In 1996, Ghazi Kraytem, general manager

and part-owner of Soliver, found

himself in a tight spot. A manufacturer

of glass bottles, Soliver was facing all the

difficulties afflicting local industry: high real

costs, high domestic and regional tariff

barriers, corruption and a slipping economy.

But for Soliver things were more acute.

Competition in the Gulf, its main export

market, had been growing “astronomically,” says Kraytem. In two years, industrial

capacity for glass bottles there grew 600%

while demand was barely growing. “We

got hit pretty bad,” he says. “Our competition

was selling to our customers at 25% less than

our cost.” Making matters worse was the

impact plastic containers were having on

the glass bottle market. Bottles made from

PET (polyethylene terephthalate) have

become favorites of soda and bottled water

producers, because the material offers glass-

like clarity but won’t break like glass and its

lightness makes transportation cheaper.

These factors made Soliver’s future

prospects unappealing. “We had a choice of

either closing down,” says Kraytem, “or

meeting the challenge.” In order to become

competitive, both locally and internationally,

Soliver had to cut costs, replace its outdated,

labor-intensive manufacturing equipment and invest $14 million in new

high-tech machinery.

But just hold on a minute there. What was

that first bit? Cut costs? Isn’t cutting costs

just a euphemism for laying off workers, for

firing people? In Lebanon eliminating old

machinery and investing in new equipment

is fine, but firing people, that’s a different

story. And for Soliver, it was. While the

company faced no interference with its resolution to upgrade its operations, the firm’s

“reluctant” decision to lay off 70 workers

attracted a lot of government attention.

“When we informed the ministry of

labor,” says Kraytem, “they said we could

lay off workers, but not as we wanted to.”

Instead, after talks with the prime minister

and pressure from the ministry, Kraytem

says that Soliver was required to pay $1 million

in compensation for its 70 workers, on

top of their end-of-work indemnities. In

return Soliver was given promises, such

as protection from imports, lower utility and

fuel costs. “We even had a written contract

with the ministry of labor, but nothing

came of it,” he says. And what infuriated

Kraytem even more was that many of the

laborers Soliver hired were not needed in the

first place – they were employed as a result

of political pressure.

Soliver’s case is not unusual; it’s just one of

a few companies willing to go on record

about the issue. Indeed, Kraytem says he

knows of many other companies that were

forced to hire unnecessary workers and pressured

to keep them when times got tough.

The case neatly illustrates what most

industrialists or managers of any other

labor-intensive operations know: keeping staff on,

even if they are redundant, is considered

an unwritten law in Lebanon. And

implicit in this law is the understanding

that if you fire staff, it will cost you.

We say unwritten because the labor law

itself does not encompass such a meaning.

Katia Bou Assy, an attorney at Moghaizel

Law Offices, argues that the Lebanese

labor law is quite clear. “The employer or

the employee can terminate the agreement

at any time provided the conditions are

complied with,” she says. Those conditions?

Firstly, an employee should not

be dismissed unfairly. For example, notice

must be given. An employee with less than

three years’ service at a company must be

given one month’s notice, between three to

six years requires two months, between six

and 12 years three months, and finally

more than 12 years’ service requires a less

than onerous four months. Alternatively, if

the employer is particularly keen for the

employee to go, it can choose to pay in lieu

of giving notice.

Other cases of unfair dismissal include firing

someone because of membership in a

workers’ union or because the employee has

filed legal action against the employer in

order to oblige the employer to conform to

applicable laws. Finally, the employer

can’t fire a worker who is a board member

of a union; in this case the employer must

apply to the labor court, which will in turn

make the decision.

So what about a legal dismissal? By law,

if the employee is incompetent, he or she

can be fired without notice as long as the

employee is given a minimum of three

warnings or if the employee’s negligence

causes damage to the employer. In the latter

case, the employer should inform the

ministry of labor within three days of

becoming aware of the negligence before

firing the employee. If the employee is

absent from work without a legal excuse for

more than 15 days in one year, or seven days

consecutively, the employer can also fire

without notice.

But perhaps the most important clause in

the labor law has to do with terminating

employment based on a company’s financial

difficulties. The law states that a firm can lay

off employees if it is facing financial trouble,

in other words, if keeping workers

would impair or jeopardize the company’s

survival, or if it needs to upgrade technology,

operating or manufacturing systems,

a process that may involve laying off

employees. This is critical: If a company is

not free to cut costs and upgrade during a

recession and as a consequence it folds,

many more would be hurt than the few targeted

to lose their jobs.

In order to lay off employees under this

clause, the employer has to inform the

ministry of labor of those he intends to let

go and the ministry will act as a third party

between the employer and the employee to

negotiate the level of compensation.

Again, according to the law, the level of

compensation is clear. The employer is

required to pay anywhere from two to 12

months of salary in compensation; the court

determines the amount of compensation by

taking into account things like the employee’s

age, years of service and health.

But this is in theory. Nicholas Nahas is a

shareholder and director of Sibline, one of

Lebanon’s largest cement manufacturers and an employer of about 400 people. He

argues the reality is quite different and that

companies often pay much more compensation

than is stipulated under the law,

thanks to interference from the ministry of

labor. The reason, says Nahas, was the

high-inflation period during and after the

war. When inflation was sky-rocketing, at

times the lira dropped 30% a day against the

dollar, the ministry of labor was made

responsible for determining the dollar-

pound exchange rate; in effect, the amount

of compensation to be paid. The problem

with this, says Nahas, is that it opened the

window for the ministry to apply a greater

degree of influence on the private sector in

terms of employee compensation.

Additionally, Nahas argues that once the

economy had stabilized, the established

system continued.

The reason the ministry of labor has continued

to exercise influence over employer-employee

relations is not so much to do with

the simplistic and outdated belief that private

companies are merciless and out to rip

off workers given the chance, but more to

do with the deficiencies of the Lebanese

state. Since the government has not seen fit

to establish a welfare system that provides

unemployment benefits and job search services,

the ministry of labor has been forced

to act as a quasi-department of social security

at the expense of the private sector.

Fares Saad, the head of work force relations

at the ministry of labor, is unabashedly

direct about the ministry’s unofficial

role. “We cannot force any company not to

dismiss an employee; the Lebanese labor

law is clear on this point. But the first thing

we do when an employer wants to lay off

staff is to try to ensure [via negotiations with

the employer] the continuity of work, to

keep them at work,” says Saad. “For example,

if the owner wants 12 employees to go, we try to lower that to eight or less and ask

the employer to transfer the others to different

positions.” Negotiations don’t end

there, however. “If that doesn’t work,”

says Saad, “when we discuss the level of compensation with the business owners,

we try to ensure that the employee is given

more compensation than 12 months’

salary. Why? Because we can’t always

find vacancies at another company for

these employees.”

This is the reality of employer-worker

relations here. “In Lebanon,” says Saad,

“we have no retirement or end-of-service law

while at the same time we have no law for the

people who can’t find a new job. For this reason,

we make the employer pay penalties.”

That statement neatly reveals the conceptual

chasm between government officials

and Lebanon’s private firms. In the

absence of a functioning welfare system, the

ministry of labor wants the private sector to

pay; on the other hand, private companies

and institutions, like their international

counterparts, argue that social security is not

their responsibility.

“We prefer, as the ministry of labor,”

says Saad, “for Lebanese laborers to be

employed for $400 a month than for a foreigner

to be given the job for $150. But the

companies always prefer their profits.”

Indeed. Any manager of a private company

will argue that its number one priority is

delivering growth and profits and that it’s up to

the government to provide the legislative

framework and resources to protect worker

rights and ensure adequate welfare.

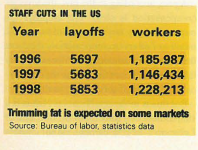

The logical extension of this thinking is

the type of labor relations exercised in the

United States, where companies routinely

hire and fire without government interference

and where private sector icons like

IBM, Boeing and Levi Strauss can lay off

tens of thousands of employees under

restructuring programs, a move that is

generally welcomed by investors.

This kind of labor flexibility is possible in

the context of the world’s strongest economy

and a well-developed social security system

originally put in place through lessons

learned during the Great Depression of the

1930s. It’s impossible to argue that this

could happen any time soon in Lebanon.

The bottom line is that with no welfare

system in place and the ministry of labor the

self-appointed guardian of the Lebanese

worker, laying off staff will remain an

expensive and politically difficult exercise

for local firms, which ultimately raises

their costs and undermines efficiency. If private

companies absolutely have to fire

employees on a large scale, they will face

pressure from officialdom. “I’ve lived

through several ministers of labor,” says

Nahas, “and they always have some connections.

It’s politics. So if you need to lay

off 30% of your work force, you never

know what’s going to happen. And I have

stories where it was really painful.”

The result is that a lot of firms try to lay

off carefully and quietly, or just not at all.

The over-staffed banking sector has a few

examples. Bank of Beirut managed to quietly

reduce its staff from 490 to 417 after its

merger with Transorient Bank at the end of

1998, and aims to reach 400 by the end of

2000. Banque Audi, on the other hand, doesn’t

lay off workers. Although it has a reputation

for a high overhead, it has refrained from

hiring new employees to staff its rapid

branch expansion and has instead been

attempting to transfer existing employees to

the new branch positions.

Until the government is in a financial position

to provide some sort of welfare scheme to

the unemployed, local businesses are unlikely

to see a more flexible labor market. So local

business owners or managers will have to grin

and bear the situation or think of new ways to

increase worker productivity, because the

law certainly won’t help them.