On May 17, Lebanon was on top of the world. Literally. A Lebanese flag had been planted at the summit of Mount Everest, the world’s highest point. And what then, according to the Daily Star, did mountaineer Maxim Chaya do?

“He contacted his sponsor, Audi Bank, and thanked them for making his dream come true.”

Call it community outreach, or charity, or Corporate Social Responsibility. Banks’ logos can be seen in the sponsor’s position at athletic contests, concerts and art exhibits, and other cultural events around the country. And they also lend their support (and their brand names) to educational, environmental and development efforts.

Marwan Kheireddine, General Manager of Al Mawarid Bank, rejects the idea that publicity is the primary goal of CSR spending, at least for his bank. “The objective is not really exposure. The objective is community development.”

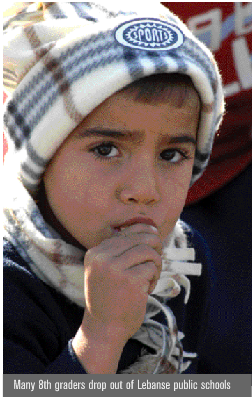

But Elie Azar of Lebanese Canadian Bank doesn’t see publicity as a bad thing. “When we opened our new branch in Halba,” he says, “we didn’t do an expensive advertising campaign. We gave away 180 boxes of food and provisions to the needy families there. These people were our best publicity.”

No bright lines

Azar does not see a bright line between a bank’s service to the community in its charity spending and its service as a commercial entity. “When we opened our branch in Hermel in 2003,” he says, “we were the first bank in the area, and we gave the people there access to a number of services they needed if there was going to be development, if they were to be able to stay there.” This value notwithstanding, the bank also contributed to a UNDP project bringing clean water to five hundred homes in the province.

This “both-and” approach informs another Lebanese Canadian Bank initiative. At the beginning of May they started to offer a unique loan program, offering loans of up to $5,000 at a 9% interest rate to homeowners in order to install solar water heaters in their homes.

“It’s a win all around for everyone,” says Azar. “The loans are profitable for us, and the customers save much more in heating costs than they pay over the time of the loan. And then you can add in that it saves the environment and reduces the pressure on our electrical and fuel infrastructure.”

LCB has been getting 5-10 applications a day for the loans. “This is the future,” says Azar. “If you look at the other countries in the region, in Israel 80% of the houses are using these heaters – in Greece, it’s 60%.”

In their more traditional CSR spending, Azar says, his bank concentrates on finding “effective projects that will have a positive impact.”

Relying on local knowledge

To identify the projects they wish to fund, banks rely on their local managers’ knowledge of their own communities.

“We work with each branch to discern the needs of each region,” explains Nahla Bou-Diab, assistant general manager of Al Mawarid. “The needs in rural areas are different from major cities. We have a branch in the village of Dmit, in the Shouf mountains. The community there are not well-off – their needs are for assistance in terms of developing a medical center – we helped them with basic necessities, schools, medicine, and so on. In another village in the Shouf area, the community were a bit more affluent, so in that particular area we designed a garden.”

Individual branch managers for Al Mawarid analyze the opportunities in a community and submit recommendations to the central branch. Some ideas come from formal or informal requests by NGOs or other organizations, and others come from the managers themselves. “Our manager in one area knew of a medical center that was crucial to the community – it was a poor area, and people were reliant on it every day. He knew that this center had a number of needs, and proposed to us that we help with them.”

Byblos Bank trusts its managers to decide on much of its educational spending. “In all the regions in Lebanon, our branches have a lot of schools as customers,” says Joumana Chelala, Senior Manager at Byblos Bank. “Our managers each have a budget to use towards educational needs, whether scholarships or something else.”

Banks are eager to get their employees involved. “Social responsibility is not just about contributing money to the community,” says Bou-Diab. “The other part that’s really essential is highlighting that these areas are really important in the eyes of management. One example of that was when we offered to match our employees’ contribution to St. Jude’s Children’s Cancer Care Center. We had 90% participation among our employees.”

“The salary structure in Lebanese companies is not very high,” she adds. “So these employees who contributed are not, financially, very very comfortable.”

The banks’ representatives show the pragmatism of a hardened loan officer in assessing their choices. Khaireddine says that Al Mawarid stopped funding concerts because “they were not doing anything for the community. We financed a few classical concerts in the Shouf, but the people who came, came at night, and didn’t even spend dinner up there. We felt like we were just making the events more profitable for the promoters.”

Chelala came to the opposite conclusion about cultural events, but arrived there by a very similar line of reasoning. Discussing her bank’s support for the Byblos festival, she says, “Before the festival, Byblos was not a destination for Lebanese. But now, even when the festival is not going on, many people from Beirut go up for dinner, or to visit the old souq.”

Focused on tangible outcomes

Perhaps because of their pragmatic approach, banks’ spending tends to be focused on tangible outcomes; medical centers refurbished or trees planted or schools equipped and teachers trained. Buzzwords common among the NGO community, like “civil society” or “dialogue,” don’t come up much.

“The private sector is becoming very active in supporting work in the environment, education, and so forth,” says Gilbert Doumit, who works both in education and in civil society areas. “Lebanon is well ahead of most Arab countries in this. But in more political, civil society, or citizenship-related areas, they are not so eager.”

To identif the projects they wish to fund, banks rely on their local managers’ knowledge of their own communities.

Education is a priority across the board. Kheireddine points to a library and computer training center near Shebaa. “We’ve taught people how to use computers there, and more importantly, we’ve given the young people there, right next to the Shebaa farms, access to the internet. Now they have access to the world.” Azar discusses a new library in Hermel. But it’s Byblos Bank that has taken on perhaps the most ambitious project.

Adopt-a-school

In a partnership with UNICEF, International College, and a large network of NGOs, Byblos Bank launched an “Adopt-a-school” project. The $200,000, three-year project, whose goal is to reduce the drop-out rates at a pair of public schools in Tripoli and Kesrouan, aims at attacking the problem from a number of different angles simultaneously.

There will be physical upgrades to the schools, especially to the bathroom and sanitation facilities. There will be training for teachers and administrators in identifying and helping children with special needs. But possibly the most important factor is literacy classes for the parents of children in danger of dropping out.

With an illiteracy rate as high as 20% in Northern Lebanon, children are “not given the support they need at crucial points in the curriculum,” says Roberto Laurenti, head of the project for UNICEF. “As the curriculum becomes more difficult, illiterate parents are unable to help those children who are already struggling.” As a result, the drop-out rates among 7th and 8th graders in Lebanese public schools are 9% and 11%, respectively, twice as high as at private schools. And once they drop out, they become vulnerable to any number of problems, from child labor to drugs and violence. “It costs much less to invest in keeping these children in school than to pay the social consequences later,” notes Laurenti.

“It costs much less to keep these children in school than to pay the social consequences.”

He emphasizes that all of the resources for the program, from expertise in training to monetary resources, are coming from within the country. “UNICEF is acting as a broker, bringing the people with the monetary resources in contact with the NGOs who can make use of them. We’ve been able to provide an opportunity to narrow the distance between financial and human resources in this country.”

The program differs from much charitable giving, Laurenti says, in that it is focused on dealing with a specific problem through a wide variety of needs, rather than on focusing on physical infrastructure. “We hope to see measurable improvement in the drop-out rate within a year and a half,” he adds.

This focus on a measurable outcome is a major step forward for CSR spending in Lebanon, says Isabelle Naoum, head of PR for Byblos Bank. “It helps us move towards a more formal CSR program, one where we can quantify the results of our action, and better fulfill our responsibility to our shareholders.”