The global picture

This month the world will mark 20 years since the fall of the Berlin Wall — on November 9, 1989 — and the end of the Cold War. With the doomsday scenario of (nuclear) World War III less likely, people around the globe had high hopes for an era of peace and prosperity, including a decrease in military spending.

Following decades of military build-up in the United States, the former Soviet Union and both of their allies, military budgets did indeed decrease, albeit not for long. Over the past decade, military spending has gradually regained lost ground, reaching record levels last year.

According to the Stockholm International Peace Research Institute (SIPRI), global military expenditure in 2008 amounted to $1.46 trillion, which represented an estimated 2.4 percent of global GDP in 2008, and a 45 percent increase since 1999. Why?

The US leads the pack

“The idea of the ‘war on terror’ has encouraged many countries to see their problems through a highly militarized lens, using this to justify increased military spending, while the wars in Iraq and Afghanistan have cost $903 billion in additional military spending by the US alone,” said Sam Perlo-Freeman, head of the Military Expenditure Project at SIPRI. The US remains the world’s largest military spender.

The 2008 national defense budget amounted to $516 billion, or 42 percent of the world total, not including the $194 billion spent that year on the wars in Iraq and Afghanistan. Over the past decade, US spending increased by $219 billion, which represents 58 percent of the global increase. US Defense Secretary Robert Gates proposed a 2010 military budget of $534 billion and a reduced $117 billion budget for Iraq and Afghanistan.

The US is followed at some distance by China (8.2 percent of global military spending), Russia (4.75 percent), the United Kingdom (3.75 percent) and France (3.67 percent). China and Russia increased military spending over the past decade by $42 billion and $24 billion, respectively. Other major budget increases also occurred in India, South Korea, Brazil and a number of Middle Eastern countries, including Israel, Iran, Kingdom of Saudi Arabia (KSA), the United Arab Emirates, Algeria and Oman.

Untransparent military budgets

KSA remains the region’s top spender, increasing its 1998 military budget by 61 percent to $33 billion in 2008. The kingdom is followed by Israel ($13 billion), Iran ($6.1 billion), Oman ($4 billion), Kuwait ($3.6 billion), Egypt ($2.6 billion) and the UAE ($2.5 billion). Considering that most countries in the Middle East have no arms industry to speak of, their share of the global arms trade is relatively high.

Military spending includes everything from soldiers’ pay and building maintenance to the actual acquisition of arms. The media often tend to confuse overall military spending with arms acquisitions.

“Many countries with lower levels of transparency do not even include arms imports in their military expenditure figures,” said Perlo-Freeman. “This may well include many Middle Eastern countries. In most cases the only data available for the military budget is a single figure, so it can be hard to relate military budgets to arms import trends. Also, official budgets often leave out quite a lot, not only arms imports. Iran, for example, does not include the Revolutionary Guard’s budget and the UAE budget does not include spending by individual Emirates, which is believed to be quite significant.”

One thing is certain: regional military spending will not decrease any time soon. In August, American research firm Sullivan & Frost concluded that the region’s military budgets are likely to break the $100 billion mark by 2014, amounting to 11 percent of global spending, compared to 7 percent today.

While most Middle Eastern countries are not among the world’s top spenders in absolute figures, they are top of the bill when military spending is defined as a percentage of GDP. The regional average is twice as high as the global average of 2.4 percent. The Middle East also scores high in terms of military spending per capita. Israel tops the global list with some $2,300 per inhabitant, followed by the US ($1,950), Oman ($1,650), Singapore ($1,625), Kuwait ($1,600) and KSA ($1,500).

It may come as a surprise to see Oman among the top spenders. The sultanate significantly increased its military budget from $1.7 billion in 1999 to $4 billion in 2008. The reasons are the same as elsewhere in the region: strategically located on the Strait of Hormuz, Oman fears Iran’s alleged nuclear and regional ambitions, as well as the fall-out from a potential US-led attack on Iran. It remains to be seen if the Iranian threat justifies the region-wide splurge in military spending.

Top 15 countries by military spending per capita

The regional arms race

British Typhoon combat jets to KSA, German Dolphin submarines to Israel, American Patriot defense missiles to Israel and the UAE, American F-16 fighter jets to Turkey, KSA and the UAE, and state-of-the-art American F-35 fighter jets to Israel: these are just a few examples of the military hardware coming the region’s way as part of a multi-billion dollar arms race. The Middle East has long been a lucrative market for international arms manufacturers, and will arguably remain so for many years to come.

“Predictions about the future volume of arms transfers are difficult to make, as good information is hard to get,” said Pieter Wezeman, a SIPRI senior researcher on international arms trade. “Still, known information about existing orders, and orders being negotiated, indicate that several countries will maintain their level of arms imports in the coming years.”

One major growth market will be Iraq, which is expected to increase its military spending, including arms imports, as the US army is set to increasingly take a back seat. Yet, it will take some years before Iraq will come anywhere near the region’s traditional big spenders on arms: KSA, Israel, Iran and, to a lesser extent, the UAE and Egypt.

“KSA buys everything from new German rifles to British combat aircraft, and possibly more aircraft from the US,” said Wezeman. “Some weapons are getting old and are ready to be replaced. In other cases weapons are procured, which arguably add to existing military capabilities. For example, the procurement of new and upgraded combat aircraft armed with cruise missiles will give KSA, at least in theory, the capacity to strike targets at a long range, in some ways creating a counter deterrence to Iran’s ballistic missiles.”

KSA and its allies, as well as Israel, view Iran as the main threat to regional stability, which, as such, functions as the main catalyst in the current Middle East arms race. Naturally, their concerns were not exactly reduced when the Islamic Republic in recent months test-fired a series of long-range Sijil and Shahab III missiles, whose range extends as far as Tel Aviv.

Partly with the aim to counter Iran’s ballistic threat, KSA in 2007 bought 72 Eurofighter Typhoon jets from the world’s second largest arms manufacturer, Britain’s BAE for an estimated $9 billion. The British Ministry of Defense hailed “Project Salam” as a “new chapter” in Saudi-British relations, which arguably referred to the cloud of corruption that accompanied the massive 1980s Yamamah arms deal. It speaks for itself that the $9 billion “peace project” will be spread over the kingdom’s annual military budgets for many years.

One major growth market will be Iraq, which is expected to increase military spending, including arms imports, as the U.S. army takes a back seat

Riyadh’s arms bazaar

The Financial Times in September reported another major Saudi deal, with Riyadh planning to buy at least $2 billion worth of Russian arms. According to the British daily, the contract could be signed before year’s end, yet Wezeman warned that Russian arms manufacturers tend to announce things early, and recommended adopting a “wait and see” attitude.

It is nevertheless an interesting development. KSA has significantly improved its ties with Russia in recent years. Following former Russian President Vladimir Putin’s 2007 visit to the kingdom, the first ever by a Russian head of state, Moscow and Riyadh last year signed a military cooperation agreement. The Financial Times reported the value of the deal was at least $2 billion, and possibly as high as $7 billion, including hundreds of Mi-35 attack helicopters, Mi-17 transport helicopters, T-90S tanks, BMP-3 infantry vehicles, and, most importantly, the S-400 Triumf, Russia’s most advanced anti-aircraft missile defense system.

The S-400 is an upgraded version of the S-300 long-range surface-to-air missile system, and is capable of detecting and engaging six targets from a range of 400 kilometers. Despite the arrival of the Russians in a region that is traditionally a customer of Western arms manufacturers, not a word of protest has been heard in Washington or European capitals.

Serenading Moscow

Most analysts believe that the deal is some sort of sweetener, aimed at convincing Russia to accept economic sanctions on Iran and dissuading Moscow from selling its missile defense systems to the Islamic Republic. In a widely publicized 2007 deal, Russia agreed to sell Iran its S-300 missile defense system — a contract reportedly worth between $750 million and $1 billion — yet so far no delivery has been made.

“The pressure from the US is a stick, and the huge weapons deal prepared by the Saudis is a carrot,” Ruslan Pukhov, director of the Centre for Analysis of Strategies and Technologies, told the Russian news agency Interfax. “We all know Saudi Arabia buys weapons as a ‘bribe’ to the world’s great powers in exchange for support.”

“The exact motivations and rationale for arms procurement by most governments in the Middle East often remain obscure,” said SIPRI’s Wezeman. “Only in Israel there exists some sort of public debate. It is plausible that KSA wants to buy arms from Russia, in particular air defense missiles, on the condition that Russia does not sell the same weapons to Iran. That would be a very good bargain indeed, as it would not only increase its defense capacity, but also keep Iran vulnerable. Considering the major military market in KSA, this scenario may also be appealing to the Russians.”

“But other motivations may play a role as well,” he continued. “KSA may want to diversify its sources to avoid ending up in a situation where its current suppliers will restrain their exports. KSA may want to improve its relations with a broader group of global players. Last year, for example, it bought Chinese artillery, which may have been aimed at pleasing Beijing. Finally, there may be a relation with the division between power centers in KSA, where the National Guard has often bought weapons completely independently from the armed forces.”

A qualitative edge would make up for a quantitative manpower shortage when facing a bigger adversary

Emirates bristle with US missiles

KSA is not the only country splashing out on arms. The UAE has invested considerably in missile defense systems, fighter jets and marine vessels. Unfortunately, there are few reliable figures available regarding the UAE’s overall military budget, if only because military spending by individual emirates is not included. Consequently, SIPRI has not published UAE figures since 2005. Still, from the reported arms deals it becomes clear that the UAE has optimized its defense capabilities.

According to the Dubai-based Institute for Near East & Gulf Military Analysis (INEGMA), the noticeable hike in defense expenditure in a few Gulf countries, and specifically in the UAE, is very much related to a possible regional war between Iran, on the one side, and the United States and Israel on the other, which might swirl out of control and drag in the Arab countries.

According to INEGMA, it is of strategic importance for the UAE to keep the Strait of Hormuz open for import and export.

“Lacking geographical depth and sizable manpower, the need to protect strategic assets requires the country to seek high-tech and top quality defense systems to make up for the existing disadvantages, and to extend an effective defense umbrella to all of the state’s assets and its infrastructure,” said Riad Kahwaji, INEGMA’s founder and general manager.

“So it is a qualitative edge that would make up for quantitative shortages in manpower, especially when facing a bigger adversary.”

Fortress Arabia

According to Kahwaji, the UAE and other Gulf states could also become the target of terrorist attacks by extremists entering the country illegally by land or sea. That’s why in 2008 the UAE embarked on a multi-million-dollar high-tech project to consolidate the security of its borders with cameras and sensors, as well as reconnaissance airplanes and coastal patrol boats. The country also recently asked the Pentagon for approval to purchase more than 360 Hellfire missiles and all accompanying hardware.

Earlier this year, the UAE became the first foreign country to purchase the Theater High Altitude Air Defense (THAAD) system with advanced Patriot PAC-3 missiles for low-to-medium altitude interceptions and advanced radars, both airborne and land-based, for early warning.

The country furthermore completed taking delivery of 80 US F-16 fighter jets, which are to operate alongside its 60 French Mirages, and it has ordered a series of Hercules and Boeing transport planes from Lockheed Martin, reportedly worth some $3 billion.

Finally, the UAE Navy ordered a $117 million anti-sub frigate from Italy and asked the Abu Dhabi Ship Building Company to build 12 new Fast Fighting Vessels and upgrade 12 existing ones.

How real is the Iranian threat?

To justify the billions of dollars spent on the military in general and arms procurements in particular, the region’s politicians and media almost routinely point at Iran, which allegedly aims to build an A-bomb and is said to have regional ambitions in Iraq, Afghanistan and beyond. Or, as Egyptian President Hosni Mubarak cried in 2008: “The Persians are trying to devour the Arab states.”

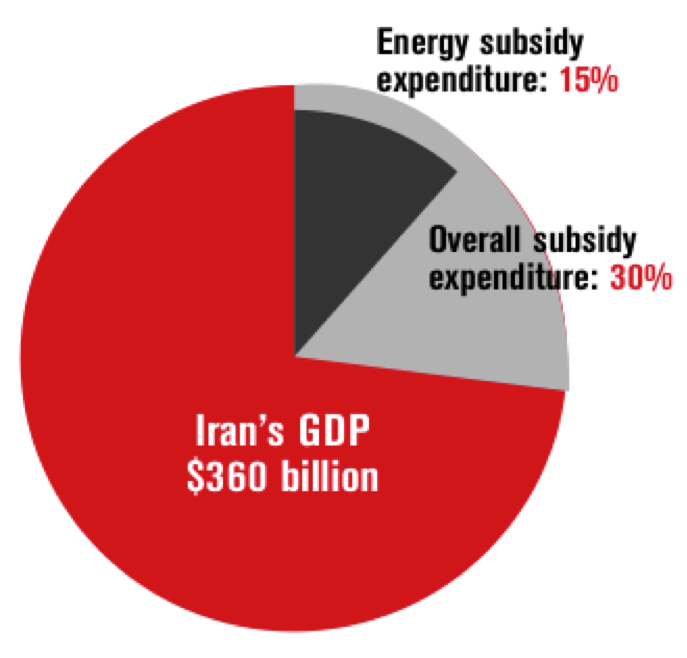

Thus Iran has effectively taken over Israel’s role as the region’s main bully and bad boy. The fact is that Iran has increased its military spending, from $3.2 billion in 1999 to a touch more than $6 billion in 2008 and, as stated previously, this amount is arguably much higher as it does not include the country’s budget for the elite Revolutionary Guards.

Inflated threat

Even so, most experts agree that Iran’s military threat is greatly exaggerated. The London-based International Institute for Strategic Studies (IISS), for example, estimates that Iran, with a population of 66.5 million, spends up to 25 times less per capita on its military than Israel and most of its Arab neighbors.

According to Travis Sharp, military policy analyst at the Center for Arms Control and Non-Proliferation, the Arab states are wary of Iran’s military threat, yet that hasn’t stopped them from maintaining close political and economic relations with Tehran. Billions of dollars in goods destined for Iran pass through Dubai annually.

“Is the UAE willing to participate in strengthened sanctions against Iran if doing so would mean the loss of trade revenue?” Sharp posited. “Probably not, especially if the UAE and other Arab states believe that Europe, Israel and the US are going to deal with Iran…the Arab states want a free ride on the West’s commitment to prevent an Iranian nuclear bomb.”

“Iranian arms procurement has been discussed widely in recent years, but a lot was based on rumors…which have not proven to be true,” said SIPRI’s Pieter Wezeman. “Two years ago Iran was first said to buy 250 advanced combat aircraft from Russia, yet nothing happened. Russia has sold Iran some short-range missile air defense systems, but (apparently) has put delivery of long range air defense missiles on hold.”

“Whatever the intentions of the Iranian government are, its military capabilities are limited and easily exaggerated,” Wezeman continued. “In terms of conventional weapons Iran’s capability to threaten anyone is very limited. Iran has not been able to buy large numbers of advanced weapons, such as combat aircraft and long-range missile air defense systems, while most, if not all, of its adversaries have comparatively large, or very large, arsenals of such weapons. Iran also does not have the financial means to go on a major arms procurement spree.”

As a result, the Iranian armed forces are largely equipped with outdated weapons. Just look at Iran’s air force, which will have to win the battle for the skies with a few dozen 1991 French Mirages, Russian Migs and Chinese jets, as well as a handful of American 1968 F-4 Phantoms.

Ironically, despite the boycott, much of Iran’s arms are American-made and stem from the days when the Shah was a major American ally. Meanwhile, the US is replacing its fleet of F-16s with the more advanced F-35s and F-22s, and has sold hundreds of F-15s and F-16s to countries such as Turkey, Egypt, UAE and KSA. Israel has the largest fleet of F-16s outside the US, and is to receive F-35s to maintain “its qualitative edge” over its Arab neighbors.

Iran’s capability to use force lies mainly in its arsenal of ballistic missiles and its influence over (militant) groups in countries such as Iraq and Lebanon. However, Iran’s missiles are limited in number and lack accuracy. Armed with conventional warheads, they have a limited military impact. Of course, if Iran would acquire nuclear warheads, the story would be quite different.

Yet, as Wezeman pointed out, it remains to be seen in such a scenario how current Arab arms procurements will actually help to face any real or perceived Iranian threat.

“It can even be argued that Iran perceives itself as being encircled by unfriendly states with considerable, partly offensive and increasing military capability, which may be an added motivation for Iran to pursue some sort of nuclear weapons capability,” Wezeman concluded.

Israel’s might made in America

Israel remains the region’s top spender after KSA, with a military budget of $13 billion in 2008, which represents some 8 percent of GDP, and an increase of 31.5 percent since 1999. Despite Washington’s arms sales to Arab countries, Israel remains without a doubt its leading ally in the region.

In 2007, the Bush administration increased military aid to Israel by more than 25 percent to an average $3 billion per year for the next decade.

“We consider this $30 billion in assistance to Israel to be an investment in peace — in long-term peace,” Nicholas Burns, then Under Secretary of State for Political Affairs explained. “Peace will not be made without strength. Peace will not be made without Israel being strong in the future.”

The Bush administration also announced the sale of additional sophisticated weaponry to Saudi Arabia and other Gulf countries, yet US officials have since repeatedly stressed that US policy in the region is based on maintaining Israel’s “qualitative military edge” over its neighbors.

Nearly half of the US annual military aid budget goes to Israel, which is the only recipient not obliged to spend all of it in the US. This has not only helped the Israeli armed forces become one of the most advanced and feared in the world, but also helped the country build a domestic defense industry, which today ranks among the leading exporters worldwide. On average, Israel uses some 75 percent of American military aid to purchase US defense equipment.

While Israel already has the largest fleet of F-16s outside the US, in addition to F-15s, as well as all the latest attack helicopters, Washington has agreed to sell 25 more advanced F-35s to Israel, with an option of another 50. The F-35 will not be sold to Arab countries. Last but not least, Israel has an estimated 150 to 200 nuclear warheads, which can be delivered by a ballistic missile.

The 10 largest arms producing companies, 2007

*Note: Companies are US-based, unless indicated otherwise. The profit (not the sales) figures are from all company activities, which include non-military sales.