Fear, adoration and envy are emotions with great relevance to human and business relations. If we don’t look at a leader in fear or adoration, we often look at her or him in envy – but usually we keep one eye on the leader. Sometimes the only reason why we don’t look to the leader is because we are too busy trying to become the boss and often it is our biggest loss if we don’t learn from, copy or emulate a relevant leader.

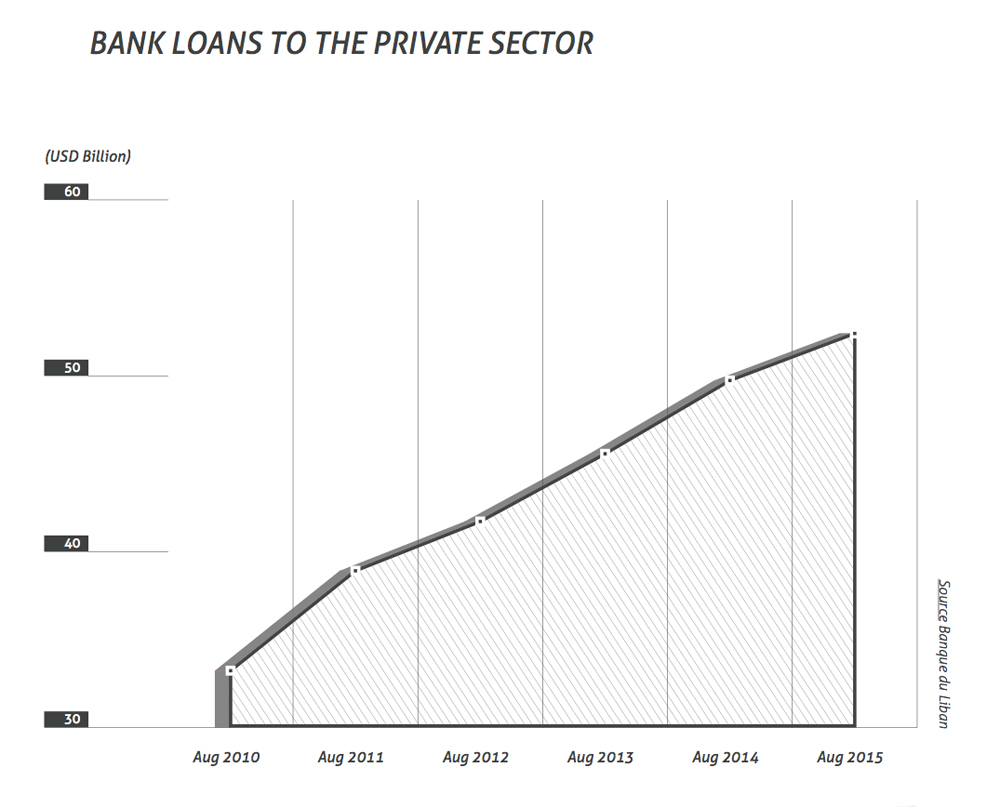

Banks are arguably the businesses that are best positioned for being viewed as leaders in the Lebanese economic context, given their much-larger-than-GDP shares in financial assets and their lifeline function in financing the private and public sectors. In order to gain leader-level perspectives on quantitative and qualitative factors that mattered most in Lebanese banking in 2015, Executive talked to influencers at four banks that between their institutions represent some 53 percent of assets in the Lebanese banking sector, employ nearly 16,000 people in Lebanon and abroad and have networks entailing 300 domestic and 270 foreign branches, demonstrating their strong diversifications and mix of local and global approaches.

[pullquote] Our consolidated balance sheet shows growth of $398 million in assets [/pullquote]

Sector leader Bank Audi ranked first in consolidated net profits but while it increased its assets by 6.2 percent year on year to $42.3 billion, its year-to-date growth in assets, at 0.95 percent, was deceptively low when viewed only in consolidated dollar terms. The background of this dichotomous looking picture resides in the bank’s operations in foreign markets and exchange rate developments between the US dollar and currencies of markets where Audi Group has significant presence, which include the eurozone, Turkey and Egypt, according to Freddie Baz, group strategy director and board member of Bank Audi. He tells Executive: “Our consolidated balance sheet shows growth of $398 million in assets for the first nine months in 2015. Growth of assets is reported for the year to date, according to the International Financial Reporting Standards. If I consider the constant exchange rate at the beginning of the period, which is end of December [2014] for the year to date, my assets would have grown by $2.4 billion to September. You have to produce consolidated statements but it is a very conceptual exercise that is done just to give a view how things look if it was one single currency and single entity and single geography. If we apply constant exchange rates, we would have seen a balance sheet not of $42.3 billion but $44.7 billion at end of September.”

Turkish delights

Currency volatility in economies where Audi Group operates was most pronounced in Turkey during the first nine months of 2015, with the Turkish lira weakening by some 30 percent against the dollar, giving up much more of its value when compared with the dollar exchange rate developments of the euro and Egyptian pound in the same period. Given that Turkey is the most important market after Lebanon for Bank Audi, the reflection of the country’s exchange rate drop in Audi’s consolidated balance sheet would be irksome for presenting results to superficial observers. However, Baz maintains that serious analysts look at results of individual entities and claims that the stability outlook for Turkey has improved due to clear pro-Erdogan election results in early November, and also due to the fact that the lira’s weakening in 2015 was driven by international investors’ anticipations of things that did not come to pass, mainly the increases in benchmark rates in the United States. “Turkey has been affected so far in anticipation of those potential changes in the benchmark rates. If those changes occur [in the near future], Turkey already paid the price in anticipation. [The drop in the lira] was obviously amplified by domestic political tensions but in terms of relative weight, I still believe that two thirds of the currency slip in Turkey was due to international money market considerations, with massive exits among portfolio investors generating this volatility in foreign exchange and in interest rates because the tool [that was available] to the central bank to face the situation was to raise interest rates,” Baz says, with a hidden nod to the positive implications that new growth in the Turkish market has for the performance of Audi Group going forward.

At BLOM Bank Group, international considerations are no less central but with a focus on foreign subsidiaries that were less or not exposed to the currency turmoils of 2015. Profits for the first nine months in 2015 amounted to $290 million on total assets of $30.7 billion. “We have seen 7 percent increase in profits so far this year and expect to see what happened in the first nine months to continue through the rest of the year. All the growth in our profit was coming from outside, I would say. We had a big improvement especially in the results of our Egyptian subsidiary and also saw good improvements in our Jordanian [unit] and from our presence in the Gulf,” BLOM Group Chairman Saad Azhari tells Executive.

Maintaining the paradigm that conservatism is no contradiction to innovation, Azhari attributes the development of BLOM’s size and performance to a portfolio of conventional sounding initiatives. “BLOM has always been conservative and innovative at the same time. Our expansion in terms of presence in Lebanon is continuing as we are opening new branches in the north and also in the south and in Beirut. We have new products in retail and asset management, [such as] funds, and always try to provide the best service to our customers. We always continue to evolve because without evolving you cannot be a leader in the banking market,” he muses.

Bank of Beirut, the sector’s number three in terms of total profits achieved during the first nine months of 2015, Chairman Salim Sfeir says that his bank reached several milestones and was able to present good growth in the main financial indicators for the first three quarters. Numbers pointed to year-on-year growth above 10 percent in both assets and deposits by the end of September; loan growth was subdued, at 1.6 percent, and the loans to deposits ratio saw a downward variation of 3.17 percentage points, the largest drop by any bank in the alpha group, the tier of Lebanese banks with deposits above $2 billion. Bank of Beirut reported 12 percent growth in net profits when compared with September 2014, ahead of the 9.7 percent increase identified by analyst firm Bankdata as the average for the alpha group. The bank was in a median position for profit growth rates of alpha banks as six lenders showed higher rates of increase, beginning with CreditBank that nearly doubled its net profit year on year.

Highlighting the bank’s activities in asset management – where Bank of Beirut had the alpha group’s second best year-to-date growth in assets under management in the first nine months of 2015 – and trade finance as two areas of special strength, Sfeir explains the importance and scope of trade finance in the context of Bank of Beirut as an activity where the “Lebanese scenario is not really Lebanese” but a regional one. “Trade finance is an international much more than a regional market and we, as Bank of Beirut, are very active in trade finance not only in Lebanon but in the region and in Africa,” Sfeir explains. However, he then goes on to say that trade finance activities have recently been impacted by the weakness of the oil price and related disadvantageous developments in important countries such as Nigeria where the election of the current president was followed by decisions to limit certain trade activities. “The overall situation [for trade finance], be it in the Middle East or in Africa, is regretfully not promising for the near future. So we continue to be very active and continue to look for new opportunities,” Sfeir says.

In addressing the bank’s strategy mix for working in Lebanon versus its expansion steps in other markets, Bank of Beirut’s chairman elaborates: “We are all dependent on Lebanon because Lebanon is our natural market and we have greater room for mobility within our own marketplace. We, meaning the Lebanese entrepreneurs, are not looking to be strong players on the international market because we are fully aware of our dimension. However, we are very active on the international scene insofar as our potential permits. Our role, whether as bankers or traders, is internationally driven by the marginal risk-adjusted returns over and above the returns from our own market. We are, and will remain, heavily invested in Lebanon. Yet within the next 24 months, around 50 percent of our income will be produced outside of Lebanon; mainly in stable A Grade countries.”

Survivor instinct

The long-standing second runner up by assets and deposits in the Lebanese banking sector, Byblos Bank, saw its assets increase to LBP 29.1 trillion, or $19.3 billion, at the end of September 2015 and reported nine-month profits of $113.2 million, almost unchanged from the same period in 2014. Growth in assets was below 2 percent in both year to date and year on year comparisons and the bank slipped one notch in asset rankings, behind relatively stronger gainer Fransabank. Byblos Bank remained in third place for total customer deposits and maintained powerful positions in the domestic market, including leading roles in deposits in Lebanese pounds and in domestic loans, as well as by openings of letters of credit and assets under management.

[pullquote] Without evolving you cannot be a leader in the banking market [/pullquote]

According to Alain Wanna, head of group financial markets and financial institutions and member in the core senior management team at Byblos Bank, 2015 was a year to prove the survivor qualities of Lebanon and Lebanese banks. “Even with all this uncertainty in Lebanon and the surrounding region and with the drop in oil prices, all of the Lebanese banks are making profits and they might report a slight increase in their profits. Deposits in Lebanon are expected to grow between 5 and 6 percent in 2015 and the assumption for the next year is that it will be the same rate of growth, so I think Lebanese banks know how to manage in difficult and tough times,” he tells Executive.

While Byblos Bank has pioneered expansions into regional and international markets ahead of many of its peers, 2015 continued to be challenging for many of these economies. “The most material subsidiaries that we have are in Syria, Iraq, Sudan [and] Europe, plus different presences on a smaller scale. So these markets are still witnessing tough times, all of them,” Wanna admits and affirms that the bank has no plans to abandon any of them. “When we enter a market, we enter for the long term. It was unfortunate there were unexpected events in several foreign markets that we have entered. But there is no decision at the board level to exit any of these markets. We are downsizing, limiting our exposure. But it is not on the agenda to exit fully from any market,” he says.

He furthermore emphasizes that Byblos is persistent in strategizing for new expansions which could easily boost the bank’s position in the banking sector’s pecking order. In an example cited by Wanna, Byblos Bank had its eyes set on the Egyptian market for a while and placed a bid for Piraeus Bank Egypt early in 2015. However, this did not result in a win; the subsidiary of the Greek Piraeus Bank was acquired by Kuwait’s Al Ahli Bank group. The Gulf lender, which reported assets of 3.82 billion Kuwaiti dinars ($12.55 billion) at end September 2015, paid $149.7 million, representing 1.5 times the book value, for the Egyptian unit, Piraeus Bank said in a November 2015 statement confirming the transaction’s closure.

Interesting narratives

A look across the banking sector’s developments in 2015 beyond the overall numbers and the performances of banks in the top size bracket shows numerous interesting narratives confirming which concerns are current and which have faded or are not yet getting attention. Quite a few of these stories relate to the banking sector’s inner workings and some specifically corroborate that the troubles of the Lebanese economy and state governance from the recent past have not impaired the sector’s appetite for growth and have not deterred aspirations of banks that believe they can mobilize enough competitive energy to push beyond the $2 billion deposits threshold that currently defines the alpha group.

In one such indication on the sector’s confidence and ruddy health, newcomer Cedrus Bank said in early spring 2015 that it wants to grow into the sector’s top size stratum. The new bank was formed in a collaborative effort between the local Cedrus Invest Bank and emerging markets specialist Standard Chartered which sold its Lebanese operation to Cedrus after trying for about 15 years to make its model succeed in the small market here. Standard Chartered officials did not want to disclose how they priced the sale to Cedrus or how much money they injected into their local adventure over their years of direct presence; both banks emphasized that they would collaborate in future.

Another bank that voiced its high ambitions in 2015 was Middle East Africa Bank (MEAB). Having just emerged from a succession transfer of ownership and corporate leadership, MEAB’s new chairman, Ali Hejeij, told Executive that it is his declared aim to reach alpha bank status. In response to an interview request for Executive’s year end issue, the bank confirms in a written statement that its goals for 2016 and beyond include “working towards becoming an Alpha bank in Lebanon”.

“We believe that the stability and notable resilience of the Lebanese market present an opportunity for MEAB to continue to grow in the coming years, both in Lebanon and in foreign markets,” MEAB General Manager Nabih Haddad adds, conceding, however, that it may be “too soon to develop a firm assessment of the bank’s performance” in the short time since the change in leadership in midyear. The transformation at the time had been related to a June 2015 action by the United States’ Office of Foreign Assets Control, which had placed Kassem Hejeij, the father of Ali and the bank’s chairman at the time, on a blacklist of alleged backers of Hezbollah.

Big Brotherism and other foreign ideas

Troubles with US politically-motivated interference in Arab banking have been impacting the operations of regional banks in varied ways since the 9/11 terror attacks against America. More important in 2015 than sanctions against individual businessmen and bankers have been the indirect effects of US policies where international banks tended to cut correspondent banking relationships with Arab banks. This problem had been highlighted by the Union of Arab Banks in several statements and contributions to the international conference in 2015. However, de-risking is a concern for all banks and could even lead to a new banking crisis, comments Bank Audi’s Baz. “By definition, a bank cannot survive if it’s not being provided correspondent banking services. All the global banks have been reducing their number of relationships, leaving medium to small banks without any correspondent relationships; [this] is no prospect for the future. We are talking about thousands of those banks globally,” he explains.

[pullquote] We are all dependent on Lebanon because Lebanon is our natural market [/pullquote]

According to Bank of Beirut’s Sfeir, foreign pressure continues to weigh down banks that are based in the Arab world and a different international leadership paradigm would be more productive. “We are being severely affected by the politically oriented actions of our big brother, the US government, which is being very unfair toward their followers in the region. Our American brothers have to be fair to our markets as much as they are fair to their own market if they are looking for [and maintaining a role of] international leadership. Leadership should be balanced,” he says.

An existential concern for banking (at least in theory) is the commitment and measurable contribution to society as function of their sound economic performance. More than the charitable engagements and social responsibility undertakings that can be presented in annual CSR reports – but are done so by too few Lebanese banks until now – the core issues in this regard are the governance performances, macroeconomic contributions and model functions vis-a-vis the state and society that banks must have an interest in carrying out, for the sake of their sustainability and long-term profitability.

With respect to governance, banking leaders are rather confident that they have not only come a long way in applying corporate governance standards but also are doing more than complying with the legal minimums that are being raised every now and then by the central bank via new circulars imposing stricter standards. BLOM’s Azhari says that both the Lebanese banking sector and the bank “are definitely improving in terms of governance, [such as] how you manage the bank and how you manage the relations with all stakeholders, in terms of employees, of shareholders and of customers.”

Baz says that for Audi it was a confirmation of extreme validity in the bank’s corporate governance approach when its corporate secretary and “godfather of corporate governance at Bank Audi”, Farid Lahoud, was invited in 2013 and 2014 to first become a member and then the chairperson of the World Health Organization’s audit committee.

Regarding the cost of corporate governance and increasing compliance regulations, he cites the issuance of a circular by Banque du Liban that required banks to employ a compliance officer in each branch. “We have 82 or 83 branches in Lebanon, [so] we have to have 83 compliance officers, one for each branch, in addition to which a lot of [information technology] systems are required. There is a cost, obviously, and all banks are incurring an additional cost for compliance,” he points out and argues that compliance needs to produce a good balance between certain compliance-induced reductions in the volume of business and improvements in business quality.

From the cost-benefit perspective, corporate governance is productive in relating to business clients which have stronger sensitivities regarding a bank’s policies that protect clients against information abuses and conflicts of interest but also in interacting with the average retail customer, claims Azhari. According to him the requirement for branch-based compliance officers meant that processes have become “perhaps more regularized” but BLOM could implement the change without direct extra cost to the bank. “But I can tell you that having good governance was always something [that] we felt gave us extra business,” he enthuses.

In the view of Bank of Beirut’s Sfeir, corporate governance in Lebanese banking is indeed on course to a “very positive evolution”. “We are improving yearly and are on the right track,” he says.

About going the macroeconomic mile

Whereas banks have a solid track record of highlighting their vital macroeconomic role of financing the private and public sector needs in Lebanon, 2015 saw some renewed accusations that banks were part of the country’s economic malaise by being in cahoots with political elites in a state of crony capitalism. All bankers in communication with Executive dismissed these accusations outright. Banking and politics don’t mix at Bank of Beirut, argues Sfeir, as each side’s interests conflict fundamentally with the other’s, and “a banker has no advantage to be a politician because he will lose his bank and a politician cannot afford to be a banker because he will lose his market.”

Byblos’ Wanna would not comment on the issue but Azhari says that allegations of mistrust between the Lebanese and their banks are generally unfounded. Pointing to studies on the reputation of different institutions and sectors in Lebanon, he concedes that banks are generally not liked in countries around the world. It may be a universal sentiment that banks are more trusted than liked, “but in Lebanon banks have a good image compared to other industries,” he assures.

[pullquote] The stability and notable resilience of the Lebanese market present an opportunity [/pullquote]

In Baz’s view the tendency to accuse banks of profiteering is in one way still related to times when interest rates on government debt instruments – such as treasury bills and certificates of deposit – were in double digits and ranged during some periods as high as 35 percent. However, this perception is flawed, he reasons, because banks operated with lower interest rate spreads than commonly thought. According to him spreads, which are presently around 2 percent, reached 4 or 4.25 percent “but not 10 or 15 percent” in those days. “I don’t have any respect for those populist messages [accusing banks of crony capitalism] which are not documented and unjustified. If one is professional and technical, one would say that the main suffering of this country entails no implicit or explicit or whatever alliance between banks and any third party, ever,” he exclaims and goes on to say that such accusations fail to address the real problems behind the Lebanese underperformance of many years.

The problem, he maintains, lies in what he calls the ‘Dutch disease’ of the country’s reliance on recurrent yearly inflows that boosted domestic incomes and triggered household consumption far beyond the domestic output ever since Lebanon’s independence. “This generated very high dependence on imports in order to cover household consumption. At the end of the day [these dependencies] translate into lower potential growth rates in GDP but, more dramatically, it creates not only lower growth rates [in the economy] but also a much lower job component in those lower growth rates,” he reasons.

What is needed for Lebanon in light of this entrenched problem is something that banks cannot produce. “What we need to do – and here our politicians have failed and banks are accused of not helping through inclusion – is initiate a process through a new social contract in Lebanon between politicians, working people and economic associations,” the board member of Lebanon’s top bank advocates with verve. Baz is on a roll and continues “The solution that we need is to shift from a domestic-demand-triggered growth in Lebanon to a foreign-demand-triggered growth, by lowering consumption, [and] by increasing real savings. In order to promote productive investments, to bring back Lebanese labor, to have competitive exports and to lower the dependence toward inflows and inputs, we need a new social contract. Banks can probably speed up the process but we cannot initiate it.”

")