The Lebanese constitution is clear in laying down the principles of democratic governance and the

responsibility that those who wish to hold office have towards economic democracy, social equality,

human rights, and more. And yet, our daily reality is nothing if not a narrative of chaos.

Isn’t it ironic that we despair that our political leaders cannot agree on a government but we have no

greater wish than getting rid of our political corruption?

I don’t know if you agree with me but I hold true that we all, each in our own way, have to challenge the

chaos that is bringing us to our breaking points. For Executive, putting our shoulder to the wheel of

fighting chaos has meant holding industry roundtables and asking leaders in our economy: How can a

corporation preserve the value that it built over years of hard work, retain its talent and pursue

profitability in an environment where those in the highest political power have demonstrated their

disregard of all those principles?

Their answers and other lessons of the chaos experience of this year up to the present moment

encourage me to call your attention to three points of note and request your responses.

Lesson One: Economic democratic principles are built on contracts and agreements. The functioning of

such an economy needs all its participants’ adherence to policies and procedures. Public and private

institutions alike therefore must be accountable, honoring contracts, reporting to internal and external

auditors, and obeying legal and regulatory authorities that monitor and reinforce commitment to

governance standards and take to task all those who breach the law and violate stakeholders’ rights.

This is what builds trust, attracts capital, and nourishes innovation and trade.

Lesson Two: The ethical firm and the ethical state are more than assemblies of contracts and

agreements. They need purpose, and the ethical state must support the purpose of the ethical firm and

the ethical family, just as the ethical family and ethical firm have to meet their obligations to the state.

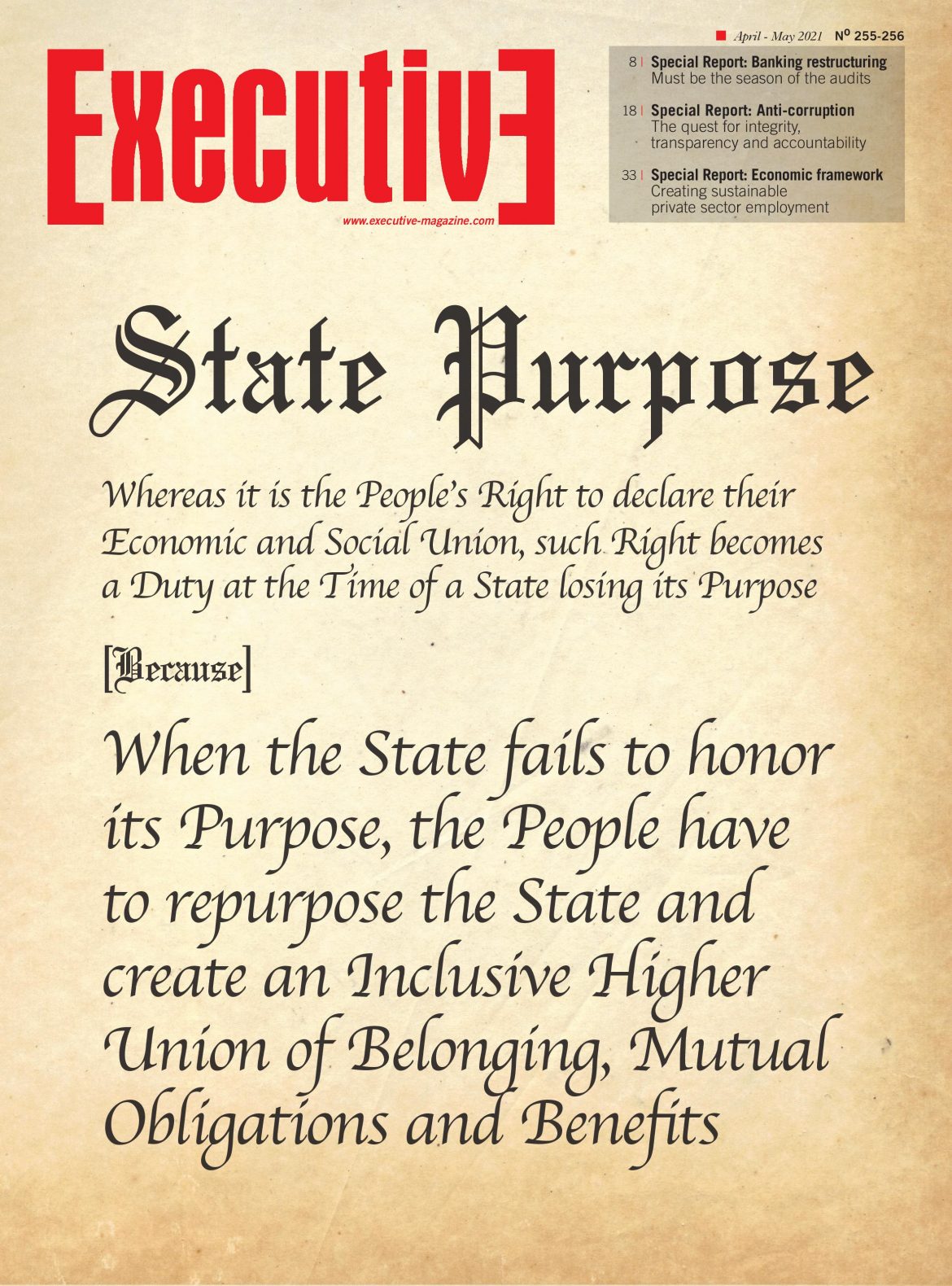

Lesson Three: When the state fails to honor its purpose, the people have to repurpose the state and

create an inclusive higher union of belonging, mutual obligations and benefits.

It is obvious that political systems will be degraded and fall into chaos if they produce public servants

that use the constitution as a tool to grab power and gain unfair advantages for themselves. They slide

down the slope of corruption, extracting economic value without adding any value in return. Pursuing

this model of constant depreciation, the culture of public corruption crowds out those who want to play

by the rules. Instead of being the agency of growth for private economic actors, such a broken public

system exhausts the remaining economic performers, be they employers or employees, consumers or

producers.

The Lebanese private enterprise can and must build its capacity to rise above the broken system. In an

increasingly connected and globalized world, the Lebanese private enterprise can and must evolve,

adapt, and persist in its pursuit of value creation. Its talents will always be recognized and valued for

their creativity and innovation.