In October 2019, following years of dysfunctional public policies, Lebanon entered the vortex of an unprecedented collapse. This was evidenced by, among other indicators, a further dramatic decline in economic growth rates, exceptional primary deficits and a negative balance of payments, a banking sector in crisis, and the emergence of a parallel foreign exchange (FX) rate in a country that imports most of its consumption needs. The increase in consumption prices is one of the most revealing indicators of these structural dysfunctions, and one of the most influential on the lives of the country’s residents—the majority of whose salaries are in the national currency.

Using the Consumer Price Index (CPI) of the Consultation and Research Institute (CRI) consultancy firm, which has been issuing a monthly CPI for Greater Beirut since 1977, we have predicted the inflation trend over the medium term. (The CPI was the only inflation indicator in Lebanon until the Central Administration of Statistics began issuing their own in 2000; the two indexes record similar trends but are not identical as they weigh various expenditure categories within a typical household budget differently.)

Increasing inflation

Based on the trends recorded by the CPI over the past few months, several conclusions and warnings over future expectations can be drawn.

Firstly, the emergence of a parallel FX rate in October 2019 resulted in a price increase across several major items of the Lebanese consumption basket, in particular food items (see infographic below). The CPI, however, as it includes around 1,000 products and services, only began to increase in December 2019. The yearly price increase (a comparison of the CPI for each month of 2019 with its equivalent in 2018), remained either flat or negative for the first eleven months of 2019 (due to the stability of the peg until October last year).

Starting in December 2019, the CPI began to increase compared to the year prior, rising by 4.6 percent in December, 8.7 percent in January, 11.4 percent in February, and 13 percent in March (see graph below). More alarming was the sharper increases in the price of food items on year-on-year comparison, which rose by 3.1 percent in December, 10 percent in January, 16.8 percent in February, and 20 percent in March. In other words, the marked increases in food prices (weighed at 30 percent of expenditures in the CPI), which constitute a high share of the expenditure budget of low-income households (30 percent if not more for the lowest income households), have been the main driver behind the CPI’s increasing trend over the past few months.

The relative delay in the impact of the exchange rate on consumption prices following October 2019 (see graph below) could be explained by the following factors: 1) The government’s commitment (through Banque du Liban) to subsidize the import of fuel, medication, and wheat, which constitute a major share of the consumption basket (fuel 3.03 percent, health 9.8 percent, and wheat 3.6 percent); 2) the stability of public fees and taxes, and the relative stability of housing prices; 3) the volatility in the price of vegetables; 4) the repercussions of the economic recession reflected in negative growth rates since 2018, which drove a number of importers and wholesalers to prioritize clearing their inventories, at least in the short term, by keeping their prices stable despite the devaluation of the lira on the parallel exchange market.

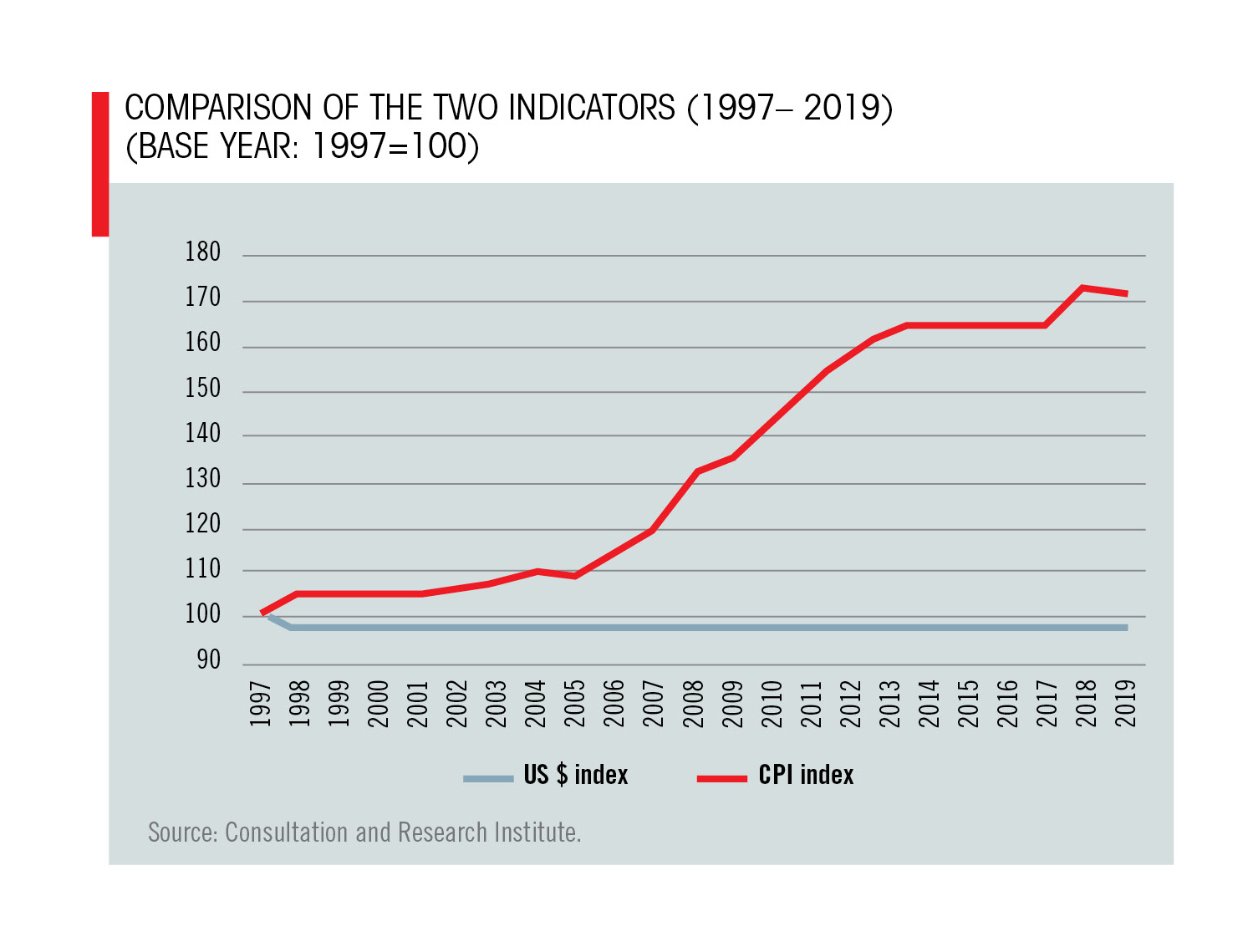

Lessons from the past

The most important point, however, is the lesson that can be drawn from the historical relationship between the CPI and US dollar exchange rate trends. Based on CRI’s database, the yearly CPI curve remained consistently above the exchange rate curve from the mid-1970s until the mid-1990s, when the lira peg was put in place (with a limited exception in 1985-1987). Interestingly, after the inauguration of the peg, the gap between the two curves continued to widen year after year, despite the stable exchange rate (between LL1507 and LL1515 to the dollar). The trend is reflected in the demands of the Union Coordination Committee for a 121 percent wage adjustment to compensate for the accumulated inflation between 1996 and 2012, a period during which the US dollar exchange rate remained completely stable as a result of the peg.

The three graphs below show the trends of these two indicators during three distinct periods that could not be merged into one graph as a result of the 4,800 times increase in the CPI between 1977 and 2019. The first period, which extends from 1977 to 1985, was characterized by relatively moderate differences between the two indicators, with the exchange rate curve catching up to the CPI curve in 1985.

The second period, between 1985 and 1997, witnessed a closing of the gap between the two curves in 1985-1988, following which the CPI curve took off on its own while the exchange rate curve began to decline as of 1993 (this was aided by factors such as the expected increase in prices after the war due to the spring effect, multiple wage adjustments in the early 1990s, and the beginning of a descending trend of US dollar versus Lebanese lira when Rafik Hariri became prime minister in 1992).

The third period, extending from 1997 to 2019, was characterized by a widening of the gap that began in the second period, as the CPI continued its upward trend despite the quasi-absolute stability of the dollar exchange rate.

These observations clearly show that the increase of the cost of living in Lebanon over the past four decades was not only dictated by the lira/dollar exchange rate (despite the importance of that factor). Rather, it was also, if not mostly fed, by factors that are deeply rooted in the Lebanese economic model. Specifically: 1) the domination of import and internal markets by cartel groups, as a result of the absence of effective anti-trust regulations and an ambiguous commercial representation statute that has strengthened these cartels; 2) the exacerbation of distortions in consumption prices and the exchange rates of non-US dollar foreign currencies, as a consequence of the implicit monetary stabilization policy after 1992 and the explicit stabilization policy after 1997, which encouraged imports and undermined the competitiveness of domestic exports; 3) the transformation of Lebanon into a consumer country (since the onset of the 1990s and accelerating from 2011) that finances its consumption through remittances and domestic and foreign borrowing (according to Lebanon’s National Accounts, private and public consumption exceeded the country’s total GDP in 2018); and 4) the weakness of consumer protection laws and regulations, especially those related to controlling monopolies and fostering competition, in addition to the low effectiveness of price control authorities and mechanisms that are currently solely reliant on margins of profits (as they are now in Ministry of Economy and Trade regulations).

Warnings for the future

If we were to assume that the trend that has governed the relationship between the exchange rate and CPI curves over the past 40 years would remain unchanged, then we must raise an alarm regarding the potential of this relationship in the future. Based on the historical trends, what we are seeing now in terms of price increases failing to catch up to the rising exchange rate is only temporary and we should therefore expect the gap between the two curves to gradually begin narrowing. It is even likely that the consumption price increases may exceed exchange rate increases, which would have horrific consequences for the savings, wages, pensions, and purchasing power of the Lebanese people, especially if the needed public interventions do not materialize in view of the economic, fiscal, banking, and currency crises. Specifically, what is needed is macroeconomic adjustment, financial and monetary reforms, reform of the fiscal system, restructuring of public expenditures, independence of the judiciary, and accountability and the recovery of the stolen funds.

The interventions required to stave off price increases go beyond currency, fiscal, or regulatory measures that only serve to address the symptoms rather than the causes of inflation. The first step consists of regaining the trust of the people in their country, their economy, and their independent judiciary, through the immediate fulfillment of the just demands raised by the popular uprising, namely the enforcement of an effective national rescue and recovery plan starting with taking concrete steps toward the recuperation of stolen or wasted public funds, reform of taxation system, a restructuring of public expenditures, and laying the groundwork for the revival of productive sectors, in addition to addressing the root causes behind persistent primary deficits, public debt, currency devaluation, and banking collapse. This plan would focus primarily on investment in infrastructure, fostering productive activities, the creation of decent jobs for graduates and unemployed youth, and the elaboration of a comprehensive social development and protection strategy that addresses the needs of the poor as well as lower and middle-income households in a country that is characterized by staggering income inequalities.