Most businesses only dream of making millions each year.

So one would think that Cellis and LibanCell, dubbed

“cash cows,” would be content just counting up the earnings

from their build-operate-transfer (BOT) contract that was

signed with the government over five years ago. Cellis generated

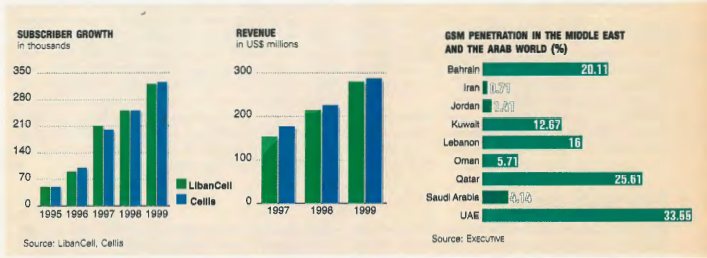

sales of $284 million last year, up from $225 million in 1998 when

it netted close to $37 million in profits. LibanCell made $42 million

in profits from a turnover of $279 million last year. Given the

rarity of such impressive earnings in Lebanon these days, who

wouldn’t want to be running a cellular operation?

But the operators have gripes. That’s because the BOT contract,

though guaranteeing money in the bank, has kept constraints on

growth. The operators are trying to get a license, which would give

them greater freedom in running their business. Ultimately that would

mean a healthier expansion of the market and greater revenues.

The essence of the contract is that the government collects a share

of every cent LibanCell and Cellis make, without investing a

penny. The operators’ networks are the property of the state,

which explains the condition in the BOT specifying the construction

of a network for a minimum of 250,000 users. The government

gets a 20% share of revenues, including those generated from the

connection fee, the monthly subscription and talk-time. In addition,

there’s a 10% municipal tax on each bill and a 6-cent tax per minute,

which was raised by the ministry of post and telecommunications

(MPT) last July. Revenue from international calls and the use of

landlines also go directly to the MPT because of its monopoly. In

total, the government cashes in 40% of all cellular proceeds from

each company, according to LibanCell. That of course is on top of

the 15% corporate tax that firms pay.

To ensure financial gain, the contract dictates the connection fee

at $500, the monthly charge at $25 as well as talk-time rates. It

exempts extra services, such as voice mail and call waiting, from

taxation. The operators argue that fixed prices and taxation

impede the normal growth of the cellular market. Following the tax

hike last year, demand has slowed and talk time has shrunk by about

10%, according to Sima Hafez, the marketing manager of Cellis.

The two companies have the market split down the middle,

give or take a bit, with about 320,000 subscribers each. Hafez

explains: “There’s no difference in terms of pricing [on permanent

lines]. And the [area] coverage, as specified in the contract, is the

same. So definitely we share the same number of subscribers.”

Customers buy whichever cards are available, because prices are

the same. “There’s no rational selection,” says Magda Sacre,

commercial manager for LibanCell.

Neither company is happy with the situation, despite the impressive

financial gains. They want their freedom. “Lebanon is a competitive

market,” says Hussein Rifai, chairman and general manager

of LibanCell. “We have to be able to compete; we have to get the

freedom of pricing.” Licensing would give them that as well as ownership

of the networks. Salah Bou Raad, chairman and CEO of Cellis,

explains that the government retains ownership of “airwaves,”

which it leases out to operators. He adds that licensing would further

allow the company to float shares on the Beirut Stock Exchange.

Growth has also been hampered by the ongoing fight over the permissible

number of subscribers (see “The government’s thirst for

more,” October 1999). The MPT’s attempt to impose a ceiling of

250,000 is disputed – and already surpassed – by both firms.

Also, a technicality with the numbering system on cellular lines means

the operators will max out their subscriber base at 400,000

each, which is expected to be reached by year-end.

But why all the fuss about licenses now? The answer may lie in

the unforeseen growth of the cellular market. When they were mining

for coal, they didn’t expect to strike gold. “We had to re-think

our investment strategy,” says Rifai. “We didn’t forecast such subscriber

growth and talk time, and so we had to increase our investment quite a lot for the first year.” Both LibanCell and Cellis have

doubled their subscriber bases each year in the first three years (see

graph). The MPT has received over $700 million in the past four

years, already coming close to the $800 million that was initially

projected over ten years.

But the operators claim the market could grow even more in a competitive

environment. The proof is the boom that followed the prepaid

cards. They were first introduced to the market in September

1997 by LibanCell. In just three months, the Premiere cards doubled

LibanCell’s customer base, from 110,000 to 210,000. “They

launched the cards before us at very cheap prices,” Hafez says. “We

were hurt by this offer, and we were losing our customers. We had

to compete. That’s not a duopoly; that’s real competition.” In

December of the same year, Cellis launched its Clic cards to recover

market share. The prepaid cards proved successful, mainly

because they had a wider reach to consumers with limited income.

And that allowed the companies to tap into a new market.

In its fever to bring in funds, the MPT is drawing up plans for a

state-run operator, under the umbrella of privatization. If it does,

the existing operators might get licenses. Otherwise the MPT

would be in breach of the BOT contract that grants exclusivity until

2004, though that could be extended if the agreement is renewed.

The MPT refused to comment on the matter because negotiations

are ongoing. The ministry is considering the options based on its

main objective of pulling in cash, according to one source. Three

meetings have taken place, which are thought to be positive. “All

parties involved want to reach an agreement fast,” says Bou Raad.

A third player would help spur competition. “Will that competition

drastically bring prices down? Competition normally brings

prices down,” Hafez says. “Any normal operator will grab a share

of the market when they enter and then they’ll grow. They might

undercut prices by, say, 10% to get part of the market.” Lower prices

should translate into an increased customer base. Needless to say,

that would benefit customers most. “Increased competition is

always good for the consumer,” says Bassam Yammine, senior manager

of the Corporate Finance Division at Lebanon Invest. “[It

would lead to] possibly lower prices and better services.”

Currently, customers have little choice. They’re the ones who have

full license to complain, really. Take for example the tax hike on

talk time – simply a way to bring in more funds. Compared to the

European average of 150 minutes, talk time in Lebanon is at least

700 minutes a month per person. The equivalent monthly bill for

a subscriber to a permanent line, making local calls only, would be

over $80, excluding taxes and extra services.

Regardless of whether the Lebanese ought to be condemned for having

a mobile phone glued to their ear, the cellular is a worldwide trend

that will continue to grow. Without the constraints of the BOT,

growth could be huge. Rifai estimates a penetration of 35% in the

next five years, a consensus shared by Hafez. She estimates that by 2004,

the number of cellular subscribers will go up to 1.4 million, more than

double the current level, which is roughly 17% of the population.

If privatization and the introduction of a third operator are

delayed, what are the chances of the operators getting licenses when

the contract expires? It’s not clear at this stage. The operators maintain

that licensing would increase government revenues. On the

other hand, the BOT allows the government to increase its share of

revenues to 40% in 2003 and 2004, and to 50% beyond that if

renewed. The MPT might not be eager to loosen the reins on its cash

cows. Unless it draws a good bargain, that is.

Top of Form

Bottom of Form

Two steps ahead

Both LibanCell and Cellis have plans to get into the new trend

sweeping Europe: the merging of Internet and wireless

technologies. Locally, LibanCell might have an advantage

because of its sister company, Internet service provider

TerraNet. “We will definitely have cooperation. We’re working on

providing Internet access to our subscribers,” says Hussein Rifai,

LibanCell chairman and general manager. Cellis, 67% owned by

France Telecom, might be able to bring in Wanadoo, the ISP

subsidiary of the French telecom. Speaking of innovation, both

operators have plans this year for mobile banking (M-banking) and

similar services, especially for their corporate clients.

Wireless Internet has just taken off in Israel. A joint venture,

GoNext, was formed between mobile phone company

Pelephone and Samsung distributor Sunny Electronics with a

$200 million investment. GoNext will enable clients to surf the

Internet in the HTML language and the Wireless Application

Protocol (WAP), especially developed for cellular phones.

Mobile Internet could well take off in Lebanon, as it is expected

to in Europe this year, since the number of cellular users locally

surpasses the number of Internet users by at least six times.

Also, cell phones are cheaper to own than computers. The question

mark remains for access prices.