Remember all the glowing clichés you’ve heard about

Lebanon? A bastion of capitalism within a sea of controlled

economies, a regional hub, the Switzerland of the Middle

East. With relatively low tax rates and banking secrecy, Lebanon

must be one of the freer economies in the Middle East, if not the

world, right? Think again.

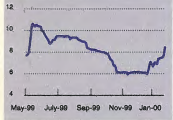

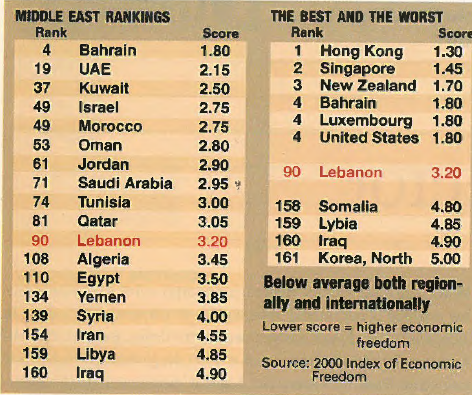

The Heritage Foundation and The Wall Street Journal, in their

recently released 2000 Index of Economic Freedom, ranked

Lebanon as number 90 among 160 countries (see chart), placing

it in the “mostly unfree category.” Lebanon found itself even

with such countries as Guyana, Madagascar and Moldova. Even

worse, it scored one point below Mongolia and three points below

Guinea and Ghana, while Fiji, Nigeria and Papua New Guinea

ranked just below Lebanon, tied at number 94. (Ratings are based

on 1998 statistics.)

Conducted annually since 1995, the survey has become something

of a benchmark for measuring the ease of doing business

in a country. Rankings are based on ten

broad factors of economic freedom: trade

policy, the fiscal burden of government,

government intervention in the economy,

monetary policy, capital flows

and foreign investment, banking,

wages and prices, property

rights, regulation and the

black market. Each factor is

scored from one to five and

averaged to determine the final grade. The

higher the score, the greater the government

interference in the economy and the lower the economic

freedom. Hong Kong topped the list of “free”

economies with a score of 1.3. Trailing the pack are repressed

economies like North Korea, which scored five. Lebanon’s score

was 3.2, below average, not only by world standards, but also by

regional standards. Among 17 countries in the Middle East,

Lebanon ranked 11th.

The study showed a direct correlation between the per capita GDP

and the level of economic freedom. “Countries with greater economic

freedom have a faster rate of economic growth and a higher

standard of living,” says Nassib Ghobril, an analyst at Lebanon

Invest. “The study is used by policy makers and investors to

assess the investment climate in a country. If a company were to

set up an office here, obviously it would want more business-friendly

policies. It’s not the country of choice. Why not set up in

Jordan, or the UAE, which is second only to Bahrain?”

Why did Lebanon score so poorly? Ghobril points to three important factors.

First, Lebanon scored a maximum of five on trade policies. High

tariffs and surcharges on imports are the main culprits.

According to IMF statistics, trade taxes account for more than

70% of the total taxes collected by the government. In an attempt

to control the high deficit, the government has increased tariffs over

the past several years. This will make the country’s hopes of joining

the WTO and the Euro-Med agreement difficult, as both deals

would require a general phasing out of trade barriers.

Lebanon has signed free trade agreements with Syria, Egypt and

Kuwait as well as the Arab common market agreement. “But still

overall the tariffs are considered very high,” says Ghobril.

Lebanon also scored five in the “black market” category, largely on

account of its rather porous border with Syria and its thriving

business in unauthorized cable television and pirated software.

Lebanon’s score was also disappointing

– 3.5 – on the fiscal burden of government, which includes income and corporate

taxation plus government expenditures. With a top income

tax rate in 1998 of 10%, Lebanon received a two for taxation. But

that was averaged with a score of five for expenditures, which were

almost 44% of GDP in 1998. Even in some areas where Lebanon

prides itself on openness, the results were disappointing. The

country received a three, “moderate barriers,” for capital flows and

foreign investment. According to the US Department of Commerce,

“Lebanon offers the most liberal investment climate in the Middle

East, with no significant restrictions on foreign investment.” The

report disagrees: “It restricts the amount of real estate a foreigner

may own and needs an efficient investment approval regime.”

It was not all bad news, however. Because of a “low level of

restrictions,” Lebanon received a two for its banking sector and on

prices and wages. As another bright spot, the index showed a modest

improvement from last year, when Lebanon scored 3.25. But

the score for 2000 is still far below its 1997 score of 2.95. And not

everyone agrees with the index’s rating. Kamal Hamdan, an economist

with the Consultation and Research Institute, feels that

Lebanon was under-rated in a number of areas. Trade barriers may

be high by international standards but by regional standards they

are not unusual, he argues. Hamdan also questioned how Lebanon

scored a five for black market, while Nigeria, which he believes has

a far worse problem, scored a three. The five for government expenditures

is also unfair, he says, because the survey calculates the

money spent on debt servicing. “I think Lebanon should be among

the top 30 to 50 countries,” he says. Marwan Iskandar, head of MI

Associates, agrees: “I think that these measures are rather arbitrary.

I would not give much credence to a study like this.”

There are reasons for hope and despair for next year. The “black market”

rating may improve if the new intellectual property rights law,

passed by parliament last spring, is enforced. On the down side, corporate

tax was raised from 10% to 15%, while the top income tax bracket

was increased from 10% to 21%. That could affect next year’s score.

OK, so Lebanon might not be a bastion of capitalism, but at least

it’s a nice place to live, right? Well, actually no, according to another

survey by international consulting firm William M. Mercer. It

ranked Beirut 168th out of 218 cities based on quality of living. The

survey was based on 39 standards including political, economic and

environmental factors, personal safety and health, education, transport

and other public services. Among the notable cities that beat

Beirut were Medellin, Colombia, the cocaine capital of the world,

and Cairo, Egypt, where the smog is so bad that a walk on the Nile

can cause lead poisoning. At the top of the list were Vancouver,

Canada and Zurich, Switzerland. At the bottom: Brazzaville and

Pointe Noire, Congo and Khartoum, Sudan. Well, at least in

Lebanon, we can ski in the morning and swim in the afternoon. Then

again, who would bother?