Condolences to Solidere shareholders. Profits of the real

estate company, responsible for rebuilding the Beirut

Central District (BCD) and the largest business in

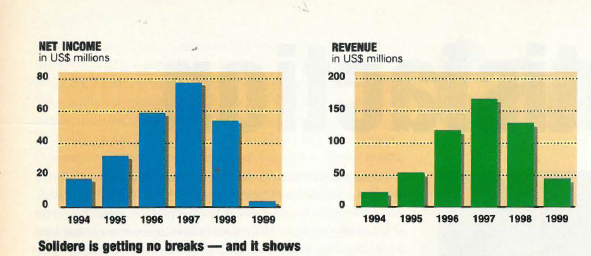

Lebanon, plummeted from $54.2 million in 1998 to $3.7 million

last year. That’s a 93% free-fall! It won’t be decided until June,

but you can bet your shorts that Solidere won’t pay dividends this

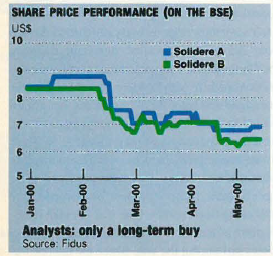

year. Share prices have more than halved since peaking in

1997. This year alone, Solidere’s A and B shares traded on the

Beirut Stock Exchange (BSE) have dropped more than 22%. Its

market cap, which takes up nearly 70% of the BSE, has shrunk from

$1.4 billion to $1.1 billion in the last 12 months. Expecting bigger

and better things in the near future? You may have to wait.

Land and real estate sales, the company’s main source of revenues,

fell 68% in 1999, from $118 million in 1998 to $37.5 million,

according to Solidere’s finance division manager Mounir

Douaidy. Sales contracts worth $79 million that were supposed to

come through last year were either cancelled or postponed.

Douaidy points to three factors contributing to Solidere’s dramatic

decline in sales: the stagnant economy, investors’ jitters about

political uncertainties and the snail’s pace of building permits.

There’s no doubt that Solidere isn’t immune to the economic slowdown

and political uncertainties. But according to Ziad Maalouf, vice

president at Middle East Capital Group (MECG), if there is economic

recovery or a peace agreement, the permit problem would keep a lid

on Solidere’s progress. “Why would a developer come and buy land

in Solidere when he knows that he’ll run into massive delays?” says

Maalouf. “Holding back permits is paralyzing Solidere 100%.”

The problem begins with the differences between the old construction

code and Solidere’s building decree 4830, which was

passed in 1994 for the purpose of rebuilding BCD, according to

Oussama Kabbani, department manager for urban management at

Solidere. “In principle you only have to pass through 4830, but it

doesn’t cover every detail,” he says. “Whenever the decree doesn’t

cover something, the municipality of Beirut goes back to the original

code. You’re using two laws that in principle should complement

each other. But when found in the grey zone, they apply the

old one and suddenly there are discrepancies.”

He claims that the

government was more flexible with 4830 under the old regime. But

things have changed under this administration. “When discrepancies

are found, nobody wants to take responsibility,” says Kabbani.

George Khouzami, head of the engineering department at the

municipality of Beirut, admits that his team is running into discrepancies

that delay the permit process but denies that the change

of government has altered the way the municipality works. “During

the previous government, we never bypassed the law,” he says. “We

followed the law then as now.”

But talk to anybody related to rebuilding downtown and they’ll tell

a different story. What motivated the powers-that-be to alter the process

is anyone’s guess. Analysts argue that there is an anti-Hariri campaign,

since he was the mover-and-shaker for Solidere while prime minister

and is a major shareholder in the company. Some at Solidere believe

that this government’s drive for law and order has forced those

working with permits to follow the rule book down to every detail.

“The government said that everybody must follow the law, so suddenly

everybody started getting scared,” says one Solidere official.

“Everybody says that it’s not their responsibility and throws the ball

in a different direction.”

Some developers and consultants that have

had a hand in the rebuilding program since the beginning have a different

theory and don’t sympathize with Solidere. “I feel sorry for the

developers that bought land and have permit problems, but not for

Solidere,” says one developer. “Solidere used to be the government,

it had power and it had a free hand in doing what it wanted to do. There

used to be pressure on the municipality. Now those at the municipality

are fed up with Solidere and are taking revenge.”

Regardless of who’s at fault, the government has stepped in to

offer a little help by passing two decrees. One was to make it easier

to get occupancy permits that were on hold because legal documents

had been destroyed during the war. Since the decree was implemented

in mid-February, only five permits have made it; 30

are pending. “Not good enough,” says one Solidere official.

The

second decree created the high council of urbanism to deal with discrepancies

found by the municipality. But according to Kabbani,

the council was given limited power. “In some cases there are five

problems, and the council can only decide on three, not the rest,”

he says. “We thought the council would get things rolling, but we

get stuck again and again.” Since the decree emerged early this year,

no construction permits have been issued — 24 are pending.

Since these decrees are merely patchwork, Solidere is anxiously

waiting for five more. One is supposed to clean up the discrepancy

mess. But there’s a problem: The council is only supposed to last

for six months, so it will expire in three. Watching how slow the

decree is moving, Solidere expects it to take one to two years to be

finalized. (It’s already been sitting at the Council for Development

and Reconstruction for over four months.) “They will probably

extend the council,” says Kabbani. “It’s better than nothing.”

Also critical are the souks. “It’s the vital part of BCD,” says

Douaidy. “It will energize the atmosphere, draw commercial life and

create traffic, which will bring in more investors.” With the souks

including 20,000m² of office space, 10,000m² of residential units and

70,000m² of retail space, not only would it bring in a new, healthy cash

flow from sales and rental income, but it could trigger a domino effect.

A decree to let Solidere develop the souks has been approved all the

way up to the last chain of command: the council of ministers.

According to Solidere, it has been waiting for the final signature for almost two

months.

The new decrees, which include dealing with the marina and property

given to government, are not only important to

Solidere. Those who have invested

in the BCD have been caught

in the crossfire.

“We are worried about how long it will take for the

decrees to be passed,” says Essam

Makarem, speaker for a group of

investors in BCD. “We’ve already

invested around $500 million in the

land, with another $1.5 billion in the

banks ready to invest; all we need is

to be sure that the other five decrees

are passed by the government.”

Is Solidere in a position to withstand

the outside forces if they continue to drag on? “Their fundamentals are

still sound,” says Maalouf. “The company is healthy in terms of financials.”

He notes that Solidere is sitting on $77 million in cash, its debt-to-equity ratio stands at an

acceptable level (22%), most of the infrastructure projects are nearly

completed and even though its net interest earnings have decreased

over the years, they’re still in the black. “And the land Solidere is sitting

on is strategic land, prime real estate, and its value can only increase

over time,” says Maalouf. “It’s a strong fundamental.”

Solidere is taking precautions to weather the storm. By downsizing

(mostly by reducing its staff by over 30%), general and administrative

expenses dropped from $16.4 million in 1998 to $14.3 million last year.

Cost cutting will mostly be felt this year, with Solidere aiming for

expenses to hit $10 million.

It has had plans to generate a new income

stream through rental income to help offset slow sales (see “Hedging

its bets,” July/August 1999). But with no substantial contracts developed

last year, its main source of rental income is still the ESCWA building —

rental revenues inched up only 0.5% ($6.9 million).

The Saifi project,

set up with an option to lease or buy, will be completed by the end

of the year and has booked 55% of space available. With Solidere’s aim

to increase its rental revenues, according to HSBC’s latest report, it will

climb steadily to reach around $19 million in 2002.

There’s also a backlog

of land and real estate sales amounting to $49 million that could

come through this year. But with the permit problem, Saifi’s results not

showing up on the books until 2001, and, most importantly, not

knowing if contracts for land and real estate will come through, it’s difficult

to predict if Solidere will show profits this year.

With economic conditions stagnant, uncertainty about the

peace issue and the permit problem dragging on, HSBC and

MECG recommend “hold” on Solidere’s shares. Some investment

firms have pulled back and stopped giving recommendations, not

knowing where the company is heading. “There are too many variables,”

says an analyst at the Merrill Lynch branch in

London. “We have to wait until things are clear before we can present

our view again.”

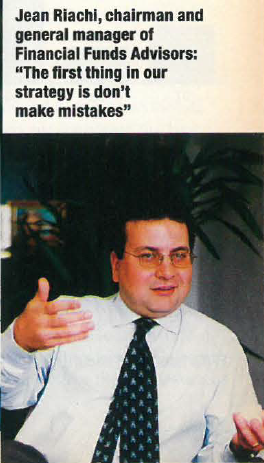

But analysts still believe that if there’s peace, Solidere’s shares will

jump. “The share prices will shoot up if there’s peace,” says Jean

Riachi, chairman and general manager at Financial Funds Advisors.

History offers some support: When peace talks were temporarily

revived a year ago, Solidere’s shares had a quick rally.

But if there is peace and the permit problem remains, the flurry would

probably lose momentum. What is needed is the government to grease

the wheels of Solidere; otherwise, it will just sit there idling