Ego and tradition have tended to

dominate Lebanon’s business circles.

Losing control of the family

fiefdom is viewed as one of the worst

nightmares, regardless of whether that

might involve a sound business decision.

But this is the new generation and

Lebanon’s Internet service providers are

among those at the forefront.

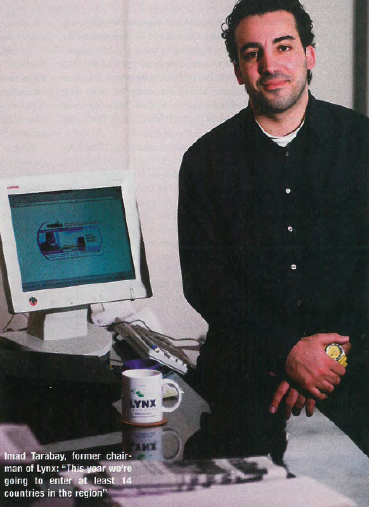

Imad Tarabay, the 27-year-old chairman

of Lynx, received an offer he couldn’t

refuse and wouldn’t disclose from

PSINet, a US-based multinational Internet

company with revenues of $555 million

last year. It was a tough choice: either roll

up the drawbridge and face a competitive

local market alone, or give up the reigns reins to

an international heavy**-**weight. Tarabay,

now vice-president of sales and marketing

for PSINet Middle East and Africa, decided

to sell at the end of December. And as

competition increases and prices drop,

more of Lebanon’s ISPs are having to face

the bitter reality that they cannot stay afloat

without financial backing.

But what on earth would attract a multinational

to a market of not more than

100,000 Internet users, less than 0.05% of

worldwide surfers?

The target is not just the local market.

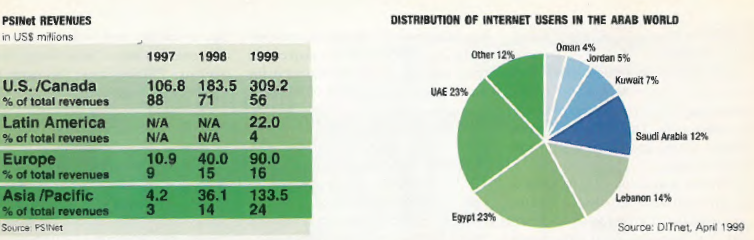

Now, Tarabay is standing tall among local

competitors and is readying the company for an aggressive push into the Middle East, a

region with an estimated 1 million Internet

users (see chart). “This year we’re going to

enter at least 14 countries in the region,”

says Tarabay. The buy-out of Lynx is part of

PSINet’s strategy to expand internationally

by acquiring existing ISPs rather than

establishing new ones from scratch. In

1999, the company acquired 43 ISPs

worldwide, including the purchase of

seven in Latin America (see box).

According to Tarabay, PSINet was

attracted to Lynx’s fiber-optic network.

Though ISPs are generally reluctant to

reveal the arrangement of their network’s

structure, the majority have routes through Cyprus or the UK. Lynx, the self-proclaimed

fifth largest local ISP with over

4,000 subscribers, claims to be the only

one with a direct fiber optic connection to the

US, avoiding any nodes or intermediary

connections. This minimizes the number of

errors and error-corrections during transmission.

Lynx still had to go through the

MPT. “I spent six months working on it,”

says Tarabay.

The regulatory environment could create

obstacles to further expansion into some

countries in the region. Egypt, where there

are about 55 ISPs, Jordan and Saudi Arabia

offer attractive markets for acquisitions.

Others, like the UAE, where one company

monopolizes the Internet, are off-limits. In

Lebanon, ISPs are at the mercy of the ministry

of post and telecommunications

(MPT), which has the sole power to grant

companies the bandwidth they require.

But whatever the hurdles now, the company’s

strategy is long-term. Many multinational

companies go into markets prematurely

in order to gain a head-start on competitors.

Ericsson, the Swedish mobile phone manufacturer,

recently opened a regional office

here. Sony, Japan’s leading electronics giant,

opened its Lebanon office two years ago.

Both are the first in their industries to enter the

local market, before the environment

becomes attractive to competitors.

“Privatization is being echoed in Lebanon

and international research firms contracted for

studies,” says Sam Lutfallah, executive

director of Inconet. “They are lured by this.”

And what better way to get into a market

than by linking up with a local firm. It was

Lynx that originally approached PSINet in

July with an offer to form a joint venture.

Tarabay, who had established Lynx with his

partner Raed Rayess only three months earlier with a $300,000 initial investment,

wanted to expand into the region and needed

a financial backer. “We had a lot of contacts

in the area, but we needed technical

and financial assistance,” he says. “Any

country you want to go into requires an

investment of $1-2 million to start up.”

Negotiations proceeded till November,

when PSINet suddenly handed Tarabay its

offer to buy.

But the new entity will not recreate the

Internet. The company has the same dial-up

and e-commerce services offered by other

ISPs. A number of services that PSINet

provides elsewhere, such as ISDN and

VoiceOver IP, cannot be offered here for the

moment because of the monopoly of the

MPT. “They are offering nothing that

[other ISPs] here don’t have,” says Abude

Omari, CEO of Cyberia. Since it’s a carrier

as well, PSINet/Lynx will be able to sell international links out of Lebanon to other

ISPs, once the MPT relinquishes its monopoly.

Lynx can take advantage of the financial

and technical boost in order to improve

services. Tarabay plans to upgrade the

amount of bandwidth in order to increase the

speed and capacity of connections.

Although the company may have the

financial weight to cut rates, don’t expect

any new price wars on dial-up. Already,

Lynx has some of the highest rates on the

market, ranging from $14.99 for unlimited

access ($9.99 for students) up to $29.99 for

unlimited corporate accounts. Tarabay

says that there are no plans to reduce these

rates any time soon. “Cutting prices was

never our strategy,” he says. “We’re going

to maintain our prices because we believe

that if you want quality you have to pay a

higher price.” Nor is the competition worried.

“This move will not affect prices,”

insists Fadi Ghazzaoui, marketing manager

for TerraNet.

With dial-up prices unprofitably low,

Lynx is focusing on the corporate market,

where it can offer a greater array of services

at higher rates. That will pit it against

Inconet, the self-proclaimed leader in corporate accounts.

PSINet’s acquisition of Lynx came as

no surprise to others in the sector. “The natural

trend is toward consolidation,” says

Bahjat el-Darwiche, IntraCom’s managing

director. “If ISPs are not backed up

financially in some way, they will not

last,” says Tarabay.

The prospect of international firms entering

the market did not seem likely last

September. Sitting in his office in Hamra,

Omari was skeptical. “Why would [a

multinational] want to operate this small

Internet service in a market of 60,000

users, when they add close to a million

users per quarter?” he told EXECUTIVE at the

time. But now he thinks differently:

“International players who bring in money

and expertise show that the market is interesting.”

Louis Hobeika, chairman of

Sodetel, welcomes the healthy dose of foreign investment that the entrance of companies

like PSINet into the market will

bring. ISPs are having trouble surviving

with rates so low, and most of the major ones say that they would welcome some sort

of partnership with a large foreign firm

(see box). PSINet’s move just might be

what’s needed to get the ball rolling.

Top of Form

PSINet’s expanding by buying out ISPs worldwide

Internet carrier PSI Net was the first company to commercialize the Internet in 1989.

CEO William Schrader was one of the founders of NYSERNet in 1985, the first network

to link university, government, and corporate supercomputers in New York.

He realized the potential of the Internet when corporate clients started approaching

NYSERNet. Being a non-profit organization, the company subsidized PSI Net

to sell Internet services.

Acquisitions in the third quarter ended September 30, 1999:

- Transaction Network Services (TNS): provider of eCommerce data communications

processing. Revenue in the third quarter 1999 was $46.1 million, net profit

$5.5 million. Sold for: $720 million in cash and stock. - In the US/Canada: Two ISPs, Internet Network Technologies (US) and TotalNet

(Canada). Add 100 business accounts. - In Europe: Seven ISPs in Spain, Austria, Hungary, and Italy. Add over 1,200 business

accounts. - In Asia Pacific: Two ISPs in Hong Kong, Global Link and Vision Network Online.

Add 500 business accounts. - In Latin America: Seven ISPs in Panama, Brazil, Argentina, and Chile. Add over

500 business accounts.

Would you sell? Here’s what the ISPs replied

Word has it that America Online

Inc. (AOL) has its eyes set on the

local market, though it seems that the

rumor’s been running for a while now.

EXECUTIVE also found out from several

sources that the French ISP Wanadoo

(www.wanadoo.fr), associated with

France Telecom, is in talks with Gellis.

This is the next big thing now.

Most ISPs refer to “partnerships”

rather than mergers and acquisitions.

The sector should witness a number of

joint ventures in the near future. Here’s

what the main players had to say.

CYBERIA: “We have no incentive at

this stage to sell. We might partner up,”

says CEO Abude Omari. Cyberia is privately

financed and will continue to be so.

INCONET. “We welcome a joint venture,”

answers executive director Sam Lutfallah, “but one in which we have a controlling

interest. We would not release our

shares.” But, he adds, if the offer were

good, the company would be open to a

buy-out. Inconet is under the umbrella of

GlobalCom, a holding company half

owned by Audi Investment Group.

SODETEL. Louis Hobeika said that he

is open to a partnership. Telecom Italia

and France Telecom together own 50%

of Sodetel.

TERRANET. Marketing manager Fadi

Ghazzaoui claims talks are underway “in

Europe and Arab countries for a partnership.

Acquisitions are not healthy,

because they would allow an [international]

firm to take control of the local

market.” TerraNet is a sister company to

LibanCell. Nizar Mohsen Dalloul is a

major shareholder in both companies.

Bottom of Form

Bottom of Form

Hack Attack: the World Wide Worry

Accessing someone’s server can be surprisingly easy.

Luckily the “art of hacking” is still rudimentary in Lebanon

Hack attacks are all the news almost monthly now.

International news, that is. Think you’re safe from similar

attacks because your Internet service provider certifies

it, because you have a firewall, or because there are no hackers

locally? Think again. “Hacking, like AIDS, is thought to happen

to other people,” says MajorD0m0. “But it can happen anytime,

anywhere, to anybody. It’s simple, and I can prove it.” So EXECUTIVE took him up on his word.

MajorD0m0 is a 20-something ethical

hacker, a rare breed whose reputation has

been soiled over the last decade by Internet

vandals and egotistical teenagers. In fact,

MajorD0m0 is a hacker in the original sense of

the word, which used to describe an amateur with a thirst for knowledge about computer technology without the

malicious intent. Web-wise, MajorD0m0‘s hacking expertise is the

result of years of surfing and learning.

“Name your website,” smiles MajorD0m0. He makes hacking look

easy, to the extent that one forgets its implications. He uses point-

and-click software, and types in just a few commands. The tools are

at his fingertips on the PC. Each is a downloadable program rarely

larger than 50kb and thus takes minutes to install and use.

They are just a few clicks away on the Web. Port scanners detect

types of networks, servers and ports that give leeway to hackers.

A trojan horse is a program embedded in email attachments that

can be secretly sent to users, allowing hackers to take control of

the remote computer. Mail bombers send thousands of junk

emails to an address, blocking or slowing down access to

emails. Password crackers are programs that can crack a user’s

password. The list goes on.

He thinks up a few local dot-coms, considering the rush to e-commerce

and everybody feeling hip about being online. Scanning a

server, MajorD0m0 detects which ports are “open.” Any information

a port provides gives the hacker more to work with. Most

ports are susceptible to some form of attack, be it access to files

or databases. He clicks, types in the website’s IP address, and up

comes the message: “start scan … ports 0 to 1000.” Seconds later

a list of ports follows. “Eureka,” he exclaims.

Each of the seven websites he tried, owned by major local

companies, had at least eight ports exposed, most commonly the

file transfer and mail ports. Secured sites wouldn’t allow scanners

to detect any of their ports. Their security system would trace the

intruder’s IP address and block access from it. MajorD0m0

demonstrates with two secured websites, where the scan message

appears but returns no information. This is one step short of

actually breaking in. But that’s as far as MajorD0m0 will go.

Hacking in Lebanon is still amateur, MajorD0m0 confirms. It’s

usually done upon a dare. The hacker uses software to crack a

friend’s email password, or take control of their desktop, turning

it into a zombie, shutting down Windows and performing tasks remotely from their own

computer, all for a laugh.

Locally, the Internet’s

limited speed (up to

36kb/s) and the lack of

permanent connections

to the Web pose difficulties

to any serious hacking

activity.

But that should not be

comforting. The threat is

global, and proficient

hackers worldwide can

attack. There is little

awareness of security in

the Middle East as a

whole and in Lebanon

particularly. Hackers

from Brazil recently

vandalized several websites in the UAE and Saudi Arabia. Vandals usually post a message

mocking the webmaster or the institution, send greetings to their

buddies and boast about their skills. After such attacks, the

servers have to be shut down and scanned, since it’s not easy to

identify exactly what the hacker did.

This is not to imply, however, that anyone can or should attempt

hacking. In fact, amateurs lacking programming and Internet

knowledge could put themselves in danger of being traced and

caught. A hacker doesn’t always go it alone, since collaboration

and speed are needed to “get in and get out” safely. MajorD0m0

points out that hackers work in pairs or groups. While one gains

access to the server and proceeds to vandalize it, the other erases

any “traces” left behind.

Did MajorD0m0 hack into any websites? No. Reading up on hacking

remains his hobby, and besides, he has better things to do. We might

be better off taking his word for it. After all, never dare a hacker.