The timing was hardly ideal.

Four years ago, the Samba

ice cream factory in the

Syrian city of Homs began operations,

rolling chocolate-covered ice

cream bars off its modern assembly

line. Samba’s aim was to be one of the first makers of premium ice cream in the country.

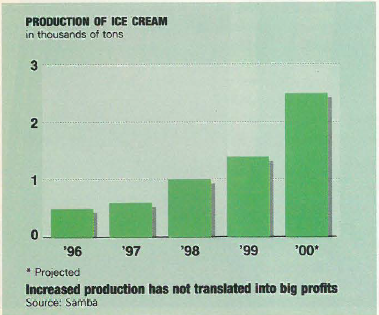

Production jumped from 600 tons in 1997 to 1,400 tons by 1999 with forecasts

at 2,500 for this year. The newly expanded factory is now working

around the clock. The firm’s national distribution network includes

35 refrigerator trucks and vans covering

7,500 points of sale with logistics and distribution

offices in Damascus, Aleppo, Al-

Jazira and Homs. Samba refused IP disclose its revenue. Using the official exchange

rate, sales for 1999 can be roughly calculated

at $4.5 million based on output and an

average price of SL10.

If the story sounds rosy, it’s not.

Expansion has not translated into big profits.

At about the same time that Samba went into

operation, no less than three other new companies

opened top-of-the-line ice cream factories

of their own: Muller, Carina and

Iceman. Carina, which enjoys a formidable

name in Syria. is a joint venture between Saeb

al Nahas and Hasan and Mohamed

Alameddine, the latter being owners of

Lebanon’s Cortina. Iceman, which entered

the market in 1995, produces about 3,000 tons of ice cream annually.

For Samba, the new arrivals meant that as production increased,

competition got stiffer. And with the onslaught of a nationwide recession,

reducing people’s purchasing power, the company had no choice

but to drop its prices. Profit margins shrank from around 15% to less

than 10% for ice cream companies, says Yihiya Talgabini, part-owner

of Muller. Iceman tried to counter that trend by increasing output,

while Samba shifted its production toward the lower end of the market.

When Samba started out, 60% to 70% of sales were in medium range

products (costing between SLI0 and SL15), whereas today

70% of sales are in low-range items (costing around SL5), says Imad

Rifaii, Samba’s vice general manager. “We had to reduce our prices

outside the city, where the purchasing power is lower,” he says, adding

that increased availability of other products created more competition.

“Of course, profits went down with falling prices.”

But there was even more competition for Samba at the low end of

the market. Ice cream has traditionally been produced for mass consumption

in Syria rather than for a premium

clientele. Hundreds of mom-and-pop

type operations manufacture mostly

Arabic ice cream manually. Few have bothered to upgrade their production line

but together they control 30% to 40% of

the market. Al Mees is one of the more

innovative of the traditional Syrian ice

cream companies. The firm started operations

in I %2, producing ice cream manually

until 1980, when it introduced new

machinery. Al Mees claims to have 5,000

points of sale and is planning to expand its

factory. ‘There are only about 10 factories

using machines and about 500 old factories

still making ice cream manually, 200 in Aleppo alone,” says Mohamed

Zoukeir, part-owner of Al Mees.

Focusing on the low end of the market

meant that Samba was forced to reduce the quality of raw materials

it imports such as milk, milk powder and sugar. “We use the same

suppliers but lower than premium quality without it much affecting

the taste for the consumer,” says Rifaii. The firm has also beefed up

its marketing effort. Samba spends about 10% of its sales each year

on advertising-60% on TV ads though the company also uses billboards.

Today, Samba offers more than 40 different ice cream products

in a wide range of flavors.

But probably one of the biggest challenges Samba faces is the limited

Syrian market. Ice cream consumption in Syria is among the

lowest in the region. The average Syrian licks up a mere one kilogram

of ice cream per year, partly because of the absence of large

supermarket chains. The Lebanese, by contrast, gorge themselves,

with a annual per capita consumption of about nine kilograms, which

is still just half the level in Europe and a third of that in the US.

Syria’s Muller recently tried to enter the Lebanese market. But the

venture proved unsuccessful after it became entangled in a legal battle

with a local company. Al Mees is also contemplating moving into

Lebanon. “Muller entered and is now out, but we will follow

Muller’s move next year at this time, and we will compete on both

quality and price,” says Zoukeir. As for Samba, Rifaii says that he has

no plans to move into Lebanon, because that would only increase his

overhead and distribution costs with little effect on profits.

Eitl1er way, the situation in Syria is likely to get worse before it gets

better. New president Bashar Al-Assad is seriously talking about

economic reform, which might mean opening the country to more

imports, including foreign ice cream brands. Perhaps the time has come

for Syrian ice cream companies to team up. “Merging is a sound policy.

We can buy out small factories, improve their production and take

advantage of their market, but we haven’t studied that option yet,” says

Rifaii. He better get busy; times are changing in Syria.