Fear and panic drove the markets through most of August causing more than $4 trillion in wealth destruction, while policymakers responded with “soft patches” and short-term solutions to what are structural and fundamental sovereign-debt problems on either side of the Atlantic.

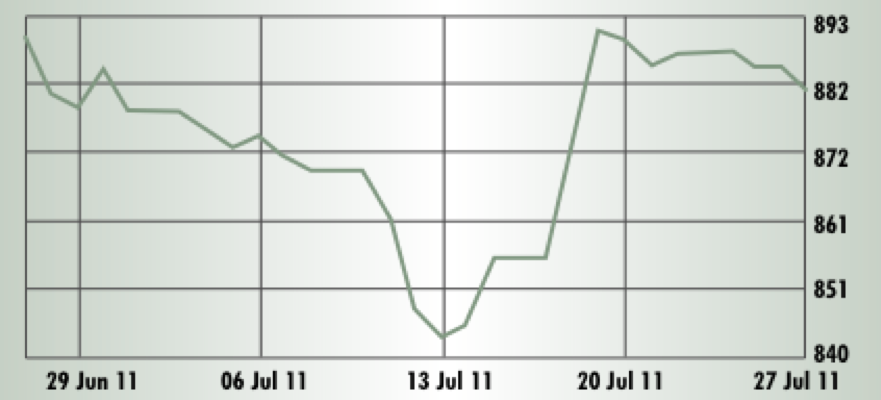

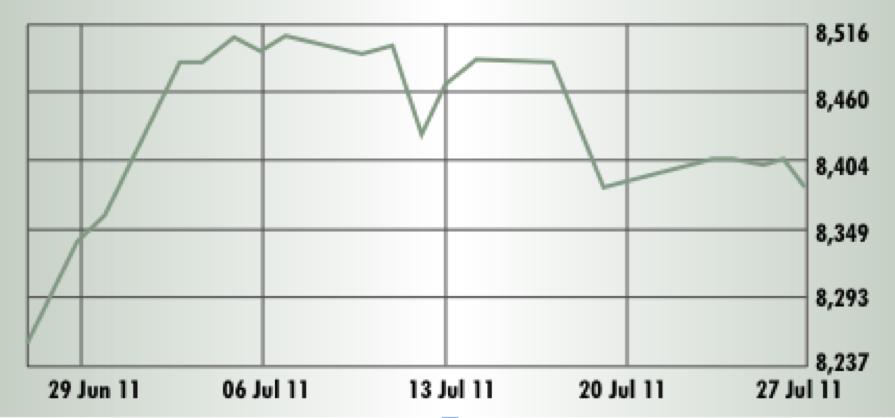

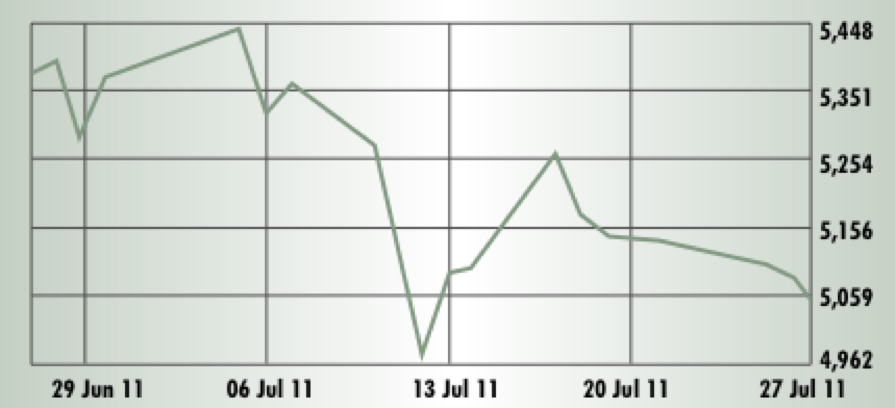

During the week of August 8 the S&P500 — best single gauge of the United States equities market — went on a roller coaster ride, closing consecutively at -6.7 percent, +4.7 percent, -4.4 percent, +4.6percent, and +0.5 percent. While choppy and erratic, both American and European equity markets began a four-week downward near the end of July, with the heightened risk of a recession prompting investors to dump risky assets and seek safety in the Swissie (CHF), gold and in long-dated US Treasuries, in other words, there has been a general flight-to-quality.

Thus, the concern today is how to trade equity and foreign exchange markets, and hedge against potential event risks until the politicians and central bankers provide durable solutions to exit their debt conundrums and correct economic imbalances.

Approaches to equity and FX

Nouriel Roubini, also known as “Dr. Doom” for having predicted the 2008 financial crisis, recently told me that he assigned a “50 percent probability to a double-dip scenario… Or possibly more.”

For investors sharing this “doom and gloom” view, outright put options on US or European indices would make sense, if not shorting the indices directly. Since implied volatility hasn’t reached the 2008 and real crisis levels, protection is still cheap and below fair price if you calculate that the worst is yet to come. The put protection provides an attractive way to limit the downside, or potential losses, to the put premium if you happen to be wrong. If such structure is not affordable, an investor could play the correlation card — given that in times of global meltdown correlation tend stowards one, meaning the markets move in sync — and buy a best-of-put on a global basket where the index that will fall the least will still drop considerably in broad-based sell-offs.

Turmoil in the S&P

Source: Standard & Poor’s

In the world of foreign exchange, investing in quality assets would protect from event risks, with possibilities including buying a barrier option for a targeted move in the USD-CHF rate, or play the Norwegian NOK if investors fear interventions from the Swiss National Bank (SNB) to control the appreciation of the Swissie.

The second group of investors — the bears — assign a lower probability of dramatic worsening of the sovereign crisis, but still believes that uncertainty will dominate markets. Even the fixed income markets in the Eurozone are pricing in a deeper debt crisis with Italian and Spanish 10-year yields flirting between 6 and 6.5 percent — that is until the European Central Bank decided to resume bond purchases — and more alarming, the Greek 2-year yield hitting 46.6 percent on August 25.

“Markets won’t give the benefit of the doubt [to theEurozone] until the results of policies to correct imbalances in public and private sector balance sheets as well as current accounts, and the new policy infrastructure, are visible,” highlights Mark Wall, managing director and co-head of European Economics at Deutsche Bank. “It is a ‘muddle through’ and as such markets don’t like it.” With this bearish view, buying (bear) put spreads on indices, for example, is a better alternative to outright puts —given the cheaper structure — as investors are willing to limit the upside, or potential gain, below the first strike.

A third and quite diverse group — the bulls — argues that the market has allegedly discounted the turmoil in the US or potential selective default in the Eurozone, with policymakers close to providing solutions; the more extreme ones even believe that ‘everything is a buy at current levels’. These investors are betting on this rally starting soon — and on a more inflationary world — and would rather buy call options on indices, for example, staking their money on the upside. Once again, this group covers a large spectrum and is quite hybrid, as being bullish does not necessarily entail being bullish on all markets.

If an investor bets on a faster resolution to economic imbalances in the US on the basis that the US has better fiscal tools at its disposal to solve the debt crisis, one could combine longs in the S&P 500 with shorts in E-STOXX50. This view can also be played through the FX market, and particularly the euro-dollar.

“As the ECB begins to aggressively accumulate Eurozone bonds— out of necessity — and overall risk appetite grows disappointed with any stimulus from the Fed, the euro-dollar is likely to make its way towards the $1.40 figure,” explains Ashraf Laidi, chief executive officer of Intermarket Strategy Ltd and author of Currency Trading & Intermarket Analysis. “The most important support remains $1.37, a break of which would flood the gates towards further downside.”

Last but not least, a growing group — the ‘risk off’ investors — would rather sit-and-wait. These investors do not wish to actively trade in these markets given the excessive uncertainty and irrationality; they prefer to dump investments across a spectrum of assets and sit on their cash, with the idea that “being flat is the new high.”

Taking a view

Looking at the divergence in trends between the end of July and what seems like a start of rally in equities and correction in quality assets during the last week of August heading into ‘Jackson Hole’ — the annual US Federal Reserve (Fed) symposium — it would seem that the irrationality of markets was more due to panic, a lack of liquidity (with many investors on holiday), day trading and market positioning, rather than to sensible trends. Either way, it seems that markets are largely untradeable, at least until we get more clarity from policymakers.

And yet, the investor has to do something, but what? Is ‘off risk’ the only logical option? The reality is, liquidity has been poor this summer and volatility high, so the investor can make the same amount of money with less notional than in a low volatility environment.

Thus in order to work out how much to put in, the real questions should be: What opportunity does the investor seek and how much does he want to make? Does the investor want a ‘high risk/high reward’ portfolio —investing in the banking sector like Warren Buffett’s recent $5 billion bet on Bank of America — or a portfolio with lower volatility, such as one with investments in the utilities sector?

Whether a sector, single-stock or asset class approach, investors must take a view, but one in search of what has been oversold and depressed, or conversely overbought and overvalued, rather than rushing into safe haven currencies, gold or US Treasuries. In short, it is more sensible to bet on assets trading under or above ‘fair value’ rather than invest blindly in ‘safety’ — value over quality.

NATACHA TANNOUS is EXECUTIVE’s financial correspondent