Lebanon’s administration needs qualified personnel. Why can’t they be found?

Lebanon is facing a brain drain while its administration is desperate to find the right people to fill posts. But it’s unlikely that the best and brightest would seek employment with the civil service.

The administration’s cadre (pre-fixed ministry positions) has 24,000 posts, of which only I0, I 82 are filled, though the actual number of people working at ministries is more than twice that figure. This is largely due to rampant hiring of political appointees during the war. But they are often unqualified for the job. Even if the civil service board ended its freeze on hiring, “the administration doesn’t have the setup to attract talented people,” says Jihad Azour, an advisor to Georges Corm, the minister of finance.

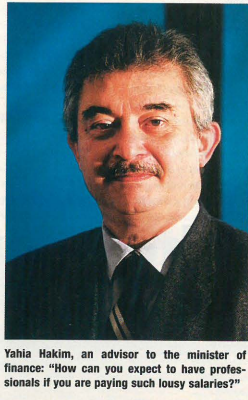

For starters, the wage scale leaves much to be desired. The most prestigious positions, director generals, are paid $1,660 per month; heads of directorates and services, $700 per month; heads of bureaus and sections, $533 per month; clerical staff, $267 to $400 per month; and unskilled labor $200 per month. “How can you expect to have professionals if you are paying such lousy salaries,” asks Yahia Hakim, one of Corm’s advisors. Even worse, raises are not based on merit. According to one source, salaries are based on seniority, not on skills and productivity. That, combined with promotions not being based on merit, breeds complacency.

To enter the administration candidates must pass a general exam. But postings are made in an ad hoc manner. “If the minister of economy has a vacancy, and he makes a request to the civil service board for someone with an economics background, they will send someone with completely different qualifications,” says one source. “Because there are lots of people with degrees in history and Arabic literature, but not with finance, degrees in the sciences and economics, things that can be more useful.” Strikingly, the only economist at the ministry of economy today is the minister himself.

Much of the qualified staff actually work in separate units that were established to coordinate and implement reform programs, largely funded by international donor agencies like the World Bank. Ministers also bring in advisors, who are hired under contract. These jobs don’t fall under the banner of civil service, and candidates are attracted because of the salaries, which are generally between $5,000 and $8,000 per month. The rate for rookies is about $1,500. Civil servants are often resentful towards those within the units and don’t collaborate on projects.

How successful are the reform projects? Those involved say things aren’t progressing as anticipated. Many leave before their contracts terminate, while others decline to renew. That’s largely due to frustration with the delays in the reform process.

The administration itself faces an image problem. “The public sector needs to market itself better,” says Azour. “A lot of people are interested in working at the central bank, because it has a better image. But it is also a public administration.” In other countries people enter the public service, because it adds to their value if they decide to go into the labor market.

“The problem is trying to get the human resource management structure in the government in line with the private sector structure,” says Raymond Khoury, director and senior IT strategy advisor for the ministry of state for administrative reform. “By having merit-based promotions, and career profiles – putting the right person in the right place. People don’t become skilled for the purpose of sitting at their desk and reading newspapers all day.”

The administration’s cadre was designed in 1959. Are all 24,000 posts necessary? Not according to consultants. For example, the ministry of finance is understaffed according to the law; just 833 of the 1,649 positions are filled. But in reality 1345 people are employed there: another 37 are contractual, 48 are temporary and 427 are paid by the hour. “No one can tell me that the ministry of finance is understaffed,” says one consultant. “Because they have not properly redefined what the functions of the ministry are.”