The office of Fadi Cumair, the director general of equipment at the Ministry of Water and Electricity, is a plush affair. While his secretaries were busy serving liqueur and chocolates, Cumair was explaining that if any person other than himself was to be quoted in this article, he would not provide any information. Cumair’s attitude, which is ironic considering he is a public servant, seems to typify the less than assiduous approach of local authorities towards the issue of proper water resource management in Lebanon.

In the Middle East, countries go to war over water, it is such an important issue. But, as far as government spending in this area in Lebanon is concerned, well, it isn’t. If the government’s allocation of financial resources in its annual budgets is any indication, attention to its water resources has increasingly taken up less of the government’s attention in the past decade.

Philippe Zgheib, an economist and professional hydrologist, made some calculations based on budget figures published in Lebanon’s monthly Official Gazette between 1984, 1994 and 1997 to prove the point. In constant dollars, annual budget expenditure for ministries such as defense, interior and labor has increased significantly. But budget expenditure for the Ministry of Water and Electricity has decreased from more than 7% in 1984 to just 0.2% of the total expenditure in 1997. Moreover, while aid from multilateral lending institutions such as the World Bank has been used to fund the rehabilitation of the electricity system, there has been no major funding for, or investment in, dams or other forms of water infrastructure. Similarly, the Ministry of Public Works, which is responsible for infrastructure projects required for water resources such as dams, saw its budget collapse from 22% of total expenditure in 1984 to 0.7% in 1997. And considering that wages and salaries absorb almost 40% of the state’s total budgeted expenditure, the money that has been provided has most likely been spent on just keeping the ministry’s employees paid.

Why has the government been so stingy in allocating resources to water? Governments are notoriously shortsighted and in Lebanon, the reality is that water has not been an issue weighing heavily on the government. Lebanon, at least for the time being, is not in dire need of water, unlike most other countries in the region. And considering the obvious repair needs after 15 years of civil war, perhaps it is understandable that water received less attention than urban reconstruction and telecommunications.

But scientists reckon spending policies have been shortsighted. Although Lebanon may have enough water for its domestic and commercial needs in a year of average rainfall, that will not always be so.

Population in the Middle East is growing at 2% to 2.5% annually, which means that water for domestic use will be in increasing demand while the productive sectors of the economy that rely on water, such as agriculture and industry, will come under pressure.

The equation is fairly simple. Lebanon is dependent entirely on precipitation, be that rain or snow, for its water supply. According to Musa Nimah, a professor of irrigation and soil physics at the American University of Beirut, Lebanon on average receives 860 to 900 mm of rain in a good year. If this figure is multiplied by the area of Lebanon, 10,452 km², Lebanon has a water supply of 9,200 million m³ per year. When rainfall drops below average, as in a time of drought, that figure drops to around 6,000 million m³ a year.

But there are problems with this figure. Lebanon lacks dams, reservoirs or other water-holding facilities to maximize the country’s use of its annual rainfall. Through evaporation loss, runoff loss, it runs into the sea, and other inefficiencies, approximately 50% of total annual rainfall is lost. That leaves Lebanon with around 4,600 million m³ per year. Out of that, 650 million m³ goes to Syria through the Orontes, Assi, River and the Northern Al-Kabir, 165 million m³ goes to Israel via the Hasbani and Wazzani tributaries of the Litani River, and 700 million m³ goes underground.

So in a year of average rainfall, Lebanon is left with approximately 3,200 million m³; in a year of drought, that falls to 800 million m³ to 700 million m³. And that, says Nimah, does not put Lebanon in a good position vis-a-vis its water needs.

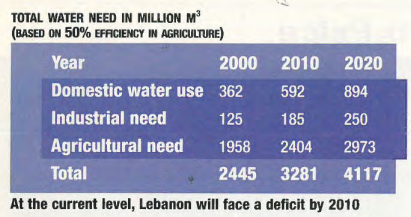

Nimah calculates that domestic water consumption this year will be approximately 200 liters per day per person, about 20% of the average daily consumption in the United States. Total annual consumption, therefore, will work out to be around 400 million m³. Add that to the industrial and agricultural consumption, and Lebanon’s annual water needs come out at 2,445 million m³. So, if Lebanon’s rainfall falls below average, it will suffer a water shortage. And since domestic use always receives priority, the shortage will hit agriculture the most. Out of the 250,000 hectares of arable land in Lebanon, only 90,000 are irrigated, which is ruinous to agricultural productivity. “Irrigated land is two to three times more productive agriculturally than rain-fed land,” says Nimah.

By 2020, Nimah calculates Lebanon’s total annual water consumption will be 3,555 million m³. Without any attempt to increase water supply, Lebanon will face water deficits each year.

So what is the solution? Lebanon needs to dramatically increase its ability to store water if it hopes to maintain a water surplus in 2020. Obviously, this will require large-scale investment in dams and water reservoirs. Less apparent is Lebanon’s decrepit and leaking underground piping network, which needs to be replaced. Chafic Abisaid, the director of the Barouk water authority from 1980 to 1990, says that the system loses up to 40% or 50% of its water load.

With new piping, the way water is distributed and charged for should also be changed. In developed countries, businesses and households pay for the amount of water they consume. But in Lebanon this is not the case. Instead of a meter, pipes connecting consumers to water are fixed with an orifice that adjusts the pipe’s water capacity, but does not record the actual amount used. The result is that your neighbor might consume twice as much as you, but still pay the same price. In addition to making people pay for what they use, the installation of meters would allow the water authority to apply different tariff rates for certain sectors of the economy.

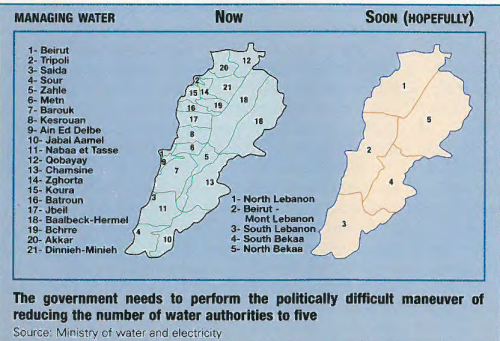

Besides the lack of funds, one of the major impediments to such obvious reforms has been the absence of any effective administration. In what must rate as one of the more ridiculous administrative follies the country has ever seen, Lebanon has 21 financially independent water authorities, a concept that goes against any idea of effective water management, especially in a country this small. For example, if there is a deficit in one authority and a surplus in another, there is currently no possibility of a transfer.

There was a decree in 1972 to reduce the authorities to five, but it was never implemented for political reasons, says Abisaid. “There have been too many beneficiaries,” he says ironically. “Every small water authority has its own board, its own director and staff. If you merge, a lot of people will suffer.”

In a January interview with EXECUTIVE, the minister of water and electricity, Suleiman Traboulsi, said the government is preparing for the looming water deficit. He is reviving the push for administrative changes, submitting a project to the council of ministers to eliminate the 21 different water authorities and reduce them to five, Beirut and Mount Lebanon, North Bekaa, South Bekaa, North Lebanon and South Lebanon. “These five authorities,” says Traboulsi, “will operate on commercial principles and will involve the private sector in administering their facilities.”

Reform of the administration is part of the larger project submitted to the council of ministers. Although short on details, the minister says the project, worth LL1.3 trillion ($867 million), will build dams and mountain reservoirs to ensure more than 2.2 million m³ after 2015 over a nine-year period. “This project,” says Traboulsi, “will be financed from the government treasury and not from foreign loans.” And he says this is not because of the difficulty of attracting funding. “It is our belief that within nine years we can secure the funds every year from the budget through a government decree called the ‘program law.'”

Governments are fond of large-scale development plans; they make good press. Completion and success of the plan is a different prospect, however. Besides the political difficulties of condensing 21 water authorities to five, Lebanon’s porous soil and mountainous terrain make large-scale dams and water reservoirs no easy task. It will take a committed ministry to secure the necessary funds and see it through.

The best-case scenario

Philippe Zgheib, an economist and professional hydrologist, is keen on water. With two doctorates in the field and a range of international experience, the Lebanese university professor has made water development issues the “passion” of his life. That’s beside, we assume, his expecting wife.

Given Zgheib’s approach to his work, he has chosen a suitably grandiose goal to pursue: nothing less than a multibillion-dollar integrated development of the region’s water resources. What is so exceptional about this? The area that we are talking about is the four points between Lebanon, Israel, Syria and Jordan.

Jordan, Israel and Syria all face severe water shortages, and in theory, an integrated development of the region’s water resources is the optimum solution to water shortages. The theory states that water, being a natural resource, does not adhere to national boundaries and therefore efficient management of the resource cannot be maximized at the country level. Instead, Zgheib says that to effectively develop the waters of one river, all the rivers in the region must be taken into consideration at the same time. Similarly, any water infrastructure, such as canals, dams, ducts, and pipe systems, has to accommodate all the water sources, not just one spring or river.

But pessimists, who always seem to outnumber optimists in the Middle East, believe the plan is wishful thinking. Even though most agree that an integrated development approach is best, they argue that the intractable grievances between the countries in question would make it impossible to join hands. Water resources, a lot of commentators say, have traditionally been a major source of conflict in the area, with no mechanism short of war being used to allocate the resource between countries.

But this year Israel and Syria are back at the negotiating table, with both sides interested in coming to a final settlement at last, a settlement in which questions over water resources will figure heavily. So perhaps it is time to give Zgheib’s plan more attention.

Although Zgheib can produce a lot of complicated figures to demonstrate the exact efficiency gains that would stem from an integrated development of the region’s water resources, understanding it is beyond this poor writer. But the basic plan makes sense. “My proposal,” says Zgheib, “goes beyond the country and looks at the resource regionally. Which means that I calculate all the water available in the region and compare that with all the demand, not by country, but by user sector: domestic, agricultural and industrial use.”

Second, instructs Zgheib, these needs would have to be factored in to population growth, which would change the level of demand for culinary and drinking water, agricultural and industrial water. Third, the development plan would need to prioritize these needs according to sequential use. This is water development speak for consumptive or non-consumptive use of water, the latter meaning using water in such a way that it does not change its chemical constitution. Industry, for example, uses water in cooling towers; the water used will rise in temperature, but its chemical makeup remains the same. Consumptive use, on the other hand, means that water undergoes a major chemical change, such as drinking water that comes out as sewage. By prioritizing non-consumptive use first, water supply can be magnified without tapping new sources since certain volumes can be used two or three times.

By looking at all the water demand and supply in this way, an integrated development plan could determine how to manage the water resources effectively. For example, it could determine what transfers would be necessary between countries and sectors to minimize shortages, calculate the infrastructure necessary to accommodate such transfers, the costs that would arise and hence what could be charged for the water in each sector.

Who would manage all this? Depending on a comprehensive peace settlement, Zgheib is envisaging some kind of supranational agency. Funded by member countries and international aid, the agency would have powers to attract financing, construct water infrastructure, impose operating and engineering rules, settle any disputes and establish and regulate a water market where users buy and sell water according to need. But given that water is a necessity for life, such a water market would have to operate under certain constraints. For example, Zgheib argues that this supranational agency would have to impose an “equity constraint,” meaning if there was a 10% water deficit in Syria’s agricultural sector, the same deficit should exist in the agricultural sectors of the other member countries.

And, says Zgheib, since Lebanon is the only country in the group with a current surplus in water supply, such a market could represent a business opportunity. One example that Zgheib uses is the Israeli predicament. The United Nations standard for the minimum amount of water each person must be secured for culinary and municipal needs is 90 liters a day; Palestinians currently have around 15 liters per person. “This is a time bomb for the Israelis,” says Zgheib. “They know that it will cost them less to buy water and give it to the Palestinians than to raise a policing army to deal with the potential instability, so they are ready to talk.”

Right now Israel could import water in floating medusa bags via ship or desalinate or build a sea pipeline from Turkey. The cheapest of these would cost at least $1 per m³. If Lebanon could supply water at a cheaper rate, Zgheib estimates that it could generate up to $2 billion in annual sales to the region, including Israel, a significant boon to the country’s huge budget deficit. But at its current level of development, Lebanon faces a water deficit by 2020. Perhaps Zgheib’s plan can be an added incentive to local authorities to get serious with improving water resource management in Lebanon.