maintenance. It will use these cost savings to introduce very inexpensive products and will not make any profits on them. The main goal of the company at the beginning will be to increase market share and establish a foothold in these markets. The exports will originate from Lebanon; the family won’t open a factory there, even though it would mean significant savings on shipping and customs. “I cannot enter the market with a factory and supply only a limited amount, it’s too risky,” says Hafez. Instead, the company will concentrate on increasing its sales until it reaches a respectable amount of units sold, around 20,000, that warrants investing in a $20-30 million factory.

And the group has made progress in the new markets, selling a total of 1,000 units in 1998, and 4,000 units in 1999. Although making no profits on those sales, economies of scale indicate that selling more volume reduces the cost per unit of manufacturing, thus generating indirect profits not coming from the sale of individual units.

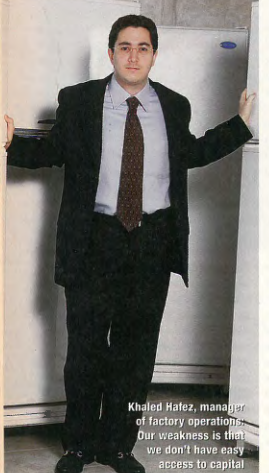

However, this expansion program faces some obstacles. For one, Lebanon is the most expensive country to export from. To get a container from the factory to the ship will cost $400 per container, so the prices have to be discounted even further. Secondly, even if the company decided to open a factory overseas, it doesn’t have the resources. “Our weakness is that we are not a shareholding company and we are not listed, so we don’t have easy access to capital,” says Khaled.

Like the family outfit that it is, the company is reluctant to open itself up to outside influence. And this could be a deciding factor in its continued sales success. Lebanon’s economic future, and that of the region, lies with the global market; the family will need significant resources to keep going forward or it will face rivals jumping ahead, not just in these new markets, but on home turf.

Even though they are facing obstacles, the bottom line is that the family wants these new markets to be the driving force of the group. They’re hot now; we’ll have to wait and see if they will cool off.