Most Lebanese textile companies are holding on by a

thread in today’s difficult times. Customs duties on raw

materials range from 20% to 25%, higher than in

any neighboring country, while electricity, fuel and labor costs are

the highest in the region. The entire sector must also compete with

cheap imports from East and Southeast Asia and with finished big name

brands from Europe. ”The economy is falling and the textile industry is following it,”

says Sleiman Khattar, president of the Lebanese Textile

Syndicate and owner of La Laniere Nationale.

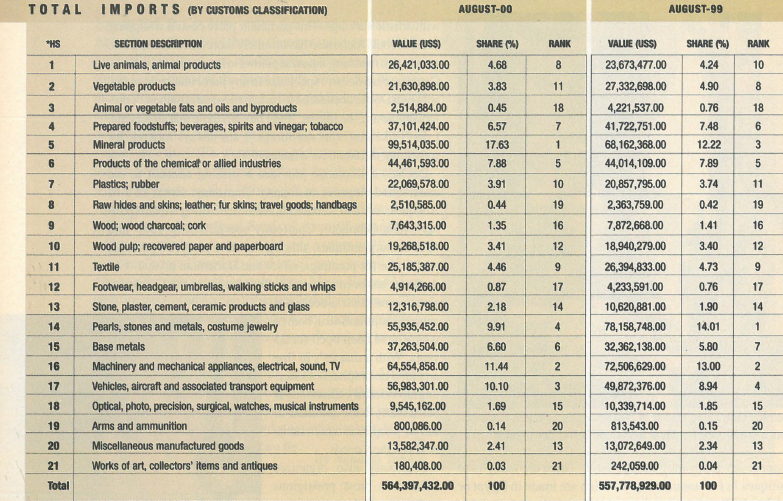

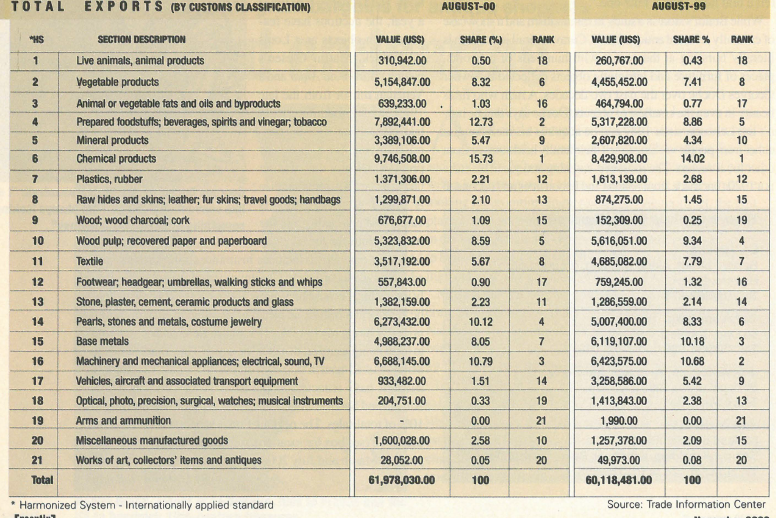

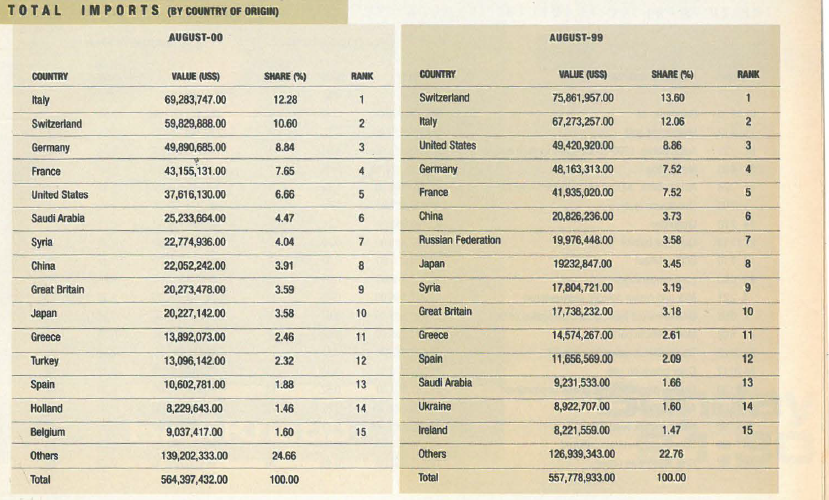

Textile exports dropped from $73 million in

1973 to$35 million in 1999, while imports rose

from $168 million to $238 million during the

same period. In the last few years, several

local textile companies have ~one out of business.

But in the midst of this malaise, one

local clothing and textile manufacturer,

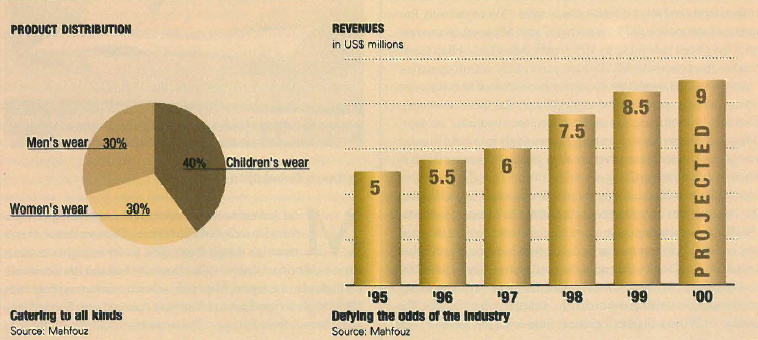

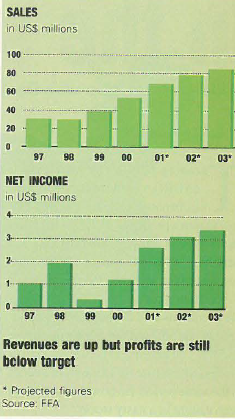

Kassem Mahfouz & Sons, has seen its revenue

grow from $5 million in 1995 to $8.5 million

in 1999, with a projected turnover of $9 million for 2000. Compare Boudakian – a textile

company that makes uniforms. It has decreased production to 1,000

pieces a day from about 1,600-1 ,700 at the start of 1999.

Mahfouz manufactures 70% of its clothes; the rest is either purchased

from local manufacturers or imported from East Asia. The company

concentrates on high volume sales at low margins. “Our main strategy

is to decrease prices and increase sales,” says Bassam Mahfouz,

the firm’s president. The company controls all stages of the production,

marketing and sales process, cutting out middlemen. “You

find other companies who work in specific areas, but we go through

the whole process,” he says. The company’s clothes are sold at

seven nationwide retail stores and two wholesale outlets. Mahfouz is

in the process of adding two more branches, one in the South and

another in Tripoli. When choosing the location of a new store,

Mahfouz is careful to select places that are far from potential competitors.

But when a competitor is nearby-such as in Choueifat, where

his store is close to another shop called Zakr- he is careful to make

sure that his prices are low and targeted at bargain-conscious consumers.

“Other companies don’t have the same customers I have, so

I feel no threat from them,” says Mahfouz. For this reason, Roy

Badaro, owner of children’s clothing chain Kindou, feels that

Mahfouz is no threat to him either. “Mahfouz has different customers

because of its low end products,” says Badaro.

Mahfouz has also been helped by recent

changes at customs. Last spring, the ‘specific

rights’ law went into force, charging customs on

textile imports by weight rather than value. For

each kilogram, an importer is required to pay

LL9,500. The new rule makes it difficult for

importers to cheat by claiming that clothes or textiles

are used or cost less than their real value. This

law has led to a decrease in imports, according to

the syndicate, hence boosting business for local

manufacturers. “Due to the new law, I started producing

at 70% capacity. I was originally operating at 40% capacity,” says Mahfouz.

His company’s biggest strength is socks. “We have one of the

biggest factories for manufacturing socks in the Middle East,” says

Mahfouz, who has the exclusive rights for the whole Middle East

to manufacture socks under the Disney brand name. “Mahfouz was

chosen because of its competitiveness, its new machinery and its

high-tech equipment,” says Khattar.

Mahfouz keeps up with the pulse of the market by attending exhibitions

in Europe and the Far East up to four times a year and by

browsing through catalogues. He tries to adapt the latest fashions

to the demands of the local market. “We usually start preparing a

particular collection one year ahead of time,” he says. Keeping up

with the latest trends is very important in this business, explains

Khatter. “Some of the factories that didn’t follow the fashion and

the new trends have been forced to close,” he says. “It’s important

that the right product is produced at the right time.”

Mahfouz also exports, with 20% of sales going to places like Italy,

Greece, Cyprus, Hungary and the Gulf. Mahfouz is a rare breed.

In an industry where most textile manufacturers are simply trying

to stay afloat, his company is operating in the fast lane. “I’m working

on increasing demand. I want to increase my production

capacity to 100%,” he says.