It is time to celebrate. After 22 years of occupation in South

Lebanon, Israel pulled out quickly and quietly, leaving the

country with a sense of relief and a brighter picture for the future.

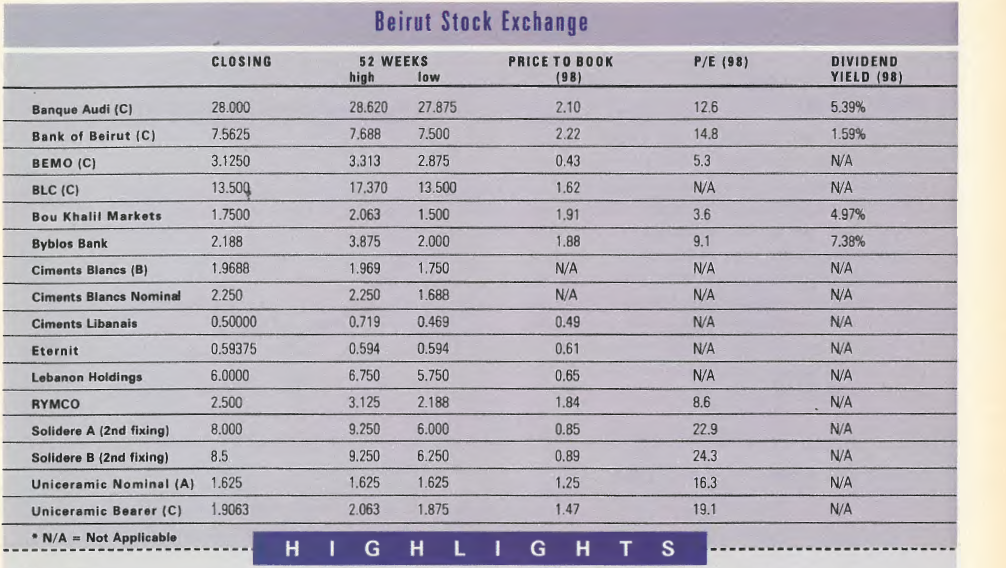

But it is also a time to worry. Solidere, Lebanon’s biggest company,

is reeling under the harsh economic conditions and political

uncertainties in the region. If that isn’t enough, the company is

wrestling with the government over permits.

The cabinet has approved the long-awaited privatization bill. A sell-off

of state-run assets could cut the debt by 30%, but it’s unclear how

privatization will be handled, or if it actually happens.

The country’s two cellular telephone operators, LibanCell and

Cellis, have their own reasons for worry. The government, claiming

the companies have breached their contracts, has ordered each

to pay a $300 million penalty or risk having their contracts canceled.

LibanPost, which began pumping new life into the country’s faltering

postal system over a year and a half ago, is also facing a barrage

of difficulties.

This month’s cover story examines the effects of the Israeli withdrawal

on the economy. Peace and stability following the pullout

could bring untold benefits. But if there is violence, the results could

be devastating.

All around, there are uncertainties in Lebanon, and uncertainty is

the enemy of economic development. Some matters, like what will

happen following the Israeli pullout, we have little control over. But

for others, like the cellular contracts, LibanPost, and Solidere, we

do. By hassling companies that are investing in rebuilding the country

and its economy, we are telling future investors that Lebanon

is not a safe place for business. Haven’t the Israelis done enough

of that already?