Lebanon, start your engine. “The

rally of Lebanon is targeted to

become a world championship

course in 2001,” asserts Gaby Kreiker,

director of the Automobile and Touring

Club of Lebanon (ATCL). He expects 500

foreign journalists to swarm the country to

report on the 900-km, four-day race, an

event that is expected to attract big-name

sponsors and professional drivers from

around the world.

Even more ambitious

are the plans to hold a Formula One race in

the Beirut Central District in the next few

years. Over a billion people could watch

Michael Schumacher weave his Ferrari

through the streets of Solidere on TV. The

event could attract as many as 40,000 visitors

and pump hundreds of millions of

dollars into the local economy.

Sounds like the dreams of a motor-crazed

country craving international attention. The

Lebanese have a passion for car racing, as

anyone driving to Jounieh on a Friday night

quickly discovers. But the sad reality is that

motor racing events here are crashing.

“Motor sports are one of the most expensive

sports you can do,” says Kamil Maalouly,

one of three partners who own the Motor

Club, a company involved in organizing

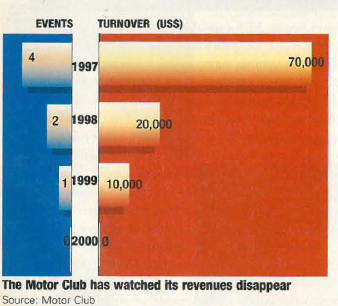

amateur rallies. In 1997, its best year,

Motor Club organized five events, including

the Amateur Cup, which attracted 350 competitors.

The event was covered by LBC,

which contributed 200–300 advertising

spots. Motor oil company IGOL was the

main sponsor, contributing $10,000, with a

number of smaller co-sponsors throwing in

another $15,000.

But in 1998, the Motor

Club organized just two events. The company

had to shift to MTV for coverage of the

Amateur Cup because LBC was no longer

willing to contribute the same number of TV

spots, and the number of participants

dropped by more than a third.

Last year, the

Amateur Cup was the only event organized

by the Motor Club. This time, the company

had to go to Future TV for sponsorship and

only 60 competitors participated. The

Motor Club did well during those three

years, earning profits of around $50,000 on

revenues of $100,000. But for 2000, lack of

demand has meant that the company is not

organizing any events.

Kreiker understands these problems well.

ATCL, a non-profit organization with 9,000

members, organizes such big-name races as

Rally of Lebanon and Rally of the Cedars, as

well as a number of smaller karting, 4×4, and

closed-circuit events.

“Between 1992 and

1994, there were no other spectator sports, and

we made money. But since 1995 we started

to go downhill, losing coverage to basketball

and other events,” he says. Rally of Lebanon

and Rally of the Cedars used to get an average

of 20 TV spots per day, one month

before the event. Today, they get just 10

spots. “This affects our sponsors and drivers,”

says Kreiker.

ATCL has to pay around $200,000

of the $600,000 budget to organize

the Rally du Liban. Marlboro foots about

$250,000 of the bill, with TV stations — such

as LBC and MTV — contributing $100,000.

Co-sponsors pay the rest.

For the Rally of the Cedars,

these days ATCL must

pay the entire $70,000 to

$100,000 needed to organize

the event. The organization

receives no contributions from

TV stations.

ATCL’s difficult situation

could change if the Rally of

Lebanon is promoted from

the Middle Eastern rally car

circuit to the world circuit, as

Kreiker says will happen.

While the Middle Eastern

circuit stops in Dubai, Abu

Dhabi, Jordan, Qatar,

Bahrain, Cyprus, and

Lebanon, the international

circuit is held at 14 different

locations around the world.

With sponsors like Michelin

helping to finance the event,

an international rally car race

could bring an estimated $10

million of revenue into

Lebanon.

Profits generated

from the event could then be

reinvested in order to make

the Cedars Rally into a

Middle Eastern circuit event.

The payoffs of a Formula

One race would be even

greater. The idea first arose

in the mind of Khaled Altaki,

a local businessman, in 1994.

His Beirut Hariri Circuit

would have run along the

Ramlet El Baida promenade.

The idea has since been

scrapped, although Altaki

now claims to be designing a

second closed-circuit track

running in an as-yet-undisclosed

location.

But the main impetus these

days is on the idea of running

a Grand Prix through the

streets of Solidere. The Ministry

of Tourism has appointed a committee of five officials,

including Cheikh Fouad Al Khazen, the

chairman of ATCL, and Nabil Karam, a

five-time champion with ATCL, to prepare

a budget and market the event through a private

company.

Should Lebanon be awarded

the rights to organize a Formula One race,

ATCL would be given the job of managing

the race. The event would demand a year of

preparation and require an estimated budget

of $100 million. ATCL would be charged

with managing the event, gaining valuable

experience and worldwide recognition.

“Formula One will change the face of

Lebanon in the eyes of the world,” says

Karam. Hotels would be full for a week,

generating some $3 million for the government

in restaurant taxes alone. It has

been estimated that the event would generate

$100 million in profits for organizers,

which would be shared by the government,

ATCL, and the company in charge of marketing

the race.

“It will have a snowballing effect on

tourism and everyone will be positively

affected — taxis, hotels, restaurants, malls,

retailers — and it will put Lebanon on the

tourist map for the entire world,” says Fadi

Saab, board member of the national council

for tourism. Saab, also chairman of TMA,

would be involved in facilitating the transport

of racecars into and out of the country.

Sound too good to be true? It probably is.

Lebanon is competing against Egypt and

Dubai to host the event. Although Lebanon

has the best climate, Sundays off, and a casino

for gambling, Dubai has pledged to spend

close to $1 billion to organize the event and

is the leading candidate.

At the same time,

Dubai and Egypt do not have to deal with the

nasty political environment plaguing

Lebanon. “Bernie Ecclestone, the head of the

international association for Formula One organizers,

refuses to come to Lebanon under

these conditions,” says Karam, adding that

Formula One wouldn’t take place here

before regional peace is achieved.

Others feel that Lebanon is not ready to host

an event of this size. “It seems to me that it’s

too early to organize such an event. The

country doesn’t have the necessary organization

to attract the right amount of tourists and

make sure their stay is trouble-free,” says

Ghassan Matar, previously an independent

consultant for the ministry of tourism.

If Lebanon succeeds as a candidate, organizers

will have to wait until 2003 before

they can hold the event. Until then, perhaps

the slogan we should be promoting is

“Rally for peace.”